U.S. Dollar Index forecast: FOMC-driven dip reversed as DXY climbs to 5-day high

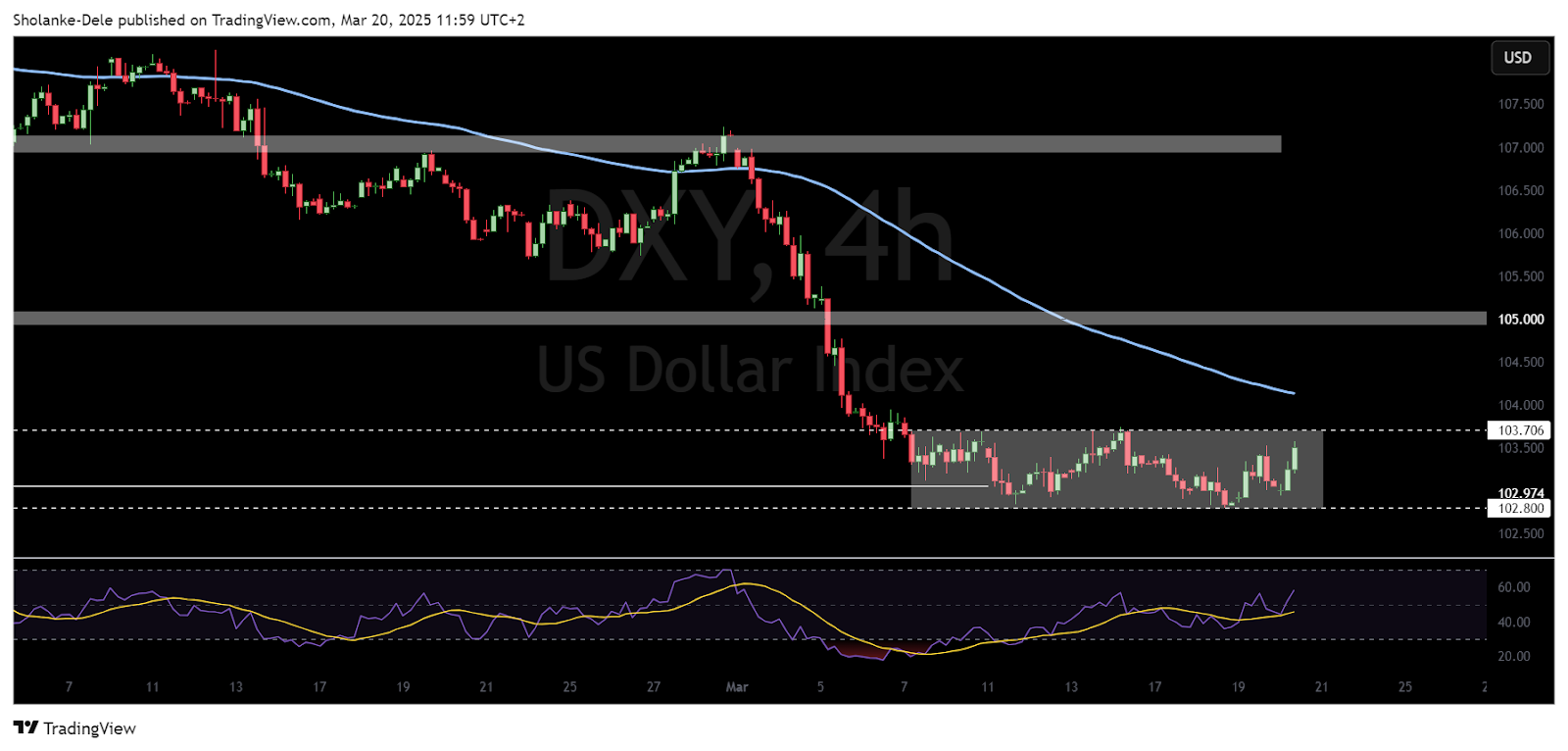

DXY attempts breakout, rising 0.57% to a five-day high of 103.6.

DXY attempts breakout, rising 0.57% to a five-day high of 103.6.

The U.S. Dollar Index (DXY) is attempting to break out of its recent range following the intraday dip that occurred as a result of the FOMC news. Despite the initial decline, the index regained momentum in the European session, rising 0.57% to a five-day high of 103.6. However, price is still within an eight-day range of 103.7 to 102.8, leaving traders watching for a decisive move.

A push beyond the 103.7 resistance level is needed to confirm further upside, with bullish momentum evident in the 4-hour RSI. A successful breakout could open the door for an extended rally, while failure to sustain gains may see price remain trapped within the range.

DXY price dynamics (Feb 2025 - March 2025). Source: TradingView.

U.S. jobless claims and philly fed index to shape dollar’s next move

The upcoming U.S. Unemployment Claims report and the Philadelphia Fed Manufacturing Index will be critical for the dollar’s next move. The forecast for initial jobless claims stands at 224K, slightly above the previous reading of 220K. A lower-than-expected figure would support the dollar, reinforcing confidence in the labor market and potentially strengthening expectations of tighter monetary policy.

Meanwhile, the Philadelphia Fed Manufacturing Index is projected at 8.8, significantly lower than the previous 18.1 reading. A weaker-than-expected result could dampen sentiment, signaling deteriorating business conditions and adding uncertainty to the dollar’s outlook.

The dollar’s ability to sustain gains hinges on whether it can break 103.7 resistance. A stronger labor market report or a resilient manufacturing index could fuel further upside. Conversely, weak data may trigger another retreat, keeping the index stuck in its consolidation range. For now, traders remain focused on key levels and upcoming economic releases, which could set the tone for the dollar’s direction in the coming sessions.

Stronger-than-expected U.S. industrial production data reinforced expectations of a firm Fed stance. The DXY rebounded from 102.80, its lowest level since October, rising 0.4% to 103.35.