Federal Reserve Outlook

Editorial Note: While we adhere to strict Editorial Integrity, this post may contain references to products from our partners. Here's an explanation for How We Make Money. None of the data and information on this webpage constitutes investment advice according to our Disclaimer.

The Federal Reserve outlook depends on balancing its two mandates: price stability and maximum employment. While inflation pressures remain a concern, signs of slowing job growth often push the Fed toward cutting rates. In addition, the central bank continues to manage its balance sheet through Quantitative Tightening, aiming to keep reserves at a “sufficiently ample” level. Overall, the Fed’s path combines cautious easing with close monitoring of inflation, employment, and financial stability.

A consensus has emerged that the Federal Reserve will resume its rate-cutting cycle this month. The cycle began last September but stalled this year. Federal Reserve Chair Powell explained that the administration’s tariffs, which are higher than nearly anyone anticipated, have thrown a wrench into the works. If not for the tariffs, Powell suggested, the Fed would likely have continued reducing rates.

Yet what will ultimately get the Fed to resume its easing cycle is not subdued inflation. On the contrary, price pressures remain troublesome. Core CPI rose above 3% for the first time since early this year, and producer prices (which do include some consumer prices, despite the name) are also elevated.

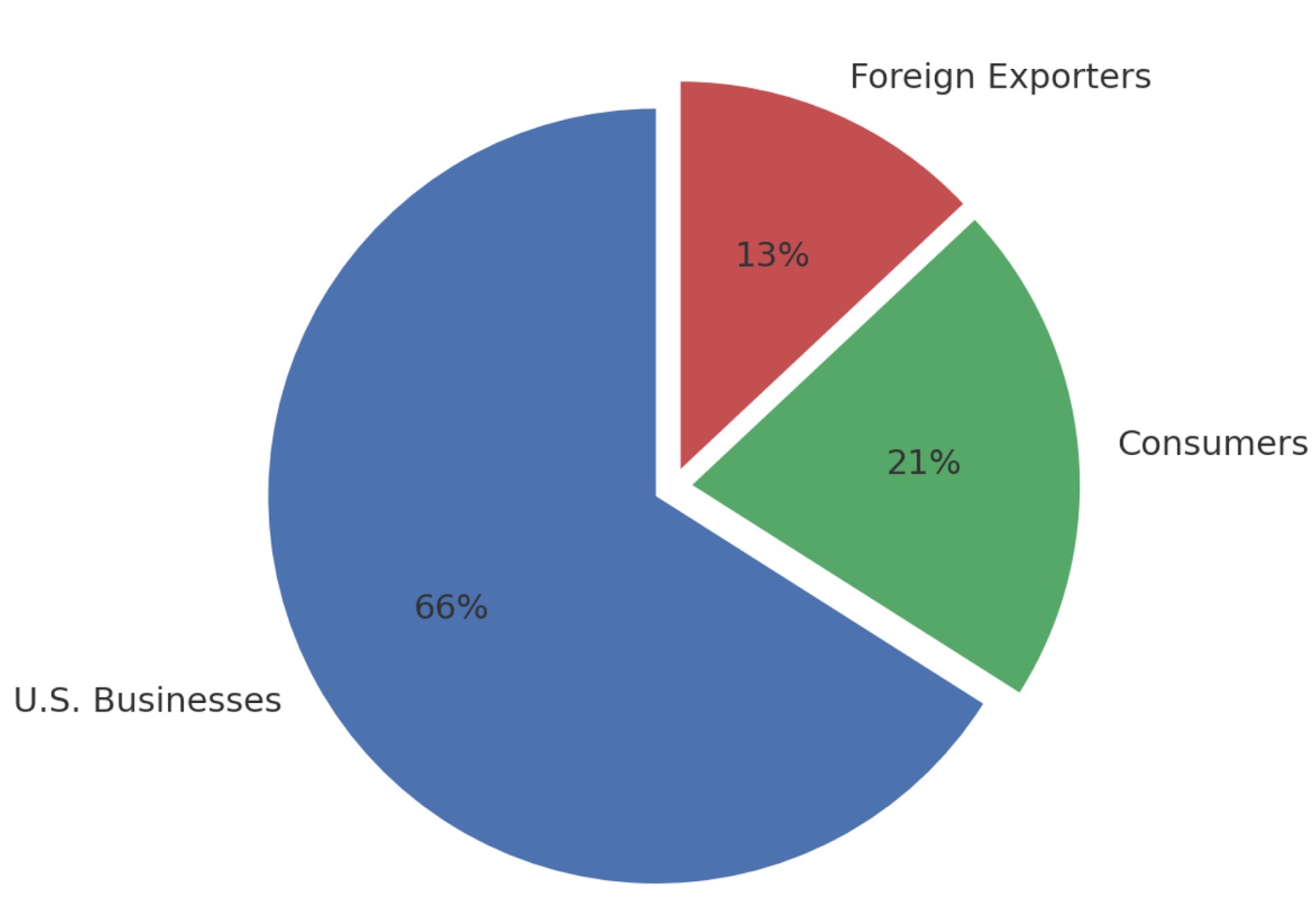

According to Goldman Sachs economists, U.S. businesses are absorbing almost two-thirds of the tariff increases, while consumers are bearing a little more than a fifth. The remainder is absorbed by foreign exporters. However, they expect the burden to shift in the coming months – more to U.S. consumers and foreign businesses, while U.S. companies succeed in reducing the impact on themselves.

Dual mandate

Even though the Fed is not seeing progress toward its inflation target, its other mandate, full employment, is deteriorating. To be sure, it has been gradually slowing, but the weakness of the July jobs data, coupled with steep downward back-month revisions, has changed the game.

A couple of days before the July nonfarm payrolls (and revisions) were announced, two Federal Reserve Governors, Waller and Bowman, dissented from the FOMC’s decision to stand pat. They warned that job growth was stalling and that tariff-related price pressures were temporary. Despite the dissents – the first time two governors dissented in slightly more than three decades – the market insisted that it was a “hawkish hold” and took U.S. rates and the dollar higher.

The market was caught leaning the wrong way. The jobs data on August 1 snapped the greenback’s rally that began on July 1. In August, U.S. rates resumed their decline, and so did the U.S. dollar. It did not help that following the jobs news, President Trump cast aspersions on the data and dismissed the head of the Bureau of Labor Statistics, responsible for the jobs report (and CPI).

ADP, which provides payroll services to many U.S. businesses, offers an estimate of private-sector employment changes. Although it says that it is not designed to predict the government’s estimate, it has done a fairly good job of doing precisely that.

Consider that in the first eight months of the year, ADP estimated that the private sector added an average of 80.9k jobs a month, compared with a little more than 117k jobs a month in the same period last year. Including revisions, BLS data estimates the private sector created an average of 74k jobs a month this year and 103k a month in the first eight months of 2024.

Powell explained at the press conference following the last FOMC meeting that the unemployment rate itself is the key metric in the current circumstances. The Fed Chair argued that the supply of labor has weakened (immigration policy) while demand has slackened. The unemployment rate shows the relative strength of the two forces.

Machinations

Federal Reserve Board Governor Adriana Kugler, whose term ends in January 2026, stepped down early. President Trump nominated Stephen Miran, an economic adviser, to finish her term. Hers could be the only seat Trump can nominate someone for until very late in his second term.

However, a new angle emerged in August. The head of the Federal Housing Finance Agency accused Governor Lisa Cook of falsifying claims on mortgage applications prior to her appointment to the Federal Reserve. President Trump fired her on the accusations, and Cook sought legal recourse. The case was heard in late August, but the decision has not been rendered, and regardless of the outcome, it will likely be appealed.

If President Trump succeeds, it will possibly give him greater influence at the Federal Reserve. Not only would he be able to nominate a replacement for Cook, but through his appointments he may be able to influence the choice of regional presidents. The Fed’s regional presidents are chosen by their own boards, but the final decision requires approval from the Board of Governors. Recall that Governors Waller and Bowman abstained rather than support Austan Goolsbee as President of the Chicago Federal Reserve, but they did not have the votes to block him. While the Board of Governors has never vetoed a regional pick, this example shows that it need not be a rubber stamp.

There is also intrigue about the chair. Powell’s term as chair, to which Trump appointed him in his first term – claiming Yellen was too short – ends in May 2026. However, Powell’s term as governor extends through January 2028. While it is customary for the chair to resign from the Federal Reserve Board when the chair’s term ends, it is not a legal requirement but a tradition. And we have seen what the administration thinks of tradition.

Trump is expected to nominate Powell’s successor early compared to recent history. Some have suggested a “shadow” chair could also add to the pressure on the Federal Reserve. If the president’s nomination for the next chair is outside the pale or seen as risking the independence of the central bank, the suspicion is that Powell will consider staying on as governor. The challenge to Cook would seem to boost the chances that Powell fulfills his term as governor.

The decision

The Federal Reserve will do two, and possibly three, things at its September 17 meeting. First, it will reduce the restrictiveness of the current policy setting by lowering the Fed funds target rate to 4.00%–4.25% from 4.25%–4.50%. Speculation of a 50 bp cut seems exaggerated given the elevated price pressures.

Second, it will update the Summary of Economic Projections. Recall that rather than have a specific Fed forecast, the Federal Reserve surveys the governors and regional presidents and publishes the range of projections and the median.

In June, the median forecast for growth this year was 1.4%, 1.6% next year, and 1.8% in 2027. The PCE deflator, which the Fed targets, was seen at 3.0% this year, 2.4% next year, and 2.1% in 2027. The median forecast for unemployment was 4.5% this year and next before slipping to 4.4% in 2027.

In terms of the policy rate, the median “dot” anticipated two cuts this year and one more next year. However, the dispersion next year was particularly wide, ranging from 2.63% to 4.14%. We suspect there is scope for next year’s median (3.625%) to fall by as much as 25 bp. The Fed funds futures see the effective Fed funds rate (weighted average) near 3.0% at the end of next year (from 4.33% currently).

The Balance sheet

Third, the Federal Reserve may give some guidance on its Quantitative Tightening process. Recall that the Federal Reserve is not actively selling securities from its portfolio. Rather, it is simply not replacing maturing issues at a pace of about $95 billion a month ($60 billion of U.S. Treasuries and $35 billion of mortgage-backed securities). The decline in the usage of the Fed’s reverse repo facility may be a sign that reserves are reaching a level officials will regard as “sufficiently ample.” In 2019, it appears they waited too long and had to inject more reserves into the banking system. Explore whether “money on the sidelines” is a myth and how the movement of Fed reverse repos and M2 velocity shapes true monetary stimulus.

If reserves fall too far, it could destabilize the short end of the curve. Several Fed officials have also indicated that in the long term, it is desirable to hold only Treasuries on the balance sheet. The Federal Reserve’s balance sheet peaked at about $8.94 trillion in April 2022. As of the end of August, it stood at $6.60 trillion. Before the pandemic and the 2019 interventions, the balance sheet was $3.76 trillion. Before the Great Financial Crisis (GFC), the Fed’s balance sheet was less than $1 trillion.

Before the GFC, the Fed’s balance sheet was 5.8%–6.0% of GDP. It peaked in late 2014, around 25.3% of GDP. It bottomed five years later near 17.5% of GDP. During the emergency response to the pandemic, it peaked in late 2021 at 36.8% of GDP and now stands near 22.2% of GDP.

It is as if during the Great Depression and WWII, the federal government levered its balance sheet. It continues to use it, of course, but starting with the GFC, it was insufficient, and the central bank’s balance sheet was harnessed to the task.

FAQs

Why does the Fed’s independence matter for markets?

The Federal Reserve’s independence ensures decisions are based on economic data rather than political pressure. If independence weakens, investors may fear short-term political goals outweigh long-term stability.

How do tariffs influence monetary policy beyond inflation?

Tariffs not only raise prices but also disrupt supply chains, reduce investment, and shift global trade flows. The Fed must consider these second-order effects when setting policy.

What role do Fed governors play compared to regional presidents?

Governors are appointed by the president and confirmed by the Senate, while regional presidents are chosen locally but require Board approval. This mix balances national oversight with regional perspectives.

How do changes in the Fed funds rate affect global currencies?

Lower rates typically weaken the U.S. dollar by reducing returns on U.S. assets, but global risk sentiment and capital flows can override this effect in the short term.

Editors' Top Picks and Insights

Crypto test drive: How automakers are exploring digital assets

Lindsey Graham death: U.S. senator’s crypto legacy

Tether under pressure: USDT in Europe, audit questions, and the fight for trust

Lean Ethereum: Why Buterin wants to rebuild the network

SK Hynix debuts on Nasdaq: Largest U.S. offering by foreign company

SpaceX falls out of orbit: Does anyone still want Musk’s stock?

Related Articles

Team that worked on the article

One of the most widely respected and quoted currency experts, Marc Chandler has been analyzing and advising on the global capital markets for more than 30 years. Throughout his career on Wall Street, Chandler has advised private businesses, hedge funds and asset managers on navigating the foreign exchange market.

Dan Blystone began his trading career in 1998 as an arbitrage clerk on the floor of the Chicago Mercantile Exchange (CME). He later traded bond and Eurex futures at proprietary firms such as Altea Trading, gaining valuable experience in high-frequency trading and risk management.

Chinmay Soni is a financial analyst with more than 5 years of experience in working with stocks, Forex, derivatives, and other assets. As a founder of a boutique research firm and an active researcher, he covers various industries and fields, providing insights backed by statistical data.

CFD is a contract between an investor/trader and seller that demonstrates that the trader will need to pay the price difference between the current value of the asset and its value at the time of contract to the seller.

Risk management is a risk management model that involves controlling potential losses while maximizing profits. The main risk management tools are stop loss, take profit, calculation of position volume taking into account leverage and pip value.

Index in trading is the measure of the performance of a group of stocks, which can include the assets and securities in it.

Bitcoin is a decentralized digital cryptocurrency that was created in 2009 by an anonymous individual or group using the pseudonym Satoshi Nakamoto. It operates on a technology called blockchain, which is a distributed ledger that records all transactions across a network of computers.

Ethereum is a decentralized blockchain platform and cryptocurrency that was proposed by Vitalik Buterin in late 2013 and development began in early 2014. It was designed as a versatile platform for creating decentralized applications (DApps) and smart contracts.

-

Afghanistan

Afghanistan

-

Albania

Albania

-

Algeria

Algeria

-

Angola

Angola

-

Argentina

Argentina

-

Armenia

Armenia

-

Australia

Australia

-

Austria

Austria

-

Azerbaijan

Azerbaijan

-

Bahamas

Bahamas

-

Bahrain

Bahrain

-

Bangladesh

Bangladesh

-

Belarus

Belarus

-

Belgium

Belgium

-

Bolivia

Bolivia

-

Botswana

Botswana

-

Brazil

Brazil

-

Brunei

Brunei

-

Bulgaria

Bulgaria

-

Cambodia

Cambodia

-

Cameroon

Cameroon

-

Canada

Canada

-

Chile

Chile

-

China

China

-

Colombia

Colombia

-

Congo

Congo

-

Costa Rica

Costa Rica

-

Cote d'Ivoire

Cote d'Ivoire

-

Croatia

Croatia

-

Cuba

Cuba

-

Cyprus

Cyprus

-

Czechia

Czechia

-

DR Congo

DR Congo

-

Denmark

Denmark

-

Dominican Republic

Dominican Republic

-

Ecuador

Ecuador

-

Egypt

Egypt

-

El Salvador

El Salvador

-

Estonia

Estonia

-

Eswatini

Eswatini

-

Ethiopia

Ethiopia

-

Finland

Finland

-

France

France

-

Georgia

Georgia

-

Germany

Germany

-

Ghana

Ghana

-

Greece

Greece

-

Haiti

Haiti

-

Hong Kong

Hong Kong

-

Hungary

Hungary

-

India

India

-

Indonesia

Indonesia

-

Iran, Islamic republic

Iran, Islamic republic

-

Iraq

Iraq

-

Ireland

Ireland

-

Israel

Israel

-

Italy

Italy

-

Jamaica

Jamaica

-

Japan

Japan

-

Jordan

Jordan

-

Kazakhstan

Kazakhstan

-

Kenya

Kenya

-

Korea

Korea

-

Kuwait

Kuwait

-

Kyrgyzstan

Kyrgyzstan

-

Laos

Laos

-

Latvia

Latvia

-

Lebanon

Lebanon

-

Lesotho

Lesotho

-

Libya

Libya

-

Lithuania

Lithuania

-

Luxembourg

Luxembourg

-

Madagascar

Madagascar

-

Malaysia

Malaysia

-

Malta

Malta

-

Mauritius

Mauritius

-

Mexico

Mexico

-

Moldova

Moldova

-

Mongolia

Mongolia

-

Montenegro

Montenegro

-

Morocco

Morocco

-

Mozambique

Mozambique

-

Myanmar

Myanmar

-

Namibia

Namibia

-

Nepal

Nepal

-

Netherlands

Netherlands

-

New Zealand

New Zealand

-

Nigeria

Nigeria

-

North Macedonia

North Macedonia

-

Norway

Norway

-

Oman

Oman

-

Pakistan

Pakistan

-

Palestine

Palestine

-

Panama

Panama

-

Papua New Guinea

Papua New Guinea

-

Paraguay

Paraguay

-

Peru

Peru

-

Philippines

Philippines

-

Poland

Poland

-

Portugal

Portugal

-

Puerto Rico

Puerto Rico

-

Qatar

Qatar

-

Reunion

Reunion

-

Romania

Romania

-

Rwanda

Rwanda

-

Saudi Arabia

Saudi Arabia

-

Serbia

Serbia

-

Singapore

Singapore

-

Slovakia

Slovakia

-

Slovenia

Slovenia

-

Somalia

Somalia

-

South Africa

South Africa

-

Spain

Spain

-

Sri Lanka

Sri Lanka

-

Sweden

Sweden

-

Switzerland

Switzerland

-

Syria

Syria

-

Taiwan

Taiwan

-

Tajikistan

Tajikistan

-

Tanzania

Tanzania

-

Thailand

Thailand

-

Trinidad and Tobago

Trinidad and Tobago

-

Tunisia

Tunisia

-

Turkey

Turkey

-

UAE

UAE

-

Uganda

Uganda

-

Ukraine

Ukraine

-

United Kingdom

United Kingdom

-

United States

-

Uruguay

Uruguay

-

Uzbekistan

Uzbekistan

-

Venezuela

Venezuela

-

Vietnam

Vietnam

-

Yemen

Yemen

-

Zambia

Zambia

-

Zimbabwe

Zimbabwe

- Forex

- Crypto