How Finfluencers Shape Retail Investment Decisions: TU Research

Editorial Note: While we adhere to strict Editorial Integrity, this post may contain references to products from our partners. Here's an explanation for How We Make Money. None of the data and information on this webpage constitutes investment advice according to our Disclaimer.

TU research shows that finfluencers have become the leading source of investment ideas for retail investors and the strongest trigger of real trades. In a CAWI survey of 1,200 investors, 41% named social media as their main idea source, 34% said finfluencers most often triggered actual trades, and 49% reported buying an asset after influencer content. The effect is strongest among younger and less experienced investors, while short-form video content drives the most impulsive decisions.

The rise of finfluencers has changed how retail investors discover ideas, evaluate risk, and act on market narratives. Social platforms no longer serve only as information channels; for many investors, they now function as a frontline decision environment where investment content competes directly with broker research, financial media, advisers, and issuer communications. CFA Institute, IOSCO, FINRA Foundation, and the SEC have all highlighted this shift from a different angle: influence, disclosure, fraud risk, and investor protection.

This TU research concept is built around one practical question: Do finfluencers affect real retail investment decisions more strongly than traditional sources? The study is designed to test not only reach, but behavioral impact: who actually moves investors from watching content to opening positions, changing allocations, or taking risks they otherwise would not take.

The study focuses on five key questions:

Findings

Based on TU proprietary research, several key patterns emerge:

- Finfluencers lead idea generation but don’t fully replace traditional sources. Social media dominates (41%), ahead of broker research (26%) and financial media (18%), though investors still use multiple channels.

- Behavioral impact outweighs trust. Finfluencers are the top trigger of real trades (34%), slightly ahead of broker platforms (29%), showing that speed and accessibility matter more than credibility.

- Decisions are fast and reactive. Nearly half of investors (49%) buy after influencer content, and 37% act within 24 hours, confirming strong short-term behavioral influence.

- Risk is higher for socially driven investors. About 28% report losses after influencer-driven trades, aligning with evidence of increased error and fraud exposure.

- Younger investors are most affected. Influence drops from 62% (ages 18–24) to 21% (45+), highlighting a strong generational gap.

- Experience reduces reliance. Trust in finfluencers falls from 44% (<1 year experience) to 18% (3+ years), indicating higher vulnerability among beginners.

- Short-form content drives action. Short videos lead (46%), far ahead of long-form (28%), articles (16%), and broker reports (10%), reinforcing the role of format in impulsive decisions.

Risk warning: Forex trading carries high risks, with potential losses including your entire deposit. Market fluctuations, economic instability, and geopolitical factors impact outcomes. Studies show that 70-80% of traders lose money. Consult a financial advisor before trading.

Institutional validation

Institutional evidence strongly supports the relevance of this topic. The FINRA Foundation’s 2026 brief on social-media-informed retail investors shows that social media is already embedded in investment decision-making behavior, especially among younger investors. It also identifies a mix of overconfidence, broader information-seeking, and significantly higher fraud vulnerability among users and finfluencer followers.

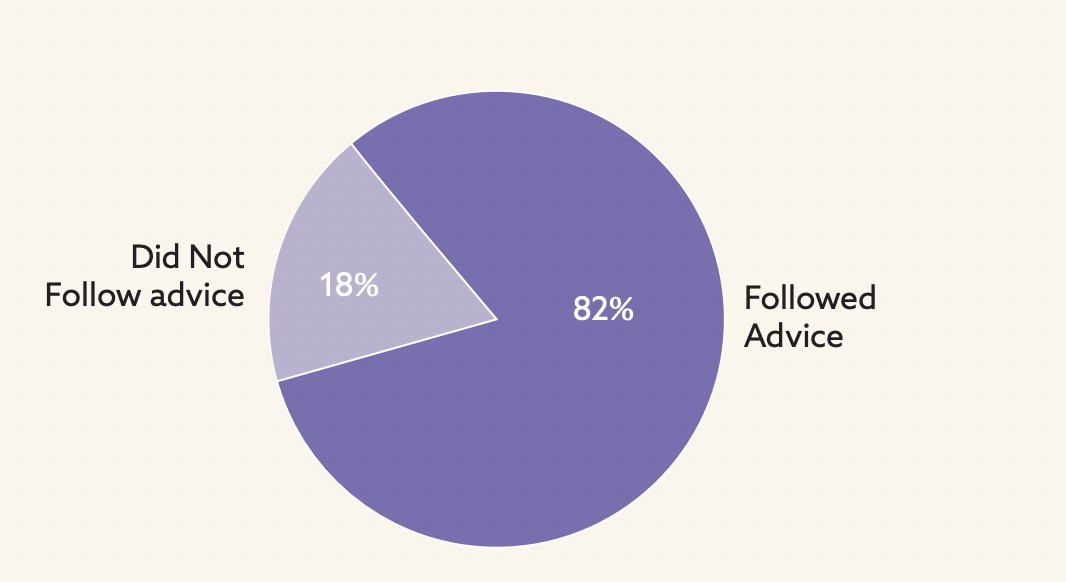

CFA Institute adds an important behavioral layer. In its 2025 survey report Clicks and Credibility, based on 1,615 investors and content analysis of 51 finfluencers, the Institute found that 82% of investors influenced by social media acted on that advice. The same report also showed weak disclosure standards and frequent explicit recommendations from largely unregistered creators.

IOSCO’s 2025 final report treats finfluencers as a formal retail-investor-protection issue. Its assessment highlights regulatory gaps, unregistered individuals influencing retail investors without professional oversight, and the need for clearer disclosures, conflict management, and investor education. That places finfluencer influence firmly inside the mainstream regulatory agenda rather than at the margins of online finance culture.

The SEC’s Investor Advisory Committee reached a similar conclusion in late 2024: social media has helped attract new, especially younger, investors into markets, but it also creates a channel for fraudulent or poor-quality investment advice. The Committee explicitly noted that some finfluencers can provide investment recommendations to large audiences without appropriate qualifications or disclosures.

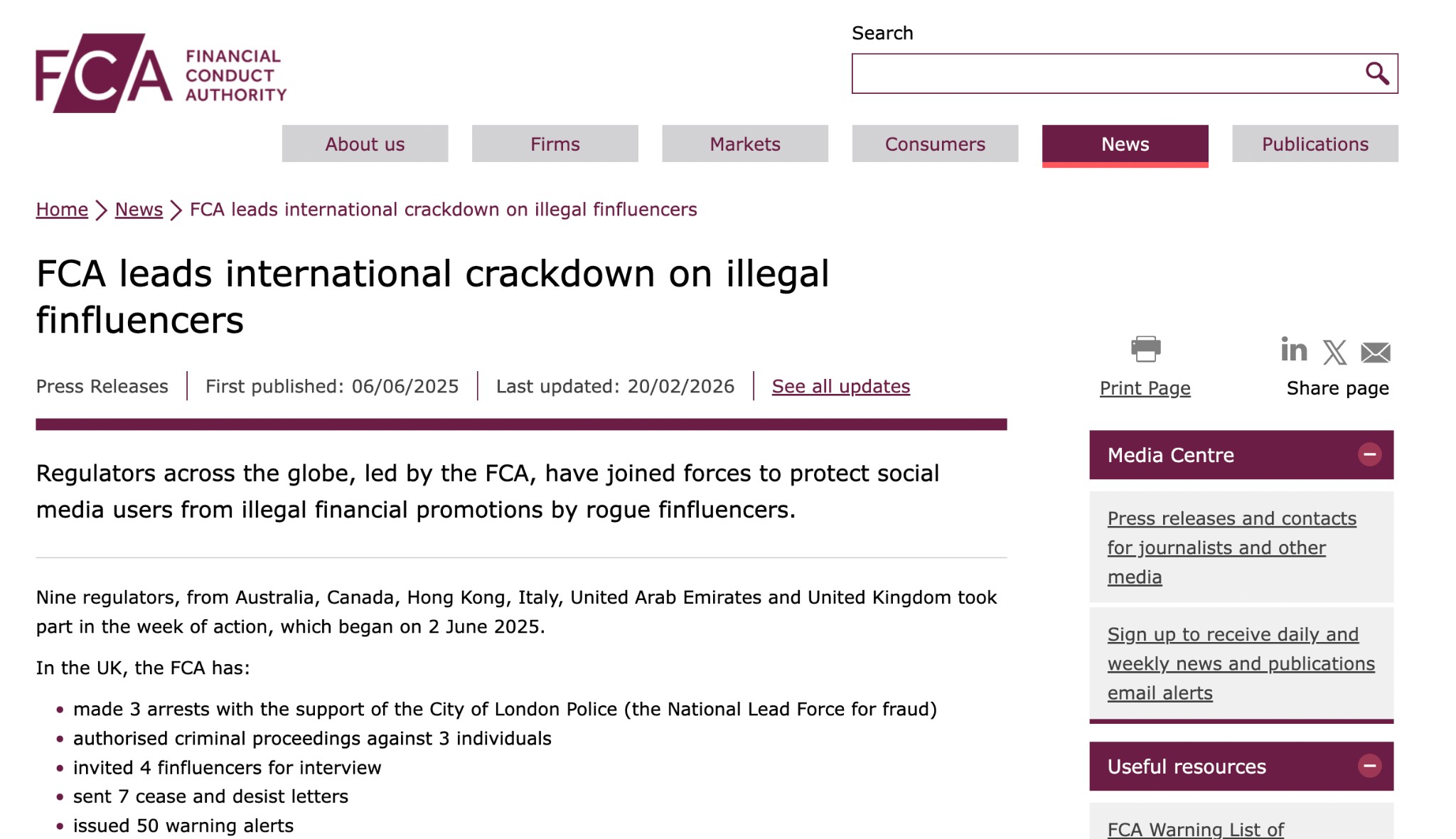

Regulators are also moving from analysis to enforcement. The UK FCA stated that in June 2025 it led an international crackdown on illegal finfluencers that resulted in arrests, cease-and-desist letters, and warning alerts. This confirms that the issue is no longer theoretical; it is already producing supervisory and legal action.

Theoretical research

From a behavioral standpoint, finfluencer influence is likely strongest when three conditions are present: low friction to content consumption, high emotional relatability, and weak source verification. CFA Institute’s 2024 report on young investors shows that finfluencer content often works because it is engaging, relatable, and native to the platforms where younger investors already spend time. That creates an asymmetry: traditional research may be more rigorous, but social content may be more persuasive.

This also suggests a key CAWI hypothesis: short-form, personality-driven content may trigger more impulsive investment behavior than longer-form or institutional content. FINRA Foundation’s findings support that concern indirectly through the combination of overconfidence, entertainment motives, and social activity motives among social-media-informed investors. In other words, for some users, investing content is not processed only as analysis; it is also consumed as identity, excitement, and participation.

A second theoretical hypothesis concerns experience. Newer investors may not simply “trust social media more”; they may rely on it differently because it is easier to understand, easier to access, and more emotionally legible than broker notes or issuer materials. That aligns with IOSCO’s concern that retail investors may struggle to interpret risks, disclaimers, or the true nature of recommendations made by influencers.

A third hypothesis concerns substitution versus complementarity. FINRA Foundation found that social-media-informed investors actually use more information sources on average than non-users. That means social media may not always replace traditional sources; in many cases, it may become the trigger that sends investors toward a broker app, a chart, a message board, or a trade ticket. The real CAWI challenge is therefore to isolate which source causes action rather than mere exposure.

Survey data

To evaluate whether finfluencers influence retail investment decisions more strongly than traditional sources, we conducted a proprietary quantitative study focused on information sources, behavioral impact, and decision-making patterns.

Unlike existing institutional research, TU provides a behavioral-level comparison between information sources, distinguishing not only where investors get ideas, but which sources actually trigger real trades. The study also introduces new dimensions, including reaction speed, content format impact, and differences between declared trust and actual decision-making.

Methodology

The research was based on a structured online survey conducted among retail investors, using the CAWI (Computer-Assisted Web Interviewing) methodology. This approach ensured standardized data collection and consistency across different regions and respondent groups.

Sample size: 1,200 retail investors.

Geography: global (multi-market sample).

Age: 18+.

Eligibility: respondents who have made at least one self-directed investment decision in the last 12 months.

Confidence level: 95%.

Margin of error: ±3.0%.

Participants were selected based on active investment behavior, with a focus on how they discover investment ideas, which sources influence their decisions, and how content consumption affects trading outcomes. The survey examined the relationship between information sources, trust levels, and real investment actions.

Research team

The study was conducted by the analytical team at Traders Union:

Anastasiia Chabaniuk (Author, TU Research) – research design and interpretation.

Chinmay Soni (Fact-checker) – data validation and statistical verification.

Dan Blystone (Editor-in-Chief) – editorial and methodological supervision.

TU Research Team (Andrey Mastykin, Oleg Tkachenko) – data collection and analysis.

Note! This research design is based on validated institutional findings, but the proprietary CAWI module should be used to confirm, nuance, or challenge those patterns in TU’s target audience rather than assume they apply universally.

Source of actions

To identify which sources actually lead to trades, we analyzed behavioral triggers.

Sources that trigger real investment actions:

Social media / finfluencers – 34%.

Broker platforms / analytics – 29%.

Financial media – 16%.

Personal network – 11%.

Advisers – 10%.

Insight: While the gap narrows, finfluencers still rank as the #1 trigger of actual trades, confirming that their influence is not just informational but behavioral.

Behavioral impact

To measure direct influence, we analyzed how often investors act on social content.

| Action | Share |

|---|---|

| Bought an asset after influencer content | 49% |

| Lost money on such trades | 28% |

| Acted within 24 hours after exposure | 37% |

Insight: The data partially confirms CFA Institute findings:

Nearly half of investors act on finfluencer content.

A significant share reports negative outcomes, supporting FINRA fraud-risk concerns.

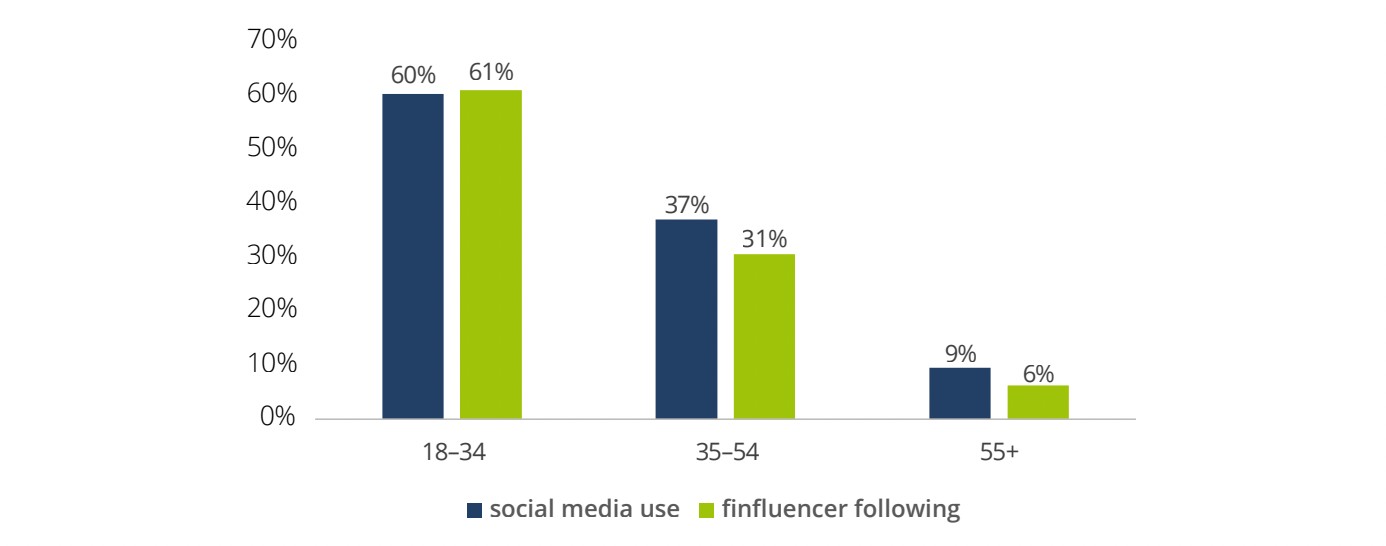

Age factor

To test generational differences, we segmented results by age.

Finfluencer impact by age segment:

18–24 – 62%.

25–34 – 57%.

35–44 – 38%.

45+ – 21%.

Insight: The hypothesis is strongly confirmed: younger investors are significantly more influenced by finfluencers.

Loss exposure factor

To assess whether social-media-driven investors face higher risks, we analyzed loss patterns and risk behavior.

| Metric | Share |

|---|---|

| Lost money on trades influenced by social content | 28% |

| Higher fraud/loss risk (social users vs non-users) | 68% vs 26% |

| Do not use stop-loss consistently | 63% |

Insight: Social-media-driven investors show higher exposure to losses and weaker risk management practices, supporting concerns about increased vulnerability to low-quality advice and impulsive trading.

Content format impact

To measure the role of content format, we analyzed behavioral responses.

Influence of content formats:

Short-form video – 46%.

Long-form video – 28%.

Articles – 16%.

Broker reports – 10%.

Insight: Short-form content (TikTok, Reels) is the strongest behavioral driver, confirming the hypothesis about impulsive decision-making.

PDF version of the TU research

Download the full PDF version of the TU research to access additional analysis, detailed survey data, and extended findings from our analytical team. The report includes complete methodology, charts, and behavioral insights referenced throughout the study.

Practical implications for retail traders

To navigate investment decisions in an environment increasingly shaped by finfluencers, retail investors need to shift from passive content consumption to structured decision-making. The following principles can help improve outcomes:

Treat content as a trigger, not a decision. Social media often acts as the starting point for an idea, not its validation. Before acting on any recommendation, investors should cross-check it with broker analytics, financial data, or independent sources. The key question is not who said it, but what data supports it.

Verify the source, not the presentation. Engaging delivery does not equal credibility. Even well-explained content may lack regulatory oversight, disclosures, or accountability. Always assess whether the source provides transparency on risks, conflicts of interest, and track record.

Separate education, opinion, and promotion. One of the most critical skills is distinguishing between informative content and marketing. Sponsored posts, affiliate-driven recommendations, and undisclosed promotions can significantly bias decision-making. Investors should develop a habit of identifying intent behind the content.

Use high-quality analysis alongside social signals. Not all Telegram or social channels are equal. For example, channels like Viktoras Karapetjanc and Anton Kharitonov provide structured analytics, trading signals, and market forecasts, combining accessibility with a more disciplined analytical approach. Using such sources as part of a broader information mix can reduce reliance on purely entertainment-driven content.

Avoid impulsive decisions driven by short-form content. Research shows that short videos and rapid content formats increase the likelihood of immediate action. Introducing a delay between idea and execution – even a few hours – can significantly improve decision quality.

Focus on the execution environment, not just ideas. Even strong trading ideas depend on execution quality. Factors such as spreads, slippage, order speed, and platform stability directly affect outcomes. This makes the choice of broker or exchange a critical component of overall performance.

From a practical standpoint, this means that successful investing is not determined by access to ideas, but by how those ideas are filtered, validated, and executed.

Below is a comparison of the best Forex brokers that provide reliable execution environments for traders acting on both analytical and signal-based strategies:

| Trading.com USA | Plus500 | OANDA | FOREX.com | Venom by Cobra Trading | |

|---|---|---|---|---|---|

|

Min. deposit, $ |

50 | 100 | No | 100 | 5000 |

|

Tradable assets |

69 | 2800 | 129 | 5500 | No |

|

Standard EUR/USD spread |

1.1 | 0.7 | 0.3 | 1.0 | 0.4 |

|

Max. leverage |

1:50 | 1:300 | 1:200 | 1:50 | 1:4 |

|

Max. Regulation Level |

Tier-1 | Tier-1 | Tier-1 | Tier-1 | Tier-1 |

|

TU overall score |

8.75 | 7.54 | 6.86 | 6.83 | 6.8 |

|

Open an account |

Go to broker Your capital is at risk. |

Go to broker 80% of retail CFD accounts lose money. |

Go to broker Your capital is at risk. |

Study review | Study review |

Data sources and methodology references

CFA Institute (2025). Clicks and Credibility: Understanding Finfluencers’ Role in Investment Decisions.

FINRA Foundation (2025). Finfluencer Followers and Social Media Scrollers.

IOSCO (2025). Finfluencers Final Report.

SEC Investor Advisory Committee (2024). Recommendation on Finfluencers and Investor Protection.

UK FCA (2025). Crackdown on illegal finfluencers.

OECD (2024). Financial Literacy and Digitalisation

European Securities and Markets Authority (ESMA, 2024). Social media sentiment: Influence on EU equity prices.

Bank for International Settlements (BIS, 2024). Retail investors and digital finance behavior.

National Bureau of Economic Research (NBER, 2024). Retail investor behavior and information sources.

IdSurvey. CAWI Methodology Overview

Previous volumes in this series

How Retail Traders Use AI in Practice

Best Time to Trade Gold: What TU Research Shows

How Retail Investors Actually Trade Crypto

Conclusion

Finfluencers have become the dominant force shaping retail investment behavior, especially among younger and less experienced investors. TU’s research confirms that social media influencers are not just a source of ideas—they actively trigger real trades, with nearly half of surveyed investors reporting they bought assets based on influencer content. This trend is further amplified by short-form videos, which drive more impulsive decisions and heighten risk exposure, as seen in the 28% loss rate after such trades. The data underscores a critical truth: in today’s digital markets, the power to move capital no longer lies solely with formal institutions, but with relatable, rapid-fire creators whose influence rivals or even surpasses traditional financial media. For retail investors, success now depends not just on what content they consume, but on how critically they filter, validate, and act on it.

FAQs

How do finfluencers influence the speed at which retail investors act on investment ideas?

What behavioral differences exist between social-media-driven investors and those who rely primarily on traditional research?

What role does trust play in the influence of finfluencers versus traditional sources on investor behavior?

How does investment experience shape the way investors interact with finfluencer content?

Editors' Top Picks and Insights

From “Holy Trinity” to WLD crash: How Arthur Hayes became a market-moving seller

The world's first trillionaire: How Musk built his fortune on electric cars, space and AI

How precious-metals mining revival is reshaping portfolios in 2026

Bitcoin price prediction after CPI rise: Is BTC headed for deeper losses?

Five years with Bitcoin: How El Salvador changed after legalizing BTC

Crypto on the court: How NBA Finals became a showcase for Ledger

Related Articles

Team that worked on the article

Anastasiia has 17 years of experience in finance and content marketing. She believes that the support of information and expert opinion is very important for the success of investors and new traders.

Dan Blystone began his trading career in 1998 as an arbitrage clerk on the floor of the Chicago Mercantile Exchange (CME). He later traded bond and Eurex futures at proprietary firms such as Altea Trading, gaining valuable experience in high-frequency trading and risk management.

Chinmay Soni is a financial analyst with more than 5 years of experience in working with stocks, Forex, derivatives, and other assets. As a founder of a boutique research firm and an active researcher, he covers various industries and fields, providing insights backed by statistical data.

-

Afghanistan

Afghanistan

-

Albania

Albania

-

Algeria

Algeria

-

Angola

Angola

-

Argentina

Argentina

-

Armenia

Armenia

-

Australia

Australia

-

Austria

Austria

-

Azerbaijan

Azerbaijan

-

Bahamas

Bahamas

-

Bahrain

Bahrain

-

Bangladesh

Bangladesh

-

Belarus

Belarus

-

Belgium

Belgium

-

Bolivia

Bolivia

-

Botswana

Botswana

-

Brazil

Brazil

-

Brunei

Brunei

-

Bulgaria

Bulgaria

-

Cambodia

Cambodia

-

Cameroon

Cameroon

-

Canada

Canada

-

Chile

Chile

-

China

China

-

Colombia

Colombia

-

Congo

Congo

-

Costa Rica

Costa Rica

-

Cote d'Ivoire

Cote d'Ivoire

-

Croatia

Croatia

-

Cuba

Cuba

-

Cyprus

Cyprus

-

Czechia

Czechia

-

DR Congo

DR Congo

-

Denmark

Denmark

-

Dominican Republic

Dominican Republic

-

Ecuador

Ecuador

-

Egypt

Egypt

-

El Salvador

El Salvador

-

Estonia

Estonia

-

Eswatini

Eswatini

-

Ethiopia

Ethiopia

-

Finland

Finland

-

France

France

-

Georgia

Georgia

-

Germany

Germany

-

Ghana

Ghana

-

Greece

Greece

-

Haiti

Haiti

-

Hong Kong

Hong Kong

-

Hungary

Hungary

-

India

India

-

Indonesia

Indonesia

-

Iran, Islamic republic

Iran, Islamic republic

-

Iraq

Iraq

-

Ireland

Ireland

-

Israel

Israel

-

Italy

Italy

-

Jamaica

Jamaica

-

Japan

Japan

-

Jordan

Jordan

-

Kazakhstan

Kazakhstan

-

Kenya

Kenya

-

Korea

Korea

-

Kuwait

Kuwait

-

Kyrgyzstan

Kyrgyzstan

-

Laos

Laos

-

Latvia

Latvia

-

Lebanon

Lebanon

-

Lesotho

Lesotho

-

Libya

Libya

-

Lithuania

Lithuania

-

Luxembourg

Luxembourg

-

Madagascar

Madagascar

-

Malaysia

Malaysia

-

Malta

Malta

-

Mauritius

Mauritius

-

Mexico

Mexico

-

Moldova

Moldova

-

Mongolia

Mongolia

-

Montenegro

Montenegro

-

Morocco

Morocco

-

Mozambique

Mozambique

-

Myanmar

Myanmar

-

Namibia

Namibia

-

Nepal

Nepal

-

Netherlands

Netherlands

-

New Zealand

New Zealand

-

Nigeria

Nigeria

-

North Macedonia

North Macedonia

-

Norway

Norway

-

Oman

Oman

-

Pakistan

Pakistan

-

Palestine

Palestine

-

Panama

Panama

-

Papua New Guinea

Papua New Guinea

-

Paraguay

Paraguay

-

Peru

Peru

-

Philippines

Philippines

-

Poland

Poland

-

Portugal

Portugal

-

Puerto Rico

Puerto Rico

-

Qatar

Qatar

-

Reunion

Reunion

-

Romania

Romania

-

Rwanda

Rwanda

-

Saudi Arabia

Saudi Arabia

-

Serbia

Serbia

-

Singapore

Singapore

-

Slovakia

Slovakia

-

Slovenia

Slovenia

-

Somalia

Somalia

-

South Africa

South Africa

-

Spain

Spain

-

Sri Lanka

Sri Lanka

-

Sweden

Sweden

-

Switzerland

Switzerland

-

Syria

Syria

-

Taiwan

Taiwan

-

Tajikistan

Tajikistan

-

Tanzania

Tanzania

-

Thailand

Thailand

-

Trinidad and Tobago

Trinidad and Tobago

-

Tunisia

Tunisia

-

Turkey

Turkey

-

UAE

UAE

-

Uganda

Uganda

-

Ukraine

Ukraine

-

United Kingdom

United Kingdom

-

United States

-

Uruguay

Uruguay

-

Uzbekistan

Uzbekistan

-

Venezuela

Venezuela

-

Vietnam

Vietnam

-

Yemen

Yemen

-

Zambia

Zambia

-

Zimbabwe

Zimbabwe

- Forex

- Crypto