Best Payment Tokenization Service Providers

Editorial Note: While we adhere to strict Editorial Integrity, this post may contain references to products from our partners. Here's an explanation for How We Make Money. None of the data and information on this webpage constitutes investment advice according to our Disclaimer.

Most trusted card tokenization solutions:

Visa Token Service (VTS) – global scheme tokenization with strong network trust but dependent on Visa’s infrastructure.

Mastercard MDES – offers scheme and control tokens with robust lifecycle tools but requires more complex API alignment.

Thales (Gemalto) – enterprise-grade universal tokenization with top security but higher cost and deeper integration needs.

Very Good Security (VGS) – proxy-based tokenization that removes PCI burden, but not a native network token solution.

TokenEx – flexible cloud-based tokenization service, though mainly focused on the U.S. market.

In today’s payment systems, replacing real card numbers with tokens is important for safety and stable transactions. A card tokenization service helps protect card data, lowers fraud, and makes PCI tasks easier. Many companies now use credit card tokenization solutions to keep payments simple and secure. This guide explains the basics and shows how traders and fintech users can choose the right card tokenization provider for their needs.

Best card tokenization services compared

Some issuers operate in‑house token services. Card networks offer their own schemes. Independent vault providers supplement or enable third‑party adoption. Below is a detailed comparison of the top vendors in 2026:

| Provider | Token type | Coverage | Strengths | Limitations |

|---|---|---|---|---|

| Visa Token Service (VTS) | Scheme tokens | 200+ markets, global | Network trust, scale | Scheme dependence, fee model |

| Mastercard MDES | Scheme + control tokens | Global | Integrated lifecycle tools | API alignment complexity |

| Thales (Gemalto) | Hybrid/universal tokens | Global bank clients | Security leadership, flexibility | Higher cost, deep integration |

| Very Good Security (VGS) | Proxy-based tokenization as a service | US, EU fintechs | Abstracts PCI complexity, strong APIs | Not native network tokens |

| TokenEx | Cloud vault tokens | Mostly US | Agile, modular architecture | Not fully global |

| Protegrity | Enterprise universal tokens | Global enterprises | Scalable, experience | Complex for small orgs |

| ACI Worldwide | Enterprise/scheme | Global banks | Integration with bank systems | Less startup-friendly |

| CyberSource (Visa-owned) | Integrated scheme tokens | Global (Visa ecosystem) | Visa-grade reliability | Vendor lock‑in |

| American Express | Closed-loop tokens | Amex ecosystem | Optimized for Amex cards | Limited interoperability |

| Other regional providers | Local/custom tokens | Asia, Latin America, etc. | Local compliance fit | Limited global reach |

Visa Token Service (VTS)

Visa issues scheme-based tokens that replace sensitive card numbers. Banks and merchants use VTS for secure payments in more than 200 markets. It is known for strong network trust and scale, but it depends on Visa’s scheme rules.

Mastercard MDES

MDES supports scheme tokens and extra control features for lifecycle management. It helps with digital wallets and in-app payments. It offers strong integration tools but can require complex API alignment.

Thales (Gemalto)

Thales provides universal and hybrid tokens for banks and global payment firms. It is valued for advanced security and flexible deployment. Costs can be higher and integration can be deep.

Very Good Security (VGS)

VGS uses a proxy-based model to secure card data without merchants storing it. It lowers PCI scope and offers strong API support. It does not use native scheme tokens.

TokenEx

TokenEx offers cloud vault tokenization for merchants and fintechs. It is simple, modular, and easy to integrate. Coverage is not fully global.

Protegrity

Protegrity supports enterprise-grade universal tokens for large companies. It is known for scale and long expertise. Smaller firms may find it complex.

ACI Worldwide

ACI provides enterprise and scheme tokenization for banks and processors. It fits well into large banking systems. It is less flexible for startups.

CyberSource (Visa-owned)

CyberSource offers integrated scheme tokenization in the Visa ecosystem. Users benefit from Visa-level reliability and support. It can create vendor lock-in.

American Express

Amex provides closed-loop tokens for its own card network. It offers optimized security within the Amex ecosystem. Interoperability is limited outside Amex.

Other regional providers

Regional tokenization services issue local tokens for domestic markets. They support local rules and compliance needs. Global coverage is limited.

Core principles of card tokenization

Encryption hides card numbers by turning them into coded text, but it can still be reversed with the right key. A card tokenization service works differently. It replaces the real card number with a safe token that has no link to the original data. Even if someone gets the token, they cannot use it without the vault. This is why many businesses choose card tokenization solutions and other tokenization services for payment processing to lower risk and keep customer cards safe.

Card tokenization system architecture

A strong credit card tokenization service needs simple parts that work together. It uses a vault to store real card numbers and a tool that links each token to the right card. It also manages how tokens are created, updated, or turned off. Many credit card tokenization service providers offer easy APIs so merchants can connect their systems fast. This setup is the base of most payment tokenization solutions.

Token types for card payments

Merchant tokens. Issued by PSPs, valid only within one merchant.

Network tokens. Issued by Visa, Mastercard, or Amex; usable across channels.

Hybrid tokens. Combine network security with merchant control for orchestration.

Lifecycle of сard tokens

A token goes through simple steps. It is created, used in payments, updated when the card changes, and turned off if the card is lost. If something fails, the system uses a backup path. Good card tokenization providers handle these steps automatically, which keeps payments stable and safe.

Real-world use cases for card tokenization

Many businesses use credit card tokenization service providers to store card details for subscriptions safely. Mobile wallets create tokens so the device never sees the real card number. Contactless terminals also use tokens to lower fraud in stores. Large platforms need tokens that work across regions, so they work with payment tokenization service providers that support global routing. Wearables use api tokenization solutions for secure payments to process small daily purchases without exposing card data.

Benefits and strategic considerations

Replacing real card numbers with tokens improves security and lowers fraud. A payment tokenization service protects card data and helps businesses meet PCI rules with less effort. Many companies also see better approval rates because tokenized payments are more stable.

There are risks too. Relying on one provider can limit flexibility, so some businesses use several card tokenization vendors to stay safe. Running your own vault is costly, which is why many companies choose a PCI (Payment Card Industry) tokenization service to save time, reduce work, and scale faster.

How to choose a card tokenization provider

When selecting a card tokenization provider, businesses must assess both technical and operational capabilities. The following criteria are crucial for ensuring scalability, security, and future readiness:

Latency and throughput. Evaluate how quickly the provider can issue, resolve, or refresh tokens at scale. Leading platforms support sub‑100 ms token resolution globally and handle 1,000+ token requests per second without throttling.

Global coverage and localization. A provider should support token vault distribution across key geographies to meet data residency and regulatory demands - especially in the EU, APAC, and LATAM regions.

API Maturity and documentation. Reliable credit card tokenization providers offer versioned APIs, SDKs, webhooks, and sandbox environments. Robust developer tooling is key for fast, stable integration.

Failover and redundancy. Enterprise-grade providers must support multi-zone failover with auto-switching token vaults. SLA-backed uptime (99.99 %+) is a standard expectation.

PCI DSS Level 1 Certification. The provider should be certified for token vault hosting and tokenization operations. PCI compliance is non-negotiable when handling raw PAN data.

Token format and lifecycle flexibility. Providers should support merchant, scheme, and hybrid tokens - with configurable expiration, refresh policies, and cryptographic metadata embedded in tokens.

Cost structure. Pricing varies by token volume, geographic distribution, and features. Look for clear cost tiers and bundle options for PCI tokenization vendors.

Architectures include monolithic vault usage, hybrid multi‑vault orchestration, and fallback routing to secondary providers. The orchestration layer can dynamically choose which vault to use for each transaction.

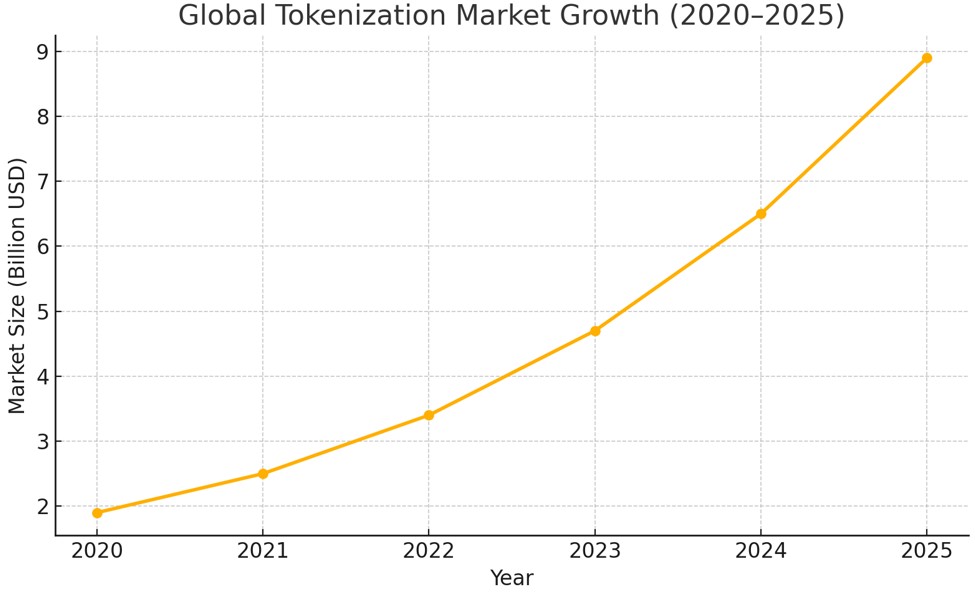

Market trends and growth forecasts

The market for payment tokenization solutions is growing fast because more payments now happen online and on mobile devices. Businesses want safer ways to handle card data, which increases demand for credit card tokenization service providers and tools that support global use.

From 2020 until now, the value of the tokenization market has risen sharply, driven by fraud risks, new security rules, and the need for simple digital payments. Much of this growth comes from companies that use a credit card tokenization service to protect transactions and meet PCI requirements.

The rise shows how important scalable and compliant payment tokenization services have become for all types of merchants, banks, and fintech businesses.

Growth drivers

Mobile wallet payments have grown quickly, and most of these transactions now use tokens instead of real card numbers. This pushes more companies to adopt payment tokenization solutions to keep up with customer habits.

Large networks have issued billions of tokens worldwide, which shows how widely Visa and Mastercard tokenization service tools are used in online shopping.

Stricter security rules also play a big role. Many businesses are moving to PCI tokenization solutions to meet new PCI standards, lower risk, and reduce audit work. These factors together drive demand for safer and more flexible credit card tokenization service options.

Regional dynamics

North America has the strongest use of tokenized payments because fintech companies adopt new tools quickly and follow strict data rules. Many firms in this region choose the best card tokenization solutions to support cloud payments and large customer volumes.

Asia-Pacific is growing even faster. Countries in this region use digital wallets and online payments at a high rate, which increases demand for card tokenization services and reliable top card tokenization providers that work across borders.

Europe is also expanding its use of tokenization. Local rules require strong privacy controls, so many businesses adopt credit card tokenization solutions that support regional compliance and safe payment flows.

Technical deep dive

Token formats and cryptographic protections. Tokens often include small encrypted parts that confirm a real transaction. These protections stop fake or repeated charges.

Token interoperability and conversion. Mapping between merchant tokens and scheme tokens, or cross‑vault conversions, is complex but essential for multi‑provider flexibility.

Token refresh and expiry. When a card changes, tokens must refresh smoothly. Good card tokenization services update tokens automatically to avoid payment issues.

Fallback flow and resilience. If a token cannot be resolved, systems switch to a backup path or use another vault for safety.

Experimentation: DLT / blockchain approaches. Some trials embed token vault logic into ledger structures, aiming for auditability and decentralization. Throughput and governance remain major limits.

Future outlook and strategic imperatives

Tokenization will expand beyond cards. Businesses will use tokens for deposits, rewards, identity, and other digital assets. This growth makes card tokenization solutions an important entry point for wider token-based systems. As open finance evolves, tokens will support lending, verification, and many cross-platform processes.

Companies should stay flexible by working with a top card tokenization provider and avoiding dependence on a single vault. They should monitor key performance metrics and explore new token uses such as loyalty and identity. Crypto-linked cards are also rising in popularity. These products still rely on trusted card tokenization services to secure each transaction and meet PCI standards while moving between crypto and traditional money.

Tokenization in crypto-backed card payments

Crypto platforms now offer debit and credit cards that let users spend digital assets in everyday payments. These cards still depend on strong card tokenization services to hide real card numbers, reduce fraud, and keep each transaction safe. A reliable setup also helps the cards meet PCI rules and handle the move between crypto and normal currency. Many exchanges use a credit card vault and tokenization provider so their card programs stay secure, stable, and easy for users to manage.

As more businesses adopt tokenization to keep payments safe, many users also look for reliable places to manage their digital activity, especially when dealing with crypto-linked cards or on chain services. If you are exploring that side of the ecosystem, the table of best crypto exchanges in your region below can help you find platforms that are easy to use and trusted by traders. It is a simple way to compare your options before you start connecting cards or making digital payments.

| Crypto | Foundation year | Min. Deposit, $ | Coins Supported | Spot Taker fee, % | Spot Maker Fee, % | Alerts | Copy trading | Tier-1 regulation | TU overall score | Open an account | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Yes | 2011 | 10 | 278 | 0.4 | 0.25 | Yes | Yes | Yes | 9.2 | Go to broker Your capital is at risk. |

|

| Yes | 2017 | 10 | 329 | 0.1 | 0.08 | Yes | Yes | No | 8.9 | Go to broker Your capital is at risk. |

|

| Yes | 2011 | 10 | 399 | 0.3 | 0.2 | No | Yes | Yes | 7.84 | Go to broker Your capital is at risk.

|

|

| Yes | 2012 | 10 | 249 | 0.5 | 0.5 | Yes | No | Yes | 7.68 | Go to broker Your capital is at risk. |

|

| Yes | 2014 | 5 | 30 | Not available | Not available | No | No | Yes | 7.6 | Go to broker Your capital is at risk.

|

Tokenization works best when simple, flexible, and easy to adapt

From my work with payment teams, I see the same pattern again and again. Tokenization helps the most when a business focuses on the basics first. It needs a provider that stays stable on busy days and gives tools the team can understand without extra training.

I usually suggest avoiding a setup that depends on only one vault, because that makes it hard to change direction later. When a company watches its token activity often and keeps simple backup steps ready, it avoids most problems before they grow. In my experience, the businesses that treat tokenization as part of their everyday workflow stay safer, meet PCI rules more easily, and grow with fewer roadblocks.

Conclusion

In summary, as payment security continues to be a top priority, selecting the right card tokenization provider is crucial for businesses aiming to protect sensitive data and prevent fraud. Leading providers like Stripe and Adyen demonstrate that robust tokenization not only instills confidence in consumers but also streamlines the checkout process for merchants. The most effective partners combine advanced technical safeguards with seamless integration, making payment experiences both safe and user-friendly. Ultimately, embracing tokenization is more than a compliance measure—it's a long-term investment in trust, efficiency, and the future of digital commerce.

FAQs

How does tokenization impact payment approval rates for online transactions?

What are the main differences between merchant, network, and hybrid token types?

Which technical features should businesses prioritize when selecting a card tokenization provider?

How is tokenization used in mobile wallets and wearable payment devices?

Editors' Top Picks and Insights

Is Bitcoin right for you? Five traits shared by many cryptocurrency holders

Chasing hits: Why investors are losing interest in Netflix

Tokenized stocks in the spotlight: How do they work and are they worth trading?

Do politicians make the best stock traders?

Crypto test drive: How automakers are exploring digital assets

Lindsey Graham death: U.S. senator’s crypto legacy

Related Articles

Team that worked on the article

Andrey Mastykin is an experienced author, editor, and content strategist who has been with Traders Union since 2020. As an editor, he is meticulous about fact-checking and ensuring the accuracy of all information published on the Traders Union platform.

Dan Blystone began his trading career in 1998 as an arbitrage clerk on the floor of the Chicago Mercantile Exchange (CME). He later traded bond and Eurex futures at proprietary firms such as Altea Trading, gaining valuable experience in high-frequency trading and risk management.

Chinmay Soni is a financial analyst with more than 5 years of experience in working with stocks, Forex, derivatives, and other assets. As a founder of a boutique research firm and an active researcher, he covers various industries and fields, providing insights backed by statistical data.

Copy trading is an investing tactic where traders replicate the trading strategies of more experienced traders, automatically mirroring their trades in their own accounts to potentially achieve similar results.

Bitcoin is a decentralized digital cryptocurrency that was created in 2009 by an anonymous individual or group using the pseudonym Satoshi Nakamoto. It operates on a technology called blockchain, which is a distributed ledger that records all transactions across a network of computers.

An investor is an individual, who invests money in an asset with the expectation that its value would appreciate in the future. The asset can be anything, including a bond, debenture, mutual fund, equity, gold, silver, exchange-traded funds (ETFs), and real-estate property.

Cryptocurrency is a type of digital or virtual currency that relies on cryptography for security. Unlike traditional currencies issued by governments (fiat currencies), cryptocurrencies operate on decentralized networks, typically based on blockchain technology.

CFD is a contract between an investor/trader and seller that demonstrates that the trader will need to pay the price difference between the current value of the asset and its value at the time of contract to the seller.

-

Afghanistan

Afghanistan

-

Albania

Albania

-

Algeria

Algeria

-

Angola

Angola

-

Argentina

Argentina

-

Armenia

Armenia

-

Australia

Australia

-

Austria

Austria

-

Azerbaijan

Azerbaijan

-

Bahamas

Bahamas

-

Bahrain

Bahrain

-

Bangladesh

Bangladesh

-

Belarus

Belarus

-

Belgium

Belgium

-

Bolivia

Bolivia

-

Botswana

Botswana

-

Brazil

Brazil

-

Brunei

Brunei

-

Bulgaria

Bulgaria

-

Cambodia

Cambodia

-

Cameroon

Cameroon

-

Canada

Canada

-

Chile

Chile

-

China

China

-

Colombia

Colombia

-

Congo

Congo

-

Costa Rica

Costa Rica

-

Cote d'Ivoire

Cote d'Ivoire

-

Croatia

Croatia

-

Cuba

Cuba

-

Cyprus

Cyprus

-

Czechia

Czechia

-

DR Congo

DR Congo

-

Denmark

Denmark

-

Dominican Republic

Dominican Republic

-

Ecuador

Ecuador

-

Egypt

Egypt

-

El Salvador

El Salvador

-

Estonia

Estonia

-

Eswatini

Eswatini

-

Ethiopia

Ethiopia

-

Finland

Finland

-

France

France

-

Georgia

Georgia

-

Germany

Germany

-

Ghana

Ghana

-

Greece

Greece

-

Haiti

Haiti

-

Hong Kong

Hong Kong

-

Hungary

Hungary

-

India

India

-

Indonesia

Indonesia

-

Iran, Islamic republic

Iran, Islamic republic

-

Iraq

Iraq

-

Ireland

Ireland

-

Israel

Israel

-

Italy

Italy

-

Jamaica

Jamaica

-

Japan

Japan

-

Jordan

Jordan

-

Kazakhstan

Kazakhstan

-

Kenya

Kenya

-

Korea

Korea

-

Kuwait

Kuwait

-

Kyrgyzstan

Kyrgyzstan

-

Laos

Laos

-

Latvia

Latvia

-

Lebanon

Lebanon

-

Lesotho

Lesotho

-

Libya

Libya

-

Lithuania

Lithuania

-

Luxembourg

Luxembourg

-

Madagascar

Madagascar

-

Malaysia

Malaysia

-

Malta

Malta

-

Mauritius

Mauritius

-

Mexico

Mexico

-

Moldova

Moldova

-

Mongolia

Mongolia

-

Montenegro

Montenegro

-

Morocco

Morocco

-

Mozambique

Mozambique

-

Myanmar

Myanmar

-

Namibia

Namibia

-

Nepal

Nepal

-

Netherlands

Netherlands

-

New Zealand

New Zealand

-

Nigeria

Nigeria

-

North Macedonia

North Macedonia

-

Norway

Norway

-

Oman

Oman

-

Pakistan

Pakistan

-

Palestine

Palestine

-

Panama

Panama

-

Papua New Guinea

Papua New Guinea

-

Paraguay

Paraguay

-

Peru

Peru

-

Philippines

Philippines

-

Poland

Poland

-

Portugal

Portugal

-

Puerto Rico

Puerto Rico

-

Qatar

Qatar

-

Reunion

Reunion

-

Romania

Romania

-

Rwanda

Rwanda

-

Saudi Arabia

Saudi Arabia

-

Serbia

Serbia

-

Singapore

Singapore

-

Slovakia

Slovakia

-

Slovenia

Slovenia

-

Somalia

Somalia

-

South Africa

South Africa

-

Spain

Spain

-

Sri Lanka

Sri Lanka

-

Sweden

Sweden

-

Switzerland

Switzerland

-

Syria

Syria

-

Taiwan

Taiwan

-

Tajikistan

Tajikistan

-

Tanzania

Tanzania

-

Thailand

Thailand

-

Trinidad and Tobago

Trinidad and Tobago

-

Tunisia

Tunisia

-

Turkey

Turkey

-

UAE

UAE

-

Uganda

Uganda

-

Ukraine

Ukraine

-

United Kingdom

United Kingdom

-

United States

-

Uruguay

Uruguay

-

Uzbekistan

Uzbekistan

-

Venezuela

Venezuela

-

Vietnam

Vietnam

-

Yemen

Yemen

-

Zambia

Zambia

-

Zimbabwe

Zimbabwe

- Forex

- Crypto

- Best card tokenization services compared

- Core principles of card tokenization

- Benefits and strategic considerations

- How to choose a card tokenization provider

- Market trends and growth forecasts

- Future outlook and strategic imperatives

- Tokenization in crypto-backed card payments

- Expert opinion

- Conclusion

- FAQs