Euro price holds firm near multi-year high, while yen and Aussie dollar soften on dollar rebound

Euro gains cool as ECB cuts rates and U.S. dollar steadies on Powell support and trade optimism

Euro gains cool as ECB cuts rates and U.S. dollar steadies on Powell support and trade optimism

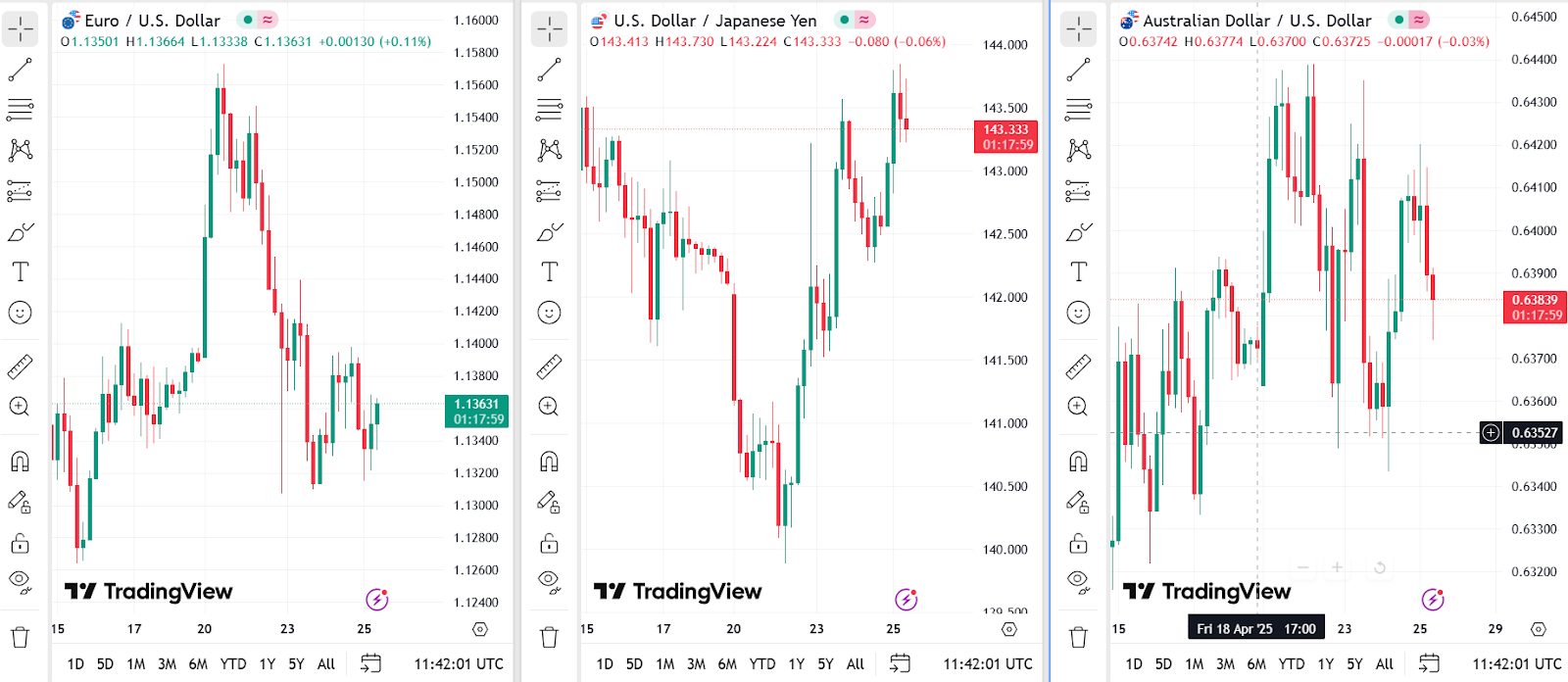

The euro traded around $1.14 on Friday, consolidating just below its recent peak of $1.15—the highest level since 2021—as investors digested a series of central bank updates and shifting geopolitical narratives. While the common currency has surged more than 5% against the U.S. dollar this month, momentum cooled slightly after President Donald Trump signaled support for Federal Reserve Chair Jerome Powell, easing concerns over political interference in monetary policy.

The European Central Bank cut its deposit rate by 25 basis points to 2.25%, the lowest since early 2023, and removed language describing its policy as "restrictive." Still, policymakers warned that the economic outlook remains clouded by deepening global trade tensions. Traders are now pricing in two or more rate cuts from the ECB before year-end, even as sentiment toward the euro remains broadly positive amid rising skepticism about dollar dominance and expectations for increased German defense spending.

EURUSD, USDJPY & AUDUSD price dynamics. Source: TradingView.

Yen weakens as Tokyo inflation jumps and dollar sentiment improves

The Japanese yen fell to around 143 per dollar, giving up gains from the previous session. A stronger greenback, buoyed by easing trade war fears and Trump's softened tone on Powell, weighed on the safe-haven currency. Reports of ongoing negotiations between the U.S. and China, along with progress in talks with Japan and South Korea, helped boost risk sentiment and U.S. dollar demand.

Domestically, Tokyo’s core inflation rose to a two-year high of 3.4% in April, complicating the Bank of Japan’s monetary stance. The central bank is widely expected to hold rates steady next week as it navigates between rising price pressures and external economic risks stemming from tariff shifts.

Aussie dollar slips despite strong domestic data

The Australian dollar slipped below $0.64, reversing gains from earlier in the week. Despite upbeat local data showing a seventh straight month of private sector expansion in April, expectations of a 25 basis point rate cut from the Reserve Bank of Australia in May, coupled with renewed U.S. dollar strength, kept the Aussie under pressure. Positive trade rhetoric from the White House, particularly regarding China and other regional allies, has shifted investor preference back toward the dollar.

As noted in earlier coverage, the euro remains supported by shifting global currency preferences and ECB policy moderation. Meanwhile, the yen and Australian dollar face structural headwinds from external policy risks and diverging monetary expectations.