Money On The Sidelines Is Not What You Think

Editorial Note: While we adhere to strict Editorial Integrity, this post may contain references to products from our partners. Here's an explanation for How We Make Money. None of the data and information on this webpage constitutes investment advice according to our Disclaimer.

“Money on the sidelines” doesn’t literally exist – every dollar is always held by someone. When cash leaves the Fed’s reverse repo facility and flows into money markets or banks, it doesn’t increase M2 but can stimulate markets by becoming more active. The difference is not in how much money exists, but in how fast it circulates.

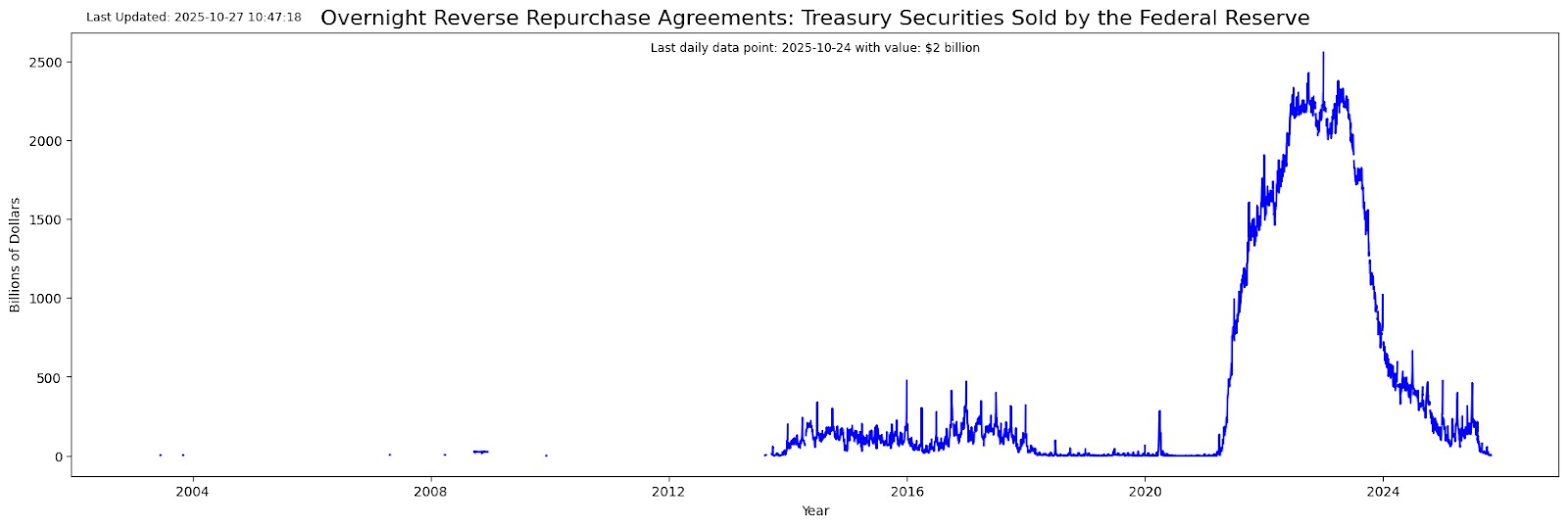

When people talk about “money on the sidelines,” they imply there’s a pile of cash that’s been sitting out the rally and is now ready to flood into markets. It’s a comforting image – but misleading. There’s nuance hidden behind the phrase, especially now that the Federal Reserve’s Overnight Reverse Repo Facility (ON RRP) has effectively gone to zero.

The Mechanics: what the Reverse Repo market really is

The ON RRP is a tool the Federal Reserve uses to absorb short-term liquidity. In a reverse repo, money-market funds and other institutions lend cash to the Fed overnight in exchange for Treasury collateral. The next day, the Fed repays the cash plus interest at the RRP rate.

It’s essentially a safe overnight parking lot for cash – guaranteed by the Fed. When the Fed’s rate is attractive, trillions flow in; when it’s not, the funds leave.

After 2021’s massive pandemic stimulus and Fed asset purchases (QE), the facility ballooned to $2.5 trillion. As the Fed pivoted to quantitative tightening (QT) – letting maturing Treasuries and MBS roll off – the ON RRP balance collapsed to near zero. The latest figures show only $2 billion remaining, a rounding error.

Where the money went

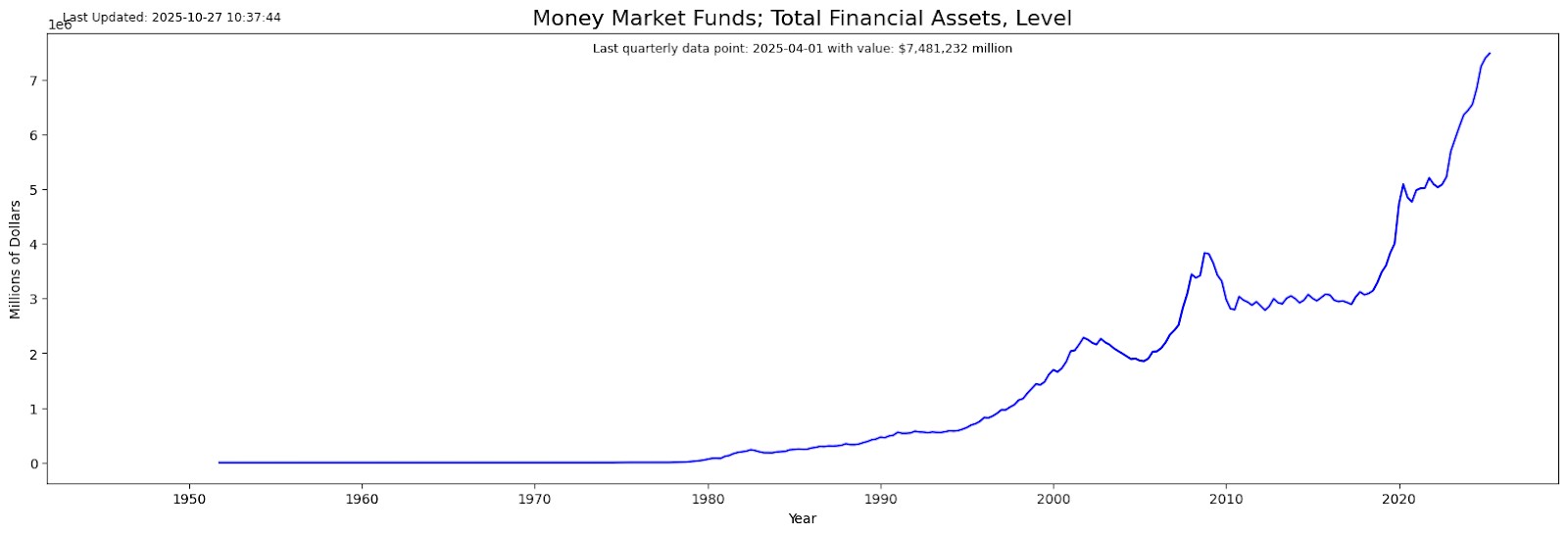

As the RRP drained, money-market fund assets surged to roughly $7.5 trillion. This sparked the “money on the sidelines” chatter – especially among market bulls arguing that this cash will soon power equities higher.

But to test that claim, we need to understand whether this shift actually creates new money or simply moves it.

John Hussman’s perspective: the identity problem

Economist Dr. John Hussman famously wrote:

“There is no such thing as money going into or out of the market – only a change in who holds it.”

He’s right in a strict accounting sense. When an investor buys a stock, cash moves from buyer → seller, not into or out of “the market.” The total amount of cash in the system remains constant.

Similarly, when money-market funds placed cash in the ON RRP, they simply exchanged one claim (bank reserves) for another (a Fed reverse repo). Both are money-like assets, just different pockets of the same system.

So yes, as Hussman insists – there are no sidelines. Every dollar is always held by someone.

The behavioral counterpoint: where the identity fails

While Hussman’s identity is logically true, it’s behaviorally incomplete.

When cash moves into the RRP, it becomes inert – locked up at the Fed.

When it moves back out into T-bills, repos, or deposits, it becomes active, influencing rates and risk appetite.

So even though the quantity of money (M2) doesn’t change, its velocity – how quickly it circulates – does. That’s the subtle but powerful distinction between a balance-sheet identity and a monetary stimulus.

M2 and velocity

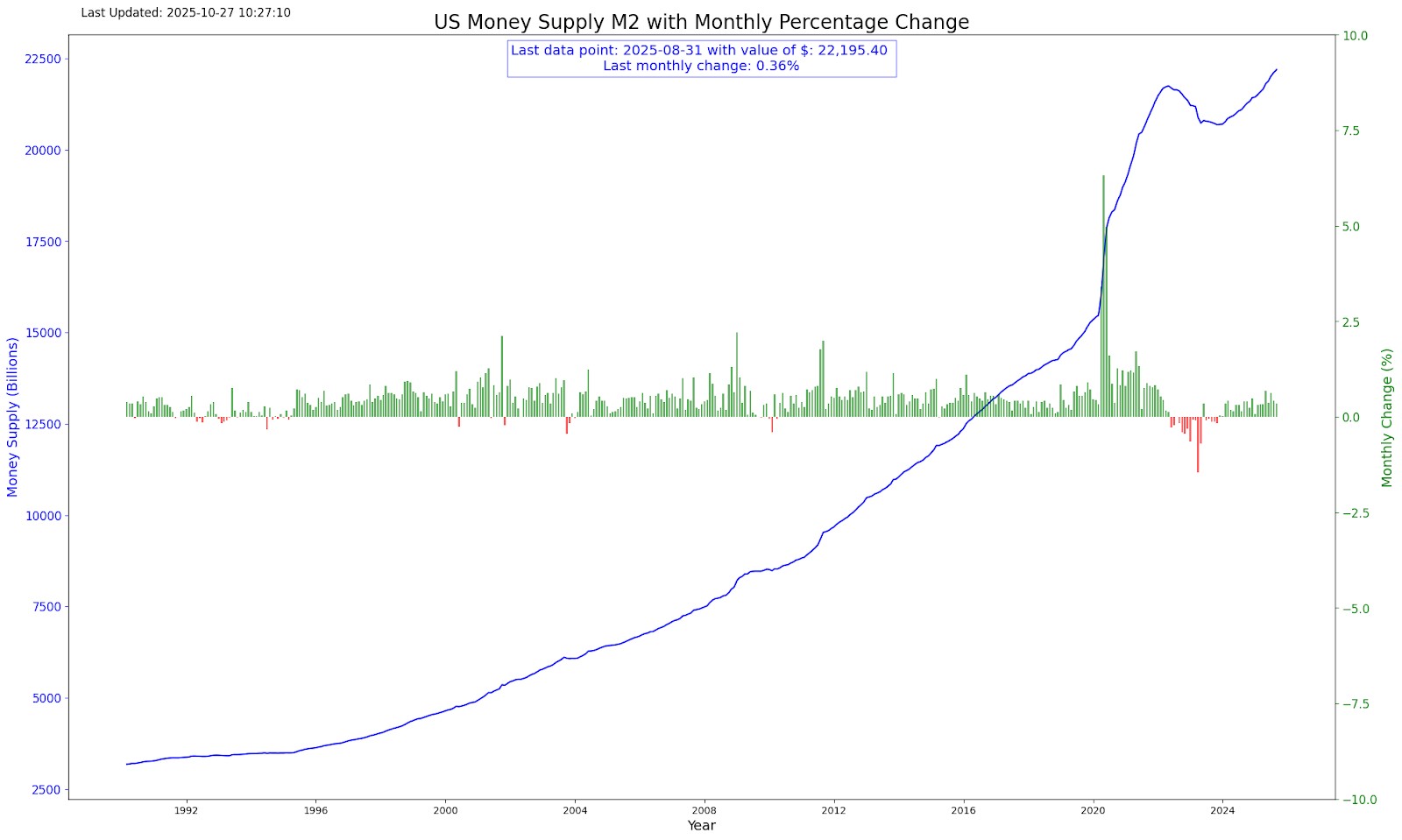

M2 includes currency in circulation, bank deposits, and retail money-market funds – but not the institutional money funds that dominate RRP activity. Therefore, when cash leaves the RRP and returns to institutional MMFs, M2 doesn’t rise. It’s a reshuffling of liquidity, not a creation of new money.

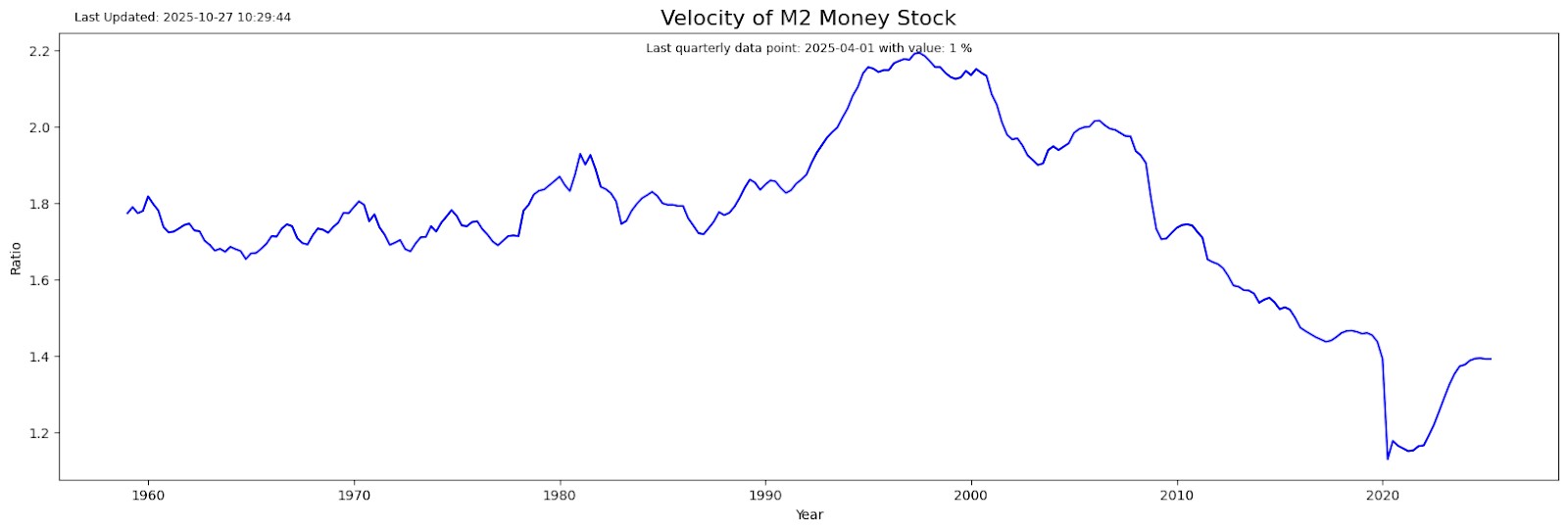

However, velocity – how fast that money turns over – can still change. Since 2000, velocity has fallen sharply, even as M2 exploded. The economy grew, but each dollar was used fewer times because stimulus increasingly came from debt expansion, not spending activity.

After the pandemic, velocity briefly rebounded as stimulus cash circulated – but it’s recently plateaued. This plateau signals that while liquidity remains abundant, its willingness to move is what matters most.

A logical identity meets human behavior

Hussman’s statement – “every dollar is always held by someone” – is an accounting identity, like saying a light switch is either on or off. Always true, but not always useful.

Economics happens in the space between those states – between money sitting and money moving. The difference is not semantic; it’s functional. Liquidity sitting in the Fed’s vault behaves very differently from liquidity chasing yield in credit markets.

Getting off the sidelines: a practical view

In reality, there’s nothing stopping the money sitting idly in reserves or MMFs from being re-lent, re-invested, or spent, increasing velocity even without expanding M2. This is the bridge between Hussman’s logic and market behavior.

So while there’s no mythical pile of “new money” waiting to rush in, there is potential energy within the system – liquidity that can shift from idle to active when confidence, yields, or risk appetite change.

The bulls are wrong that a cash avalanche is guaranteed, but the bears are wrong to think it can’t happen. The truth is latent liquidity – always present, occasionally unleashed.

The semantics are real, but so are the consequences

As someone who has spent decades in both research and trading, I’ve seen how seductive neat theories can be – whether it’s the perfect backtest or the tidy accounting identity. The danger lies in believing that technical accuracy equals predictive power. Dr. Hussman is right that there are no sidelines in a closed system, but markets are not governed solely by balance sheets; they’re driven by behavior, confidence, and institutional plumbing.

What matters is where liquidity rests and how fast it moves. When the Fed’s ON RRP drained from trillions to nearly zero, that shift didn’t change M2, but it changed the emotional temperature of markets – the willingness to take risk. Recognizing that distinction is critical for investors and policymakers alike. Monetary mechanics describe the stage, but velocity and psychology decide the play.

In short: the semantics are real, but so are the consequences.

Conclusion

The notion of 'money on the sidelines' is less a reflection of untapped market fuel and more a semantic misunderstanding of how monetary flows operate. Federal Reserve reverse repos and the stagnation of M2 velocity underscore that idle balances do not, on their own, constitute pent-up demand ready to flood markets. As John Hussman’s logic reminds investors, true stimulus comes from an increase in the willingness to spend or invest, not merely the presence of unused cash. For instance, a rise in bank reserves during 2020 did little to accelerate velocity or equity markets until sentiment shifted. Ultimately, scrutinizing the mechanics—rather than the myth—of sidelined money offers a stronger grasp of what truly moves markets.

FAQs

How does the velocity of money impact market behavior compared to the total money supply?

What happens to financial markets when liquidity shifts from idle to active use?

Why is understanding both monetary mechanics and human behavior essential for interpreting market trends?

Can latent liquidity in the system lead to sudden changes in market conditions?

Editors' Top Picks and Insights

Crypto test drive: How automakers are exploring digital assets

Lindsey Graham death: U.S. senator’s crypto legacy

Tether under pressure: USDT in Europe, audit questions, and the fight for trust

Lean Ethereum: Why Buterin wants to rebuild the network

SK Hynix debuts on Nasdaq: Largest U.S. offering by foreign company

SpaceX falls out of orbit: Does anyone still want Musk’s stock?

Related Articles

Team that worked on the article

Andrey Mastykin is an experienced author, editor, and content strategist who has been with Traders Union since 2020. As an editor, he is meticulous about fact-checking and ensuring the accuracy of all information published on the Traders Union platform.

Dan Blystone began his trading career in 1998 as an arbitrage clerk on the floor of the Chicago Mercantile Exchange (CME). He later traded bond and Eurex futures at proprietary firms such as Altea Trading, gaining valuable experience in high-frequency trading and risk management.

Chinmay Soni is a financial analyst with more than 5 years of experience in working with stocks, Forex, derivatives, and other assets. As a founder of a boutique research firm and an active researcher, he covers various industries and fields, providing insights backed by statistical data.

Index in trading is the measure of the performance of a group of stocks, which can include the assets and securities in it.

Yield refers to the earnings or income derived from an investment. It mirrors the returns generated by owning assets such as stocks, bonds, or other financial instruments.

Bitcoin is a decentralized digital cryptocurrency that was created in 2009 by an anonymous individual or group using the pseudonym Satoshi Nakamoto. It operates on a technology called blockchain, which is a distributed ledger that records all transactions across a network of computers.

Ethereum is a decentralized blockchain platform and cryptocurrency that was proposed by Vitalik Buterin in late 2013 and development began in early 2014. It was designed as a versatile platform for creating decentralized applications (DApps) and smart contracts.

Risk management is a risk management model that involves controlling potential losses while maximizing profits. The main risk management tools are stop loss, take profit, calculation of position volume taking into account leverage and pip value.

-

Afghanistan

Afghanistan

-

Albania

Albania

-

Algeria

Algeria

-

Angola

Angola

-

Argentina

Argentina

-

Armenia

Armenia

-

Australia

Australia

-

Austria

Austria

-

Azerbaijan

Azerbaijan

-

Bahamas

Bahamas

-

Bahrain

Bahrain

-

Bangladesh

Bangladesh

-

Belarus

Belarus

-

Belgium

Belgium

-

Bolivia

Bolivia

-

Botswana

Botswana

-

Brazil

Brazil

-

Brunei

Brunei

-

Bulgaria

Bulgaria

-

Cambodia

Cambodia

-

Cameroon

Cameroon

-

Canada

Canada

-

Chile

Chile

-

China

China

-

Colombia

Colombia

-

Congo

Congo

-

Costa Rica

Costa Rica

-

Cote d'Ivoire

Cote d'Ivoire

-

Croatia

Croatia

-

Cuba

Cuba

-

Cyprus

Cyprus

-

Czechia

Czechia

-

DR Congo

DR Congo

-

Denmark

Denmark

-

Dominican Republic

Dominican Republic

-

Ecuador

Ecuador

-

Egypt

Egypt

-

El Salvador

El Salvador

-

Estonia

Estonia

-

Eswatini

Eswatini

-

Ethiopia

Ethiopia

-

Finland

Finland

-

France

France

-

Georgia

Georgia

-

Germany

Germany

-

Ghana

Ghana

-

Greece

Greece

-

Haiti

Haiti

-

Hong Kong

Hong Kong

-

Hungary

Hungary

-

India

India

-

Indonesia

Indonesia

-

Iran, Islamic republic

Iran, Islamic republic

-

Iraq

Iraq

-

Ireland

Ireland

-

Israel

Israel

-

Italy

Italy

-

Jamaica

Jamaica

-

Japan

Japan

-

Jordan

Jordan

-

Kazakhstan

Kazakhstan

-

Kenya

Kenya

-

Korea

Korea

-

Kuwait

Kuwait

-

Kyrgyzstan

Kyrgyzstan

-

Laos

Laos

-

Latvia

Latvia

-

Lebanon

Lebanon

-

Lesotho

Lesotho

-

Libya

Libya

-

Lithuania

Lithuania

-

Luxembourg

Luxembourg

-

Madagascar

Madagascar

-

Malaysia

Malaysia

-

Malta

Malta

-

Mauritius

Mauritius

-

Mexico

Mexico

-

Moldova

Moldova

-

Mongolia

Mongolia

-

Montenegro

Montenegro

-

Morocco

Morocco

-

Mozambique

Mozambique

-

Myanmar

Myanmar

-

Namibia

Namibia

-

Nepal

Nepal

-

Netherlands

Netherlands

-

New Zealand

New Zealand

-

Nigeria

Nigeria

-

North Macedonia

North Macedonia

-

Norway

Norway

-

Oman

Oman

-

Pakistan

Pakistan

-

Palestine

Palestine

-

Panama

Panama

-

Papua New Guinea

Papua New Guinea

-

Paraguay

Paraguay

-

Peru

Peru

-

Philippines

Philippines

-

Poland

Poland

-

Portugal

Portugal

-

Puerto Rico

Puerto Rico

-

Qatar

Qatar

-

Reunion

Reunion

-

Romania

Romania

-

Rwanda

Rwanda

-

Saudi Arabia

Saudi Arabia

-

Serbia

Serbia

-

Singapore

Singapore

-

Slovakia

Slovakia

-

Slovenia

Slovenia

-

Somalia

Somalia

-

South Africa

South Africa

-

Spain

Spain

-

Sri Lanka

Sri Lanka

-

Sweden

Sweden

-

Switzerland

Switzerland

-

Syria

Syria

-

Taiwan

Taiwan

-

Tajikistan

Tajikistan

-

Tanzania

Tanzania

-

Thailand

Thailand

-

Trinidad and Tobago

Trinidad and Tobago

-

Tunisia

Tunisia

-

Turkey

Turkey

-

UAE

UAE

-

Uganda

Uganda

-

Ukraine

Ukraine

-

United Kingdom

United Kingdom

-

United States

-

Uruguay

Uruguay

-

Uzbekistan

Uzbekistan

-

Venezuela

Venezuela

-

Vietnam

Vietnam

-

Yemen

Yemen

-

Zambia

Zambia

-

Zimbabwe

Zimbabwe

- Forex

- Crypto

- The Mechanics: what the Reverse Repo market really is

- Where the money went

- John Hussman’s perspective: the identity problem

- The behavioral counterpoint: where the identity fails

- M2 and velocity

- A logical identity meets human behavior

- Getting off the sidelines: a practical view

- Expert opinion

- Conclusion

- FAQs