S&P 500 under pressure as tariffs, tech selloff, and recession risks cloud Q2 outlook

S&P 500 starts Q2 under pressure as tariffs and volatility drive sector rotation

S&P 500 starts Q2 under pressure as tariffs and volatility drive sector rotation

The S&P 500 enters the second quarter on a defensive note after closing Q1 2025 with a 4.6% decline, as fears over U.S. President Donald Trump’s escalating trade war and weakening growth prospects weigh on sentiment. With additional reciprocal tariffs due for announcement on Wednesday, market participants are reassessing exposure to sectors vulnerable to supply chain disruptions, while recession odds and volatility tick higher.

Goldman Sachs has raised the probability of a U.S. recession to 35%, citing trade-related inflation shocks and signs of softening demand. The investment bank also trimmed its S&P 500 year-end target to 5,700. Meanwhile, the Nasdaq posted its worst quarterly performance since 2022, sliding 10.5% as the “Magnificent Seven” tech giants led losses. Tesla fell 36%, while Nvidia lost nearly 20%, reflecting tariff-related concerns, stretched valuations, and increased regulatory scrutiny.

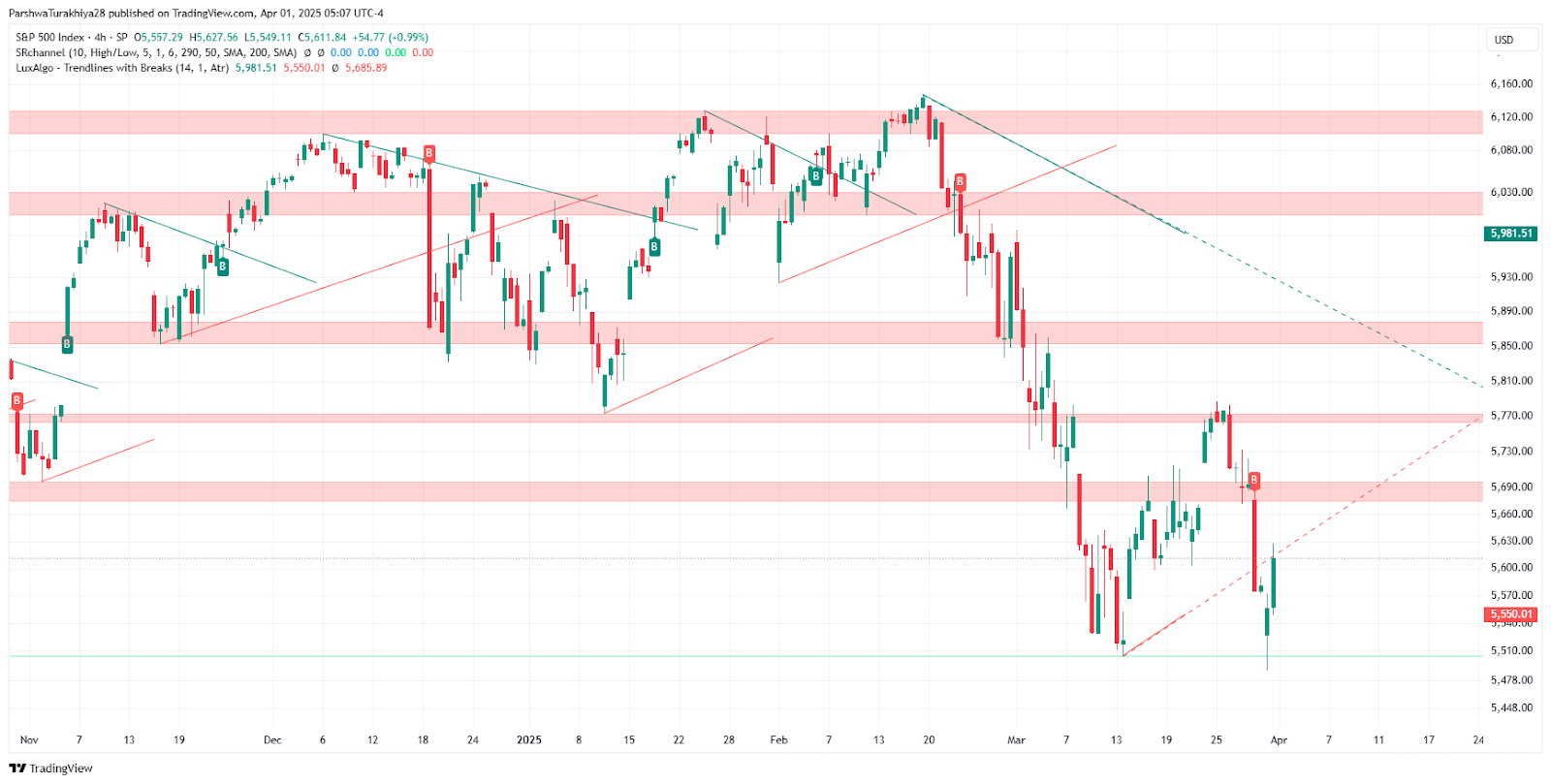

S&P 500 price forecast (November 2024 - April 2025) Source: TradingView.

Sector rotation emerges as volatility rises

Investors are shifting capital into defensives, with energy stocks rising 9.3% in Q1 amid geopolitical tensions and supply risks. Consumer staples also gained, offering a haven amid elevated volatility, with the CBOE Volatility Index (VIX) climbing to 22.28. Financials saw selective interest, driven by M&A activity—Discover and Capital One advanced 7.5% and 3.3%, respectively. Analysts suggest that value and cyclical sectors may outperform as tech leadership falters.

The broader trade outlook remains fraught with uncertainty. Aluminum, steel, and auto tariffs are already in effect, and Trump’s upcoming measures are expected to target all remaining trading partners. The sweeping scope of the tariffs risks exacerbating inflation while eroding corporate margins and consumer spending power. This trade-induced uncertainty complicates the Federal Reserve’s calculus as policymakers weigh inflation containment against a fragile economic backdrop.

Outlook for Q2: Brace for defensive positioning and volatility

As the market adjusts to a shifting economic and policy landscape, analysts advise a selective approach, focusing on companies with strong domestic revenue streams and limited exposure to trade disruption. With the ISM and labor market data due this week, investor attention will turn to Fed guidance for clues on possible rate cuts in the second half of the year.

As highlighted in previous coverage, the S&P 500's trajectory remains clouded by macro risks, including Fed policy uncertainty and global trade tensions. With volatility rising and defensive sectors gaining favor, market participants should continue to monitor developments in fiscal policy and U.S. data releases closely.