What Is Cashback On A Credit Card? Full Guide For Traders

Editorial Note: While we adhere to strict Editorial Integrity, this post may contain references to products from our partners. Here's an explanation for How We Make Money. None of the data and information on this webpage constitutes investment advice according to our Disclaimer.

Cashback on credit cards allows you to earn a percentage of your spending back, typically between 1% and 6%. This reward is funded by merchant interchange fees (usually 1.5% to 3%) collected on every transaction. For example, spending $2,000 a month on a card offering 2% cashback could earn you around $480 a year. The rewards are flexible and can be redeemed as a statement credit, direct deposit, or gift card. Unlike points, cashback is straightforward, liquid, and not taxable. For many, it’s a simple and effective way to cut costs or reinvest extra funds.

Every swipe has the potential to build value. Cashback is essentially a financial reward program from credit card issuers, where a portion of your spending is returned to you. So, if you’ve asked yourself “how does cashback work on credit cards,” think of it as a trade-off: the card issuer earns revenue from merchants and shares part of it with the cardholder. While it may seem like a small perk, the rewards can add up to a meaningful return over time.

To most consumers, cashback feels like an easy way to save. But for active traders and disciplined budgeters, it can function as a tool for building liquidity. Redirecting cashback rewards toward investments or emergency savings helps strengthen financial buffers. In fact, Americans held about $1.3 trillion in credit card debt by late 2024; this level persisted into mid-2025. That’s a massive pool of opportunity, especially for those who understand what cashback for credit cards is and use it as part of a broader return-on-investment strategy. This guide walks you through how it works, why it matters, and how to make it part of your financial playbook.

What is cashback on a credit card?

Let’s break down what a cashback credit card's meaning really is, and how choosing the right structure can benefit your wallet.

Understanding cashback in simple terms

Cashback is a perk where you get a percentage of your spending back, usually in dollars, based on eligible purchases. Think of it as a small, ongoing discount every time you use your card.

How cashback is delivered

Statement credits. The amount you earn directly reduces your card balance.

Direct deposits. Some cards deposit your rewards straight into your bank account.

Gift card redemptions: Others let you swap your earnings for store or other retailer gift cards.

How cashback differs from other rewards

Unlike points or miles, where value depends on redemption options, cashback is straightforward. You know exactly what you’ve earned and how much it’s worth, no math required.

| Cashback Model | Example Card | Rate | Annual Return on $24,000 spend | Pros | Cons |

|---|---|---|---|---|---|

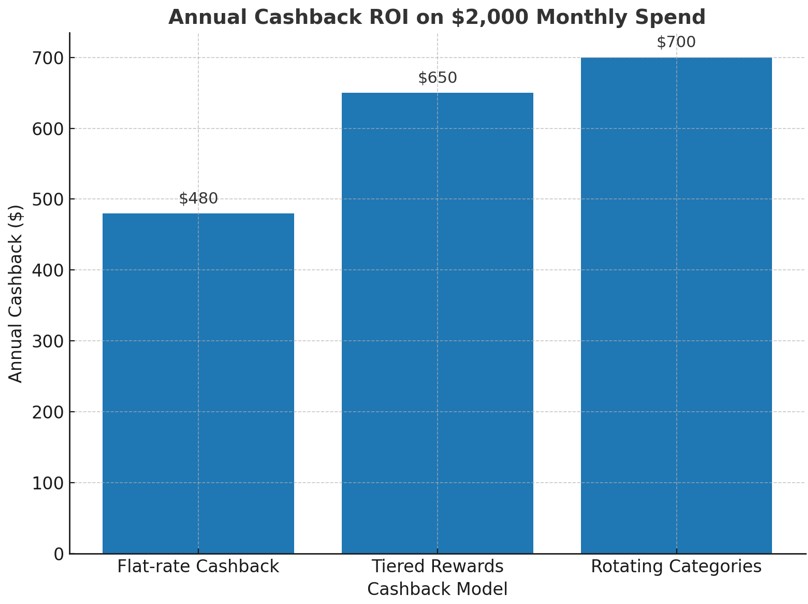

| Flat-rate cashback | Citi Double Cash | 2% total: 1% at purchase + 1% on payment | $480 (24,000 × 0.02) | Simple, no caps, no tracking | No category boosts |

| Tiered rewards credit card | AMEX Blue Cash Preferred | 6% on up to $6,000 groceries & streaming; 3% on gas & transit; 1% all else | ~$660 (assuming $6,000 groceries: $360 + $300 other) * | High rates in key categories | $95 annual fee after year 1; grocer cap; AmEx isn’t widely accepted | | Strong bonus on common categories | $95 annual fee, merchant acceptance |

| Rotating category cashback | Chase Freedom Flex | 5% on up to $1,500 per quarter (activated), plus 3% dining/drugstores, 1% elsewhere | $300 + $720 = $1,020 (maxing 5% × 6 quarters + 3% × $6,000) † | High earning potential in bonus quarters | Caps ($1,500/quarter), activation req. |

How does cashback work on credit cards?

If you’re wondering how banks can pay you for swiping plastic, here’s the secret: merchant fees are the engine, and smart structuring lets you benefit. Savvy use of tiered rewards credit cards, rotating category cashback, and selecting among the best cashback cards in the USA can meaningfully boost your returns.

Behind-the-scenes mechanics

When you spend, the merchant pays a “swipe fee”, part of which is the interchange fee with issuing banks. These fees (usually around 1 to 3% per transaction) help fund rewards programs, especially when using premium or high-earning cards. Companies like American Express keep more of the fee because they act as both issuer and payment network, enabling them to give richer rewards.

How cashback models differ

Flat-rate cashback. Earn a steady return (like 2%) on every purchase; simple to maximize.

Tiered category rewards. Get extra back in groceries, gas, or dining (e.g., 5%), and less elsewhere.

Rotating categories. You earn big rewards in categories that change quarterly; think Chase Freedom-style, where planning your spending pays off.

Tools for smarter card picks

Comparing actual take-home benefits is eye-opening. Put your spending into a chart that calculates true annual return across top cards; best cashback cards in the USA can yield 1–5% overall depending on your patterns. Use this to refine your trader strategy and manage downside surprises. Earn cashback with Apple Pay on everyday purchases by linking eligible cards and using Apple devices at supported retailers and apps.

Why cashback matters to traders

Trading is ultimately about return on investment, and cashback programs apply that same logic to everyday spending. For traders, these rewards can serve multiple purposes:

Covering monthly platform or tool subscriptions (often ranging from $50 to $100).

Helping build a small emergency fund without dipping into trading capital.

Creating a consistent, passive stream that can be reinvested for long-term benefits.

For example, spending $2,000 a month on a card offering 2% back results in $480 annually. If you're holding $30,000 in idle funds, that’s effectively a 1.6% return, similar to short-term Treasury yields. But to fully benefit, it's important to manage debt wisely. A 22% APR on a carried balance of $2,000 wipes out nearly all that gain with $440 in interest. Cards targeting subprime users often charge over 28%, making statement credit cashback meaningless unless balances are paid off every month. Find out whether cashback is taxable in the U.S., and learn how IRS rules apply to traders earning rewards, rebates, and cash bonuses.

There’s also the psychological side to consider. A 2020 study published in the Financial Services Review found that cashback programs led to about 9% more consumer spending. For traders, that’s a red flag. Increased spending can limit liquidity and increase exposure. Using cashback wisely calls for the same mindset applied to Forex risk management, measured, strategic, and intentional.

This is where comparing cashback vs points becomes important. While points systems might offer flashy rewards like flights or merchandise, cashback is often more flexible, especially when you can use it to lower monthly expenses or reinvest in your portfolio. The real advantage lies in simplicity and liquidity.

If you run a trading-related business or expense management through a company, using cashback on business credit cards can amplify these benefits. When integrated into your business spending strategy, the returns from these cards can offer meaningful offsets to software costs, data feeds, or even business travel.

How to choose the best cashback credit card

Choosing a cashback credit card isn’t just about the headline percentage, it’s about the fine print, your habits, and how you plan to redeem your rewards with smart risk management in mind.

Key factors to compare

Cashback rates. Look beyond flat rates. Tiered or rotating categories can pay off if they align with your spending. Use a cashback calculator to forecast real returns based on what you actually spend.

Annual fees. A $95 fee (for eg.) might be worth it if the earnings exceed the cost, but only if you’ll regularly spend in the bonus categories.

Redemption flexibility. Some cards let you redeem via statement credit, direct deposit, gift cards, or travel. Make sure redemption aligns with how you actually want to use the money.

Partner merchant networks. Cards linked with grocery chains, streaming services, or travel portals can deliver extra value, not just extra cashback.

Recommended tools

Try side-by-side comparison tools from NerdWallet or PNC to quickly weigh fees, APRs, and perks.

Use a cashback calculator (like Traders Union’s) to run your spending categories and see which card gives the best net return.

| Card | Base Cashback | Bonus Categories | Annual Fee | Trader Use Case |

|---|---|---|---|---|

| Citi Double Cash | 2% total (1% when you buy + 1% as you pay) | 5% on hotels, car rentals, and attractions via Citi Travel portal | $0 | Simplicity, steady ROI on all spend |

| Chase Freedom Unlimited | 1.5% base | 5% travel via Chase Travel; 3% dining; 3% drugstores | $0 | Versatile for mixed personal expenses |

| AMEX Blue Cash Preferred | 1% base | 6% groceries, 3% gas | $0 introductory for one year, then $95 | High household spend optimization |

| SoFi Credit Card | 2% flat-rate | 3% on dining; 2% groceries; 1% on other purchases (SoFi Everyday Cash version) | $0 | Seamless integration with brokerage |

| Apple Card | 1% (physical card); 2% via Apple Pay; 3% at Apple/selected partners | 3% at Apple and Apple Pay merchants (e.g., Uber, Walgreens) | $0 | Tech-savvy traders, instant tracking |

How to maximize your cashback as a trader

Let’s explore some clever, less-talked-about ways to treat your trading expenses like mini-investments, turning fees and bills into smart earnings without complicating your strategy.

Pro strategies

Pair cashback with category‑optimized spending. Before spending on things like software subscriptions or trade platform fees, pick a card offering bonus categories for online services. Combining that with a flat-rate cashback card maximizes returns, especially when those costs are recurring.

Use business credit cards for trading‑related expenses. If you trade frequently, registering a business card under your trading entity can unlock separate spending categories, higher limits, and tax‑savvy accounting, so your cashback and APR benefits align with your strategy.

Stack rewards with cashback portals (Rakuten, TopCashback). Online portals like Rakuten or TopCashback offer an extra layer of savings. For example, if a portal gives you 5% back on trading education subscriptions, and your card gives 2%, you're stacking cash back safely. TopCashback, in particular, often beats Rakuten on rates, sometimes by a few percentage points.

Caution: Do not carry a balance, interest negates cashback. Many cards advertise 5% cashback, but with an APR of 20% or more, that gain evaporates quickly if you don't pay off your bill. Stay disciplined, always clear your balance every cycle.

| Scenario | Cashback Earned | Interest Paid | Net Result |

|---|---|---|---|

| Trader A (pays full) | $480 | $0 | + $480 |

| Trader B (small debt) | $480 | $440 | + $40 |

| Trader C (large debt) | $480 | $800 | – $320 loss |

Common cashback myths debunked

Let’s shine some light on three myths about cashback and APR, how rewarding it actually is when you know how to redeem cashback, and how to maximize credit card rewards without falling into traps.

Myth 1: “Cashback is just a gimmick.”

Reality check: nearly 70% of reward cardholders are sitting on unused rewards, with 31% holding over $100 in cashback they haven’t claimed.

Myth 2: “Only big spenders benefit.”

Even modest spenders can get value, if you spend $33K annually using a 2% cashback card, you could earn about $660 a year in rewards.

Myth 3: “Cashback affects your credit score.”

Not true. As long as you pay your balance in full, using cashback wisely doesn't hurt your score, and may even help build it.

Expert tip: Integrating cashback into your trading strategy

Traders can build a frictionless reward loop:

Spend via cashback card.

Redeem as statement credit cashback or direct deposit.

Transfer rewards automatically into brokerage.

Reinvest into ETFs, Forex, or equities monthly.

Case study: Trader Joe spends $2,500/month. A 2% flat-rate cashback yields $600/year. If reinvested monthly at 7% annual return, after 5 years it compounds to ~$ 3,500.

| Metric | Value |

|---|---|

| Monthly Spend | $2,500 |

| Annual Cashback Earned | $600 |

| Reinvested at 7% return over 5 yrs | ~$3,500 compounded |

Fintech cards like SoFi allow instant redemption into trading accounts, reducing friction even further. This proves cashback isn’t just a perk, it can become a structured capital inflow when integrated with trading discipline.

Optimizing credit card cashback with trader-specific billing cycles and wallet pairing

A smart but lesser-known trick is syncing your expenses with the billing cycle of your cashback card. Some cards increase your cashback once you cross a spending threshold in a month. So, if you bunch all those fixed costs just after your cycle starts, you hit the target faster and avoid losing out by splitting spending across two cycles.

Another great hack? Use your cashback card with digital wallets. Instead of redeeming your rewards as statement credit, send that cashback into a mutual fund or goal-based savings plan within the app. You’re not just saving, it quietly compounds. What looks like a 1.5% cashback can actually help you earn more if you park it smartly. Most traders don’t do this, and it’s such a simple way to stretch your money further.

Conclusion

Cashback converts spending into an ROI tool. For U.S. traders, it offsets fees, creates liquidity, and produces compounding micro-yields. Unlike points, it is liquid and immediately reinvestable.

Whether through flat-rate cashback, tiered rewards credit cards, or rotating category cashback, traders can make each expense productive. A cashback calculator helps identify the best card for your profile and quantify the returns.

Cashback is not free money. It is a disciplined mechanism that, when used strategically, turns everyday expenses into a steady weapon for building trading capital.

FAQs

Is cashback better than a low-interest credit card for traders?

For traders who pay balances in full, cashback delivers higher value. However, if you tend to carry debt, a low-interest card may save more in the long run.

Do business cashback cards offer better rewards than personal cards?

Yes, many business cards provide higher limits and tailored categories like office supplies or online advertising, which can benefit trading operations.

Can cashback rewards expire if not redeemed quickly?

Some issuers set redemption windows (12–24 months). Flat-rate cards typically avoid expiry, but rotating category cards may have limits or forfeiture rules.

How does cashback interact with foreign transactions?

Most cards charge 2%–3% foreign transaction fees. These fees can cancel out the benefit of cashback, so traders should choose cards with no foreign fee for global use.

Editors' Top Picks and Insights

AI without limits: How dangerous are neural networks?

Worldcoin on Wall Street: From iris scans to ETF

Mark Cuban's wealth philosophy: Why stocks matter more than salary or crypto

Dangerous but indispensable: Why the crypto market needs bridges

Markus Levin: DePIN could power the AI agent economy

Pokémon cards for $2,500: How collectibles became a new form of gambling

Related Articles

Team that worked on the article

Emilio is a futures trader and financial writer who specializes in technical analysis, market news, and trading psychology. He began his career by completing the Cornerstone Traders Qualification under the mentorship of a gold futures veteran from Bank of America on Wall Street.

One of the most widely respected and quoted currency experts, Marc Chandler has been analyzing and advising on the global capital markets for more than 30 years. Throughout his career on Wall Street, Chandler has advised private businesses, hedge funds and asset managers on navigating the foreign exchange market.

Chinmay Soni is a financial analyst with more than 5 years of experience in working with stocks, Forex, derivatives, and other assets. As a founder of a boutique research firm and an active researcher, he covers various industries and fields, providing insights backed by statistical data.

Xetra is a German Stock Exchange trading system that the Frankfurt Stock Exchange operates. Deutsche Börse is the parent company of the Frankfurt Stock Exchange.

A forex bonus is a promotional incentive offered by brokers to attract traders, typically providing additional funds or trading benefits upon fulfilling certain conditions.

Risk management is a risk management model that involves controlling potential losses while maximizing profits. The main risk management tools are stop loss, take profit, calculation of position volume taking into account leverage and pip value.

CFD is a contract between an investor/trader and seller that demonstrates that the trader will need to pay the price difference between the current value of the asset and its value at the time of contract to the seller.

Index in trading is the measure of the performance of a group of stocks, which can include the assets and securities in it.

-

Afghanistan

Afghanistan

-

Albania

Albania

-

Algeria

Algeria

-

Angola

Angola

-

Argentina

Argentina

-

Armenia

Armenia

-

Australia

Australia

-

Austria

Austria

-

Azerbaijan

Azerbaijan

-

Bahamas

Bahamas

-

Bahrain

Bahrain

-

Bangladesh

Bangladesh

-

Belarus

Belarus

-

Belgium

Belgium

-

Bolivia

Bolivia

-

Botswana

Botswana

-

Brazil

Brazil

-

Brunei

Brunei

-

Bulgaria

Bulgaria

-

Cambodia

Cambodia

-

Cameroon

Cameroon

-

Canada

Canada

-

Chile

Chile

-

China

China

-

Colombia

Colombia

-

Congo

Congo

-

Costa Rica

Costa Rica

-

Cote d'Ivoire

Cote d'Ivoire

-

Croatia

Croatia

-

Cuba

Cuba

-

Cyprus

Cyprus

-

Czechia

Czechia

-

DR Congo

DR Congo

-

Denmark

Denmark

-

Dominican Republic

Dominican Republic

-

Ecuador

Ecuador

-

Egypt

Egypt

-

El Salvador

El Salvador

-

Estonia

Estonia

-

Eswatini

Eswatini

-

Ethiopia

Ethiopia

-

Finland

Finland

-

France

France

-

Georgia

Georgia

-

Germany

Germany

-

Ghana

Ghana

-

Greece

Greece

-

Haiti

Haiti

-

Hong Kong

Hong Kong

-

Hungary

Hungary

-

India

India

-

Indonesia

Indonesia

-

Iran, Islamic republic

Iran, Islamic republic

-

Iraq

Iraq

-

Ireland

Ireland

-

Israel

Israel

-

Italy

Italy

-

Jamaica

Jamaica

-

Japan

Japan

-

Jordan

Jordan

-

Kazakhstan

Kazakhstan

-

Kenya

Kenya

-

Korea

Korea

-

Kuwait

Kuwait

-

Kyrgyzstan

Kyrgyzstan

-

Laos

Laos

-

Latvia

Latvia

-

Lebanon

Lebanon

-

Lesotho

Lesotho

-

Libya

Libya

-

Lithuania

Lithuania

-

Luxembourg

Luxembourg

-

Madagascar

Madagascar

-

Malaysia

Malaysia

-

Malta

Malta

-

Mauritius

Mauritius

-

Mexico

Mexico

-

Moldova

Moldova

-

Mongolia

Mongolia

-

Montenegro

Montenegro

-

Morocco

Morocco

-

Mozambique

Mozambique

-

Myanmar

Myanmar

-

Namibia

Namibia

-

Nepal

Nepal

-

Netherlands

Netherlands

-

New Zealand

New Zealand

-

Nigeria

Nigeria

-

North Macedonia

North Macedonia

-

Norway

Norway

-

Oman

Oman

-

Pakistan

Pakistan

-

Palestine

Palestine

-

Panama

Panama

-

Papua New Guinea

Papua New Guinea

-

Paraguay

Paraguay

-

Peru

Peru

-

Philippines

Philippines

-

Poland

Poland

-

Portugal

Portugal

-

Puerto Rico

Puerto Rico

-

Qatar

Qatar

-

Reunion

Reunion

-

Romania

Romania

-

Rwanda

Rwanda

-

Saudi Arabia

Saudi Arabia

-

Serbia

Serbia

-

Singapore

Singapore

-

Slovakia

Slovakia

-

Slovenia

Slovenia

-

Somalia

Somalia

-

South Africa

South Africa

-

Spain

Spain

-

Sri Lanka

Sri Lanka

-

Sweden

Sweden

-

Switzerland

Switzerland

-

Syria

Syria

-

Taiwan

Taiwan

-

Tajikistan

Tajikistan

-

Tanzania

Tanzania

-

Thailand

Thailand

-

Trinidad and Tobago

Trinidad and Tobago

-

Tunisia

Tunisia

-

Turkey

Turkey

-

UAE

UAE

-

Uganda

Uganda

-

Ukraine

Ukraine

-

United Kingdom

United Kingdom

-

United States

-

Uruguay

Uruguay

-

Uzbekistan

Uzbekistan

-

Venezuela

Venezuela

-

Vietnam

Vietnam

-

Yemen

Yemen

-

Zambia

Zambia

-

Zimbabwe

Zimbabwe

- Forex

- Crypto