Top Sukuk Bonds In Bangladesh (2026)

Editorial Note: While we adhere to strict Editorial Integrity, this post may contain references to products from our partners. Here's an explanation for How We Make Money. None of the data and information on this webpage constitutes investment advice according to our Disclaimer.

Popular sukuk bonds in Bangladesh:

Safe Water Sukuk (ISIN: BDS092501059) — 5Y, Ijarah, 4.69% profit, funds national water supply, BDT 8,000 Cr.

Primary Schools Sukuk (BDS092601050) — 5Y, Ijarah, 4.65%, supports school infrastructure, BDT 5,000 Cr.

IRIDP-3 green-sukuk (BDS092701051) — 5Y, Istisna’a + Ijarah, 4.75%, targets rural development, BDT 5,000 Cr.

CDWSP Sukuk (BDS092901051) — 5Y, Istisna’a + Ijarah, 10.40%, for clean water/sanitation, BDT 1,000 Cr.

CIBRR-2 Sukuk (BDS093201071) — 7Y, Istisna’a + Ijarah, 9.25%, socio-economic boost, BDT 3,000 Cr.

RDIRWSP Sukuk (BDS093202072) — 7Y, Ijarah, 10.50%, rural infrastructure focus, BDT 2,000 Cr.

In recent years, sukuk in Bangladesh has gained significant traction as a viable and trusted alternative to traditional bonds. Structured to eliminate riba, sukuk offers profit through real asset ownership and leasing arrangements. Since Bangladesh launched its inaugural sovereign issuance in 2020, the sukuk bond in the Bangladesh market has helped fund key national infrastructure projects while catering to the growing demand from both institutional and individual Islamic investors. Today, sukuk plays a central role in the country’s Shariah-compliant investing landscape. This article outlines what sukuk bonds are, how investors can access them in Bangladesh, and why they represent a stable, faith-compliant investment solution.

Risk warning: All investments carry risk, including potential capital loss. Economic fluctuations and market changes affect returns, and 40-50% of investors underperform benchmarks. Diversification helps but does not eliminate risks. Invest wisely and consult professional financial advisors.

What is a sukuk bond in Bangladesh?

A sukuk bond is an Islamic investment tool designed to give profits without breaking Islamic rules about interest. In Bangladesh, sukuk works through profit-sharing or leasing models, where investors get returns from real projects or assets instead of fixed interest payments.

The first sukuk bond in Bangladesh launched by Bangladesh Bank to fund things like roads, energy, and water systems. What sets it apart is that investors are not just lenders, they become part-owners in the project. They share profits and risks, and everything from how the money is raised, used, and paid out has to be approved by religious finance experts.

By 2026, the government of Bangladesh has successfully raised BDT 19,000 crore through four separate government bond offerings structured as sovereign sukuk. Investors can purchase sukuk through Islamic banks, and the average annual return currently stands at around 10.4%. These investments are ideal for individuals seeking ethical, low-risk opportunities that align with Islamic financial principles.

Some well-known examples include the Tk 8,000 crore Government Investment Sukuk, used for clean water projects. Banks like Islami Bank Bangladesh and Standard Chartered Saadiq are also exploring sukuk for the private sector. What makes this exciting is the possibility of working with countries like Malaysia and the UAE, showing that sukuk could soon be a key part of faith-based funding for big national projects in Bangladesh.

Here are some popular sukuk bonds in Bangladesh:

| ISIN | Project name | Tenor | Sukuk type | Issue date | Maturity date | Profit/Rental rate | Outstanding (BDT Cr.) |

|---|---|---|---|---|---|---|---|

| BDS092501059 | Safe Water Supply to the Whole Country | 5 yr | Ijarah | 29‑Dec‑2020 | 29‑Dec‑2025 | 4.69% | 8,000 |

| BDS092601050 | Infrastructure Dev. of Govt Primary Schools (1st Phase) | 5 yr | Ijarah | 30‑Dec‑2021 | 30‑Dec‑2026 | 4.65% | 5,000 |

| BDS092701051 | IRIDP‑3 Social Impact Sukuk | 5 yr | Istisna’a & Ijarah | 20‑Apr‑2022 | 20‑Apr‑2027 | 4.75% | 5,000 |

| BDS092901051 | CDWSP Social Impact Sukuk | 5 yr | Istisna’a & Ijarah | 06‑Jun‑2024 | 06‑Jun‑2029 | 10.40% | 1,000 |

| BDS093201071 | CIBRR‑2 Socio‑Economic Sukuk | 7 yr | Istisna’a & Ijarah | 13‑Mar‑2025 | 13‑Mar‑2032 | 9.25% | 3,000 |

| BDS093202072 | RDIRWSP Socio‑Economic Development Sukuk | 7 yr | Ijarah | 20‑May‑2025 | 20‑May‑2032 | 10.50% | 2,000 |

You can invest in the above sukuk with a minimum of BDT 10,000 (about $100), as a resident or non-resident. Residents can invest through any scheduled bank or primary dealer during public auctions or on the secondary market. Non-residents must open a Non-Resident Investor’s Taka Account (NITA) or a foreign currency deposit account with a Bangladeshi bank to participate. These sukuk are tradable, offer semi-annual profit payouts, and profits can be freely repatriated for foreign investors.

Growth of sukuk in Bangladesh

Since the launch of the first sukuk, the Bangladesh government has held several rounds of issuance. By early 2025, the fifth series successfully secured BDT 3,000 crore to fund rural bridge construction across 58 upazilas. The total value raised through sukuk in Bangladesh reached BDT 22,000 crore by mid-2025, underscoring growing investor interest and confidence in these Islamic financial instruments.

Among the most recent issues is the 5-year CDWSP Social Impact Sukuk, launched in June 2024, which offers a 10.40% annual rental return, paid every six months. This particular offering saw 85% allocated to Shariah-based banks and financial institutions, 10% to Islamic banking windows within conventional banks, and 5% to individual investors and provident funds.

Sukuk bond investment in Bangladesh has gained traction among both retail and institutional investors, thanks to its ethical structure and predictable returns. The market’s appeal lies in its Shariah-compliant foundation, offering an attractive alternative to conventional debt instruments.

Since its inception:

Total sukuk raised (as of Q2 2025). BDT 22,000 crore

Number of sukuk series. 5

Yield on the 2024 issue. 10.40% annually

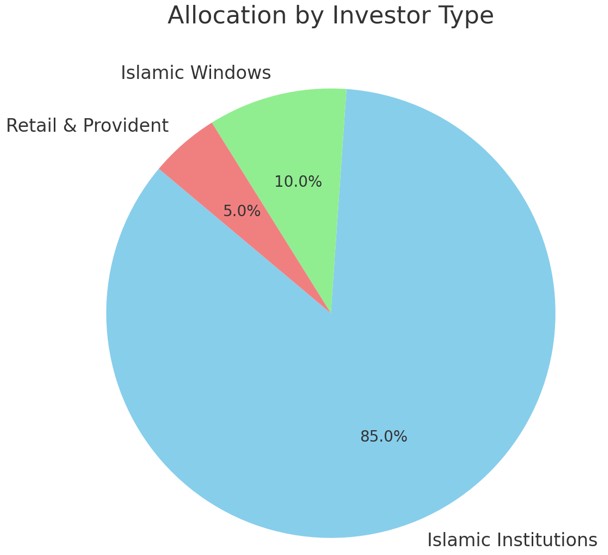

Breakdown by investor category:

85% – Islamic banks and financial institutions.

10% – Islamic windows of conventional banks.

5% – Retail investors and provident funds.

The investor allocation pie chart illustrates that Islamic banks dominate the market with an 85% share, followed by Islamic windows at 10%, and the remaining 5% going to individual investors and provident funds.

Why invest in sukuk?

Unlike conventional bonds, sukuk represent partial ownership in a tangible asset, a service, or a project, not just debt. This asset-backed nature means returns come from real economic activity, not interest payments. For investors, that translates to a more ethical and transparent link between capital and productivity. Some sukuk structures even tie payouts to project performance, adding built-in risk-sharing mechanisms that align better with Islamic finance principles.

One underreported angle is how sukuk offer stability in frontier markets. Take the sukuk bond in Bangladesh as an example. Launched to fund infrastructure, it was backed by real state assets, offering investors security while also meeting Shariah guidelines. The government’s use of Ijara (leasing) structures meant returns came from actual rental flows, not speculation. These instruments are gaining traction not just among devout investors, but also ESG-focused institutions that value ethical and asset-linked financing over synthetic derivatives.

| Benefit | Explanation |

|---|---|

| Shariah-compliant | Avoids riba (interest); backed by real assets |

| Stable returns | Typically pegged to rental income from infrastructure projects |

| Government-backed security | Issued by the Ministry of Finance; low default risk |

| Tradeable on secondary market | After 1/3rd asset delivery, sukuk can be sold at negotiated prices |

| Portfolio diversification | Non-correlated to stocks or conventional fixed-income instruments |

How to buy sukuk bonds in Bangladesh

Investing in sukuk bonds in Bangladesh is a viable option for both institutional investors and eligible individuals. The entire process is regulated by the Bangladesh Bank and carried out in coordination with Shariah-compliant banks and the Central Depository Bangladesh Ltd. (CDBL), making it secure and transparent for participants.

Open an investment account

The first step is to open an Islamic investment account or a Mudarabah savings account with a certified Shariah-compliant bank. Some of the prominent institutions offering this facility include:

Islami Bank Bangladesh Ltd.

Al-Arafah Islami Bank

First Security Islami Bank

Exim Bank

These banks often act as Primary Dealers (PDs), helping investors complete the required documentation and place bids during sukuk auctions.

Monitor Bangladesh bank sukuk announcements

All upcoming sukuk issuances are officially announced by the Bangladesh Bank on its Sukuk portal. These announcements are also communicated through PD banks. Subscription periods usually span three to five working days and include information such as maturity terms, rental yield, and the underlying asset structure.

Submit your bid or subscription request

Once the sukuk is announced, you can place your bid either by visiting your bank’s Islamic investment desk or through their online application form.

The minimum bid is typically BDT 10,000, with additional amounts in multiples of BDT 5,000. Institutional investors generally submit bids starting from BDT 1 crore (10 million) or higher.

It’s important to submit your bid before the deadline, as late entries are not accepted. For issues with high demand, such as the June 2024 sukuk which was oversubscribed by 2.5 times, early submission is strongly advised.

If you’re willing to explore other halal investment options in Bangladesh, you may refer to any of the following guides:

Halal Mutual Funds in Bangladesh.

Further, to invest in any of the halal investment options, you will need an Islamic trading account offered by a few of the top global brokers. We have listed them in the table below for your reference:

| Swap Free | ETFs | Stocks | Indices | Min. deposit, $ | Regulation | TU overall score | Open an account | |

|---|---|---|---|---|---|---|---|---|

| Yes | No | Yes | No | 10 | No | 7.89 | Go to broker Your capital is at risk.

|

|

| Yes | Yes | Yes | Yes | 100 | CIMA, FCA, FSA (Japan), NFA, IIROC, ASIC, CFTC | 6.74 | Study review | |

| Yes | No | Yes | Yes | 5 | CySEC, FSC (Belize), DFSA, FSCA, FSA (Seychelles), FSC (Mauritius), SCA (United Arab Emirates), CMA (Kenya) | 9.3 | Go to broker Your capital is at risk. |

|

| Yes | No | Yes | Yes | No | FSC (BVI), ASIC, IIROC, FCA, CFTC, NFA | 6.8 | Go to broker Your capital is at risk. |

|

| Yes | Yes | Yes | Yes | 100 | CySEC, FCA, ASIC, FMA, FSCA, FSA Seychelles, EFSA, MAS, DFSA, SCB | 7.52 | Go to broker 80% of retail CFD accounts lose money. |

Payment and allotment

If your bid is successful, payment will be made from your investment account. The sukuk units you’re allotted will be credited directly to your CDBL BO (Beneficiary Owner) account, enabling secure ownership and tracking.

Hold or trade your sukuk

You can choose to hold the sukuk until maturity to receive your full principal back. However, once one-third of the underlying asset has been delivered, the sukuk becomes eligible for trading in the secondary market under Islamic finance principles.

Banks generally charge a processing or bid handling fee between 0.10% and 0.25%, so it’s wise to confirm the exact fee beforehand.

Future outlook

Bangladesh’s sukuk market is entering a new phase of growth, driven by policy reform, a broader investor base, and alignment with national infrastructure goals. With several key initiatives underway, the country is positioning itself as a rising hub for Islamic finance in South Asia.

Policy-driven expansion

The Ministry of Finance has revealed plans to introduce a National Sukuk Policy Framework by the last quarter of 2025. Once implemented, this reform is expected to streamline the issuance process, reducing the average turnaround time from 45 days to under 21. This would make asset transfers and auction procedures more efficient and predictable.

In addition, amendments proposed to the Public Debt Act of 1944 are set to officially recognize digital sukuk formats, paving the way for deeper fintech integration into the Islamic finance space. A digital sukuk is a technology-enabled version of this financial instrument. It uses digital platforms, often blockchain or fintech-backed solutions, to issue, manage, and trade sukuk more efficiently and transparently. It lowers administrative burdens and brings Islamic finance closer to modern digital infrastructures.

Financial inclusion targets

The Bangladesh Bank has outlined its goal to bring 1 million new retail investors into the sukuk space by 2027. To support this ambition, the Central Shariah Board for Islamic Banks has launched a pilot program offering sukuk units starting at just BDT 5,000 (approximately USD 45). These will be made available through agent banking services and Islamic microfinance outlets in 40 rural districts, expanding access beyond urban centers. The initiative reflects a major step in growing sukuk investment in Bangladesh by focusing on grassroots-level financial inclusion.

Infrastructure-linked sukuk

In 2026, over BDT 6,000 crore (roughly USD 550 million) in new sukuk issuances are planned, with funds linked to specific infrastructure projects. These include the reconstruction of 62 Upazila bridges, a solar hybrid power plant between Dhaka and Mymensingh expected to generate 150 MW, and the development of water purification systems across six major municipalities. These projects will follow a ringfenced model, where lease or rent payments are generated from the operational income of the underlying infrastructure. This kind of targeted issuance model has become central to the success of sukuk bonds in Bangladesh initiatives.

Regional sukuk listings

Dual-listed sukuk refers to Islamic financial certificates that are simultaneously listed on two different stock exchanges, often in separate countries. This allows issuers to reach a wider pool of global investors while ensuring better liquidity and visibility. In this context, Bangladesh is working toward issuing sukuk that would be listed both locally and in international markets like Nasdaq Dubai.

Sukuk, often likened to Islamic bonds, are investment instruments compliant with Shariah principles, meaning they avoid interest-based earnings and are often backed by tangible assets. When paired with ESG (Environmental, Social, Governance) goals, e.g. green sukuk, these instruments attract socially conscious investors, particularly from the Islamic finance world.

Boost sukuk returns in Bangladesh by timing government issuances and targeting project-linked tranches

A lot of people think sukuk works just like any other bond, but in Bangladesh, there’s a sharper edge to it. Since many sukuk are tied directly to specific government projects, you can get ahead by tracking when those projects are about to kick off. Public development plans usually hint at when new sukuk will be issued. If you invest during the early funding phase, you're often rewarded with better returns, because you’re taking on slightly more risk upfront, and that gets factored into the payout.

Another angle most folks miss is choosing sukuk tied to specific sectors like transport or energy. These aren’t just backed by the government, they also come with clear project milestones. If you follow how the actual project is doing, you can often guess when bonuses or increased payouts might hit. It's less about waiting and more about reading the fine print and keeping an eye on real progress. That’s how you turn sukuk into a smarter game.

Conclusion

Sukuk bonds in Bangladesh represent a strategic bridge between ethical investing and infrastructure development. With over BDT 22,000 crore raised and yields reaching 10.4%, sukuk has become a vital tool for faith-based and risk-conscious investors. Accessible via Islamic banks and backed by real assets, sukuk combines compliance, stability, and purpose. As Bangladesh expands its sukuk market, this Shariah-compliant instrument is increasingly seen as a core portfolio component.

FAQs

Can non-Muslims invest in sukuk bonds in Bangladesh?

Yes, sukuk bonds are open to all investors. Non-Muslims can invest as long as they meet eligibility requirements from banks or issuers.

Are sukuk bonds taxed in Bangladesh?

Sukuk earnings are subject to applicable income tax laws. Tax exemptions may apply for certain institutions or under specific schemes.

Can I trade sukuk bonds before maturity?

Yes, after one-third of the asset is delivered, sukuk bonds can be traded on the secondary market at negotiated prices.

What risks are associated with sukuk bonds?

While sukuk is low-risk due to asset backing and government support, risks include early redemption, liquidity limits, and project delays.

Editors' Top Picks and Insights

Bitcoin mining is getting greener, but the debate isn't over

Asia's largest IPO: How CXMT became China's most valuable company

Global fintech in 2026: Three trends that matter

From Jesus Christ to aliens: Polymarket's most absurd prediction markets

Hunting crypto owners: Why criminals have gone offline

BitMEX is shutting down: Why Trump could not save the exchange

Related Articles

Team that worked on the article

Alamin Morshed is a contributor at Traders Union. He specializes in writing articles for businesses that want to improve their Google search rankings to compete with their competition.

Chinmay Soni is a financial analyst with more than 5 years of experience in working with stocks, Forex, derivatives, and other assets. As a founder of a boutique research firm and an active researcher, he covers various industries and fields, providing insights backed by statistical data.

Mirjan Hipolito is a journalist and news editor at Traders Union. She is an expert crypto writer with five years of experience in the financial markets.

-

Afghanistan

Afghanistan

-

Albania

Albania

-

Algeria

Algeria

-

Angola

Angola

-

Argentina

Argentina

-

Armenia

Armenia

-

Australia

Australia

-

Austria

Austria

-

Azerbaijan

Azerbaijan

-

Bahamas

Bahamas

-

Bahrain

Bahrain

-

Bangladesh

Bangladesh

-

Belarus

Belarus

-

Belgium

Belgium

-

Bolivia

Bolivia

-

Botswana

Botswana

-

Brazil

Brazil

-

Brunei

Brunei

-

Bulgaria

Bulgaria

-

Cambodia

Cambodia

-

Cameroon

Cameroon

-

Canada

Canada

-

Chile

Chile

-

China

China

-

Colombia

Colombia

-

Congo

Congo

-

Costa Rica

Costa Rica

-

Cote d'Ivoire

Cote d'Ivoire

-

Croatia

Croatia

-

Cuba

Cuba

-

Cyprus

Cyprus

-

Czechia

Czechia

-

DR Congo

DR Congo

-

Denmark

Denmark

-

Dominican Republic

Dominican Republic

-

Ecuador

Ecuador

-

Egypt

Egypt

-

El Salvador

El Salvador

-

Estonia

Estonia

-

Eswatini

Eswatini

-

Ethiopia

Ethiopia

-

Finland

Finland

-

France

France

-

Georgia

Georgia

-

Germany

Germany

-

Ghana

Ghana

-

Greece

Greece

-

Haiti

Haiti

-

Hong Kong

Hong Kong

-

Hungary

Hungary

-

India

India

-

Indonesia

Indonesia

-

Iran, Islamic republic

Iran, Islamic republic

-

Iraq

Iraq

-

Ireland

Ireland

-

Israel

Israel

-

Italy

Italy

-

Jamaica

Jamaica

-

Japan

Japan

-

Jordan

Jordan

-

Kazakhstan

Kazakhstan

-

Kenya

Kenya

-

Korea

Korea

-

Kuwait

Kuwait

-

Kyrgyzstan

Kyrgyzstan

-

Laos

Laos

-

Latvia

Latvia

-

Lebanon

Lebanon

-

Lesotho

Lesotho

-

Libya

Libya

-

Lithuania

Lithuania

-

Luxembourg

Luxembourg

-

Madagascar

Madagascar

-

Malaysia

Malaysia

-

Malta

Malta

-

Mauritius

Mauritius

-

Mexico

Mexico

-

Moldova

Moldova

-

Mongolia

Mongolia

-

Montenegro

Montenegro

-

Morocco

Morocco

-

Mozambique

Mozambique

-

Myanmar

Myanmar

-

Namibia

Namibia

-

Nepal

Nepal

-

Netherlands

Netherlands

-

New Zealand

New Zealand

-

Nigeria

Nigeria

-

North Macedonia

North Macedonia

-

Norway

Norway

-

Oman

Oman

-

Pakistan

Pakistan

-

Palestine

Palestine

-

Panama

Panama

-

Papua New Guinea

Papua New Guinea

-

Paraguay

Paraguay

-

Peru

Peru

-

Philippines

Philippines

-

Poland

Poland

-

Portugal

Portugal

-

Puerto Rico

Puerto Rico

-

Qatar

Qatar

-

Reunion

Reunion

-

Romania

Romania

-

Rwanda

Rwanda

-

Saudi Arabia

Saudi Arabia

-

Serbia

Serbia

-

Singapore

Singapore

-

Slovakia

Slovakia

-

Slovenia

Slovenia

-

Somalia

Somalia

-

South Africa

South Africa

-

Spain

Spain

-

Sri Lanka

Sri Lanka

-

Sweden

Sweden

-

Switzerland

Switzerland

-

Syria

Syria

-

Taiwan

Taiwan

-

Tajikistan

Tajikistan

-

Tanzania

Tanzania

-

Thailand

Thailand

-

Trinidad and Tobago

Trinidad and Tobago

-

Tunisia

Tunisia

-

Turkey

Turkey

-

UAE

UAE

-

Uganda

Uganda

-

Ukraine

Ukraine

-

United Kingdom

United Kingdom

-

United States

-

Uruguay

Uruguay

-

Uzbekistan

Uzbekistan

-

Venezuela

Venezuela

-

Vietnam

Vietnam

-

Yemen

Yemen

-

Zambia

Zambia

-

Zimbabwe

Zimbabwe

- Forex

- Crypto