How precious-metals mining revival is reshaping portfolios in 2026

One of the biggest market stories of 2026 outside the technology sector has been the strong performance of gold and silver. Silver is up 80% over the last 12 months. Gold is up about 30% over the past year, trading near $4,200 per ounce, and has gained more than 125% over the last five years. The rally in precious metals has been impressive, but many mining stocks have delivered even stronger returns thanks to their operational leverage to rising commodity prices.

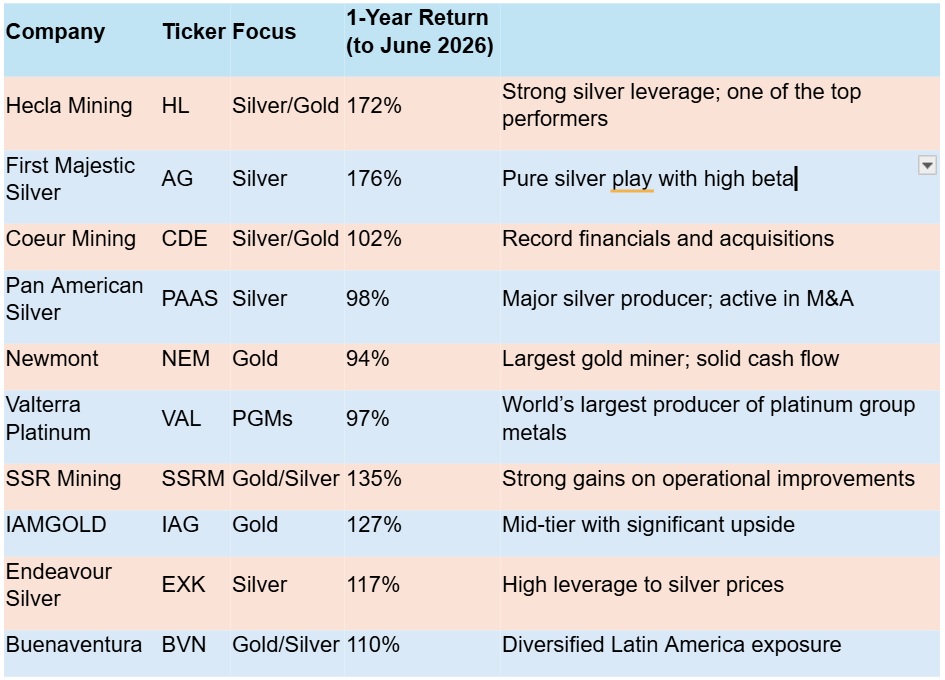

Precious metals stocks returns over 1 year

Two of the best performing stocks are heavily skewed towards silver, with both Hecla Mining and First Majestic Silver growing more than 170% over the last 12 months. Though silver exploded through $100/oz in early 2026 before settling back into the $70-$80/oz range, this generated massive margin expansion for both companies, with Hecla nearly doubling its earnings, while First Majestic hit a record 15.4 million ounces of production in 2025. This, coupled with the acquisition of Gatos Silver in Mexico and blow-out growth in revenues over the last three quarters, explain the surge in its stock price.

There’s been some retreat from the record prices of silver and gold – which broke $5,000/oz earlier this year – but many analysts remain convinced the best is yet to come.

Why banks are bullish on gold

JP Morgan remains bullish on gold, with a price target of $6,300/oz by the end of 2026, with a return to $5,000/oz by Q4, citing continued central bank purchases and asset diversification as the key drivers of price. Wells Fargo, UBS and Bank of American also see gold above $6,000/oz by the end of the year.

Goldman Sachs is more conservative, pitching gold at $5,400/oz by end-2026.

The World Gold Council and China Gold Market Update both point to a seemingly irreversible trend – the de-dollarisation of major world economies, a process that has accelerated since the 2022 freezing of Russian USD assets. This ignited panic among U.S. rival economies that their assets held offshore might be at risk. The message is clear – you cannot trust the US with your wealth. Countries have taken that on board and started buying gold.

Another factor driving money into gold is rising concerns over out-of-control sovereign debt in the US and elsewhere in the West, which ultimately debases the USD and has launched an unprecedented wave of gold call option buying from institutions.

One of the easiest ways for institutions and individuals to gain exposure to gold is through ETFs. Figures from the World Gold Council show ETFs held a staggering 4,025 tonnes of gold at the end of 2025.

“Demand for gold remains broad-based, spanning individuals, family offices, institutional investors, and central banks, with ongoing central bank accumulation providing a particularly strong underpinning to the market,” says investment firm Baker Steel. “These buyers appear set to continue accumulating gold into 2026 and beyond.”

If the outlook is bright, it’s also worth bearing in mind that precious metals are not for the weak of heart. They are prone to extreme volatility – one reason why many fund managers love them – with bull markets being followed by extended bear markets. The companies that actually mine these metals have different levels of leverage to the underlying commodities – the thinner the profit margin in bear markets, the more the stock price accelerates when precious metal prices take off.

Contrast the current market with the 2011–2020 bear market when precious metals prices were depressed, miners scrambled to pay down debt and projects were cancelled. It was a bleak time for the mining sector.

The hunt for acquisitions

Much has changed since then. Now Tier 1 miners are on the acquisition trail to replace depleting reserves and scale for growth. Even mid-sized miners are seized by the urgency of acquisition and consolidation. In 2025, Pan American Silver made a $2.1 billion bid for MAG Silver, the prize here being the Juanicipio Mine in Zacatecas, Mexico.

Coeur Mining has been on a quest to expand and diversify its asset base with two major deals in the last two years:

- the acquisition of New Gold Inc. which balances its silver-heavy portfolio with up to 815,000 ounces of gold and a further 19-22 million ounces of silver, as well as 50 million pounds of copper annually.

- In 2025 it concluded the acquisition of SilverCrest Metals, an all-stock transaction valued at $1.7 billion, transforming Coeur into a leading global silver company.

While these transactions contributed to a near doubling of revenue in 2025, the surging silver price translated into a 10X explosion in net income, allowing it to pay its first ever dividend and commence a share repurchase programme.

Another company finding new lease of life under higher precious metals prices is Pan American Silver, which concluded the acquisition of MAG Silver and accelerated its organic growth. This gave it the scale and cash to position itself for the next phase of its growth.

Another company on the acquisition trail is Gold Fields, which wrapped up the $2.4 billion cash purchase of Australia’s Gold Road Resources, coming hot on the heels of the $1.4 billion buyout of Osisko Mining in Canada. Gold Fields previously acquired Barrick Gold’s Granny Smith, Lawlers, and Darlot mines in Western Australia, giving it a more diversified exposure to Tier 1 assets (large, high quality, low cost and long-life mines).

The investment case

The chart below shows how many ounces of gold it would take to buy the S&P 500 on any given month. Taking a long-term view, gold is still cheap relative to stocks – though not as cheap as it was in 2010.

S&P 500 to gold ratio. Source: MacroTrends

The table below shows how gold and silver have performed relative to the stock market over 10 years. Surprisingly, silver emerges as the champion investment over the decade, followed by the stock market (total returns, including dividends), and then gold. The stock market performance has been heavily skewed by the outperformance of tech stocks such as Amazon and Nvidia.

Total return stock index (including dividends) v gold and silver

Gold and silver miners have learned through brutal experience to take a cautious approach to debt. They emerged from several lean years with some crucial financial and operational disciplines embedded into their management styles – pay down debt, keep operating costs as low as possible, and plan for the future as if the boom times are about to crash.

It isn’t always acquisitions the miners are seeking: the world’s largest gold miner Newmont completed eight divestitures worth $3.4 billion in recent years to optimise its portfolio. Barrick Mining earned $2.4 billion by offloading its Donlin Gold project in Alaska as well as the Hemlo gold mine in Canada, and various African assets, and various African assets. Similarly, Equinox Gold Corp. sold its Brazilian operations for $1 billion to focus on North America.

Expert comment

We may indeed be at the start of a multi-year upcycle for precious metals and commodities more generally. De-dollarisation is real, and accelerating. Countries are starting to move away from the U.S. dollar and gold is the obvious candidate as a replacement. BRICS countries are underweight gold, and their central banks have started stepping up gold acquisitions to hedge against currency debasement. We see demand for gold and silver remaining firm in the teeth of supply constraints, and that will continue to underpin prices. What is encouraging is the mining sector, having learned discipline in the lean years, is carrying those lessons forward now that operating conditions are easier.Conclusion

The precious metals mining revival of 2026 has transformed the sector from a forgotten corner of the market into one of its strongest performers. With record prices, robust margins, and accelerating M&A, well-positioned miners are delivering outsized returns. For discerning investors, this cycle still offers significant upside — provided they navigate volatility with discipline.

Latest Silver News

-

Afghanistan

Afghanistan

-

Albania

Albania

-

Algeria

Algeria

-

Angola

Angola

-

Argentina

Argentina

-

Armenia

Armenia

-

Australia

Australia

-

Austria

Austria

-

Azerbaijan

Azerbaijan

-

Bahamas

Bahamas

-

Bahrain

Bahrain

-

Bangladesh

Bangladesh

-

Belarus

Belarus

-

Belgium

Belgium

-

Bolivia

Bolivia

-

Botswana

Botswana

-

Brazil

Brazil

-

Brunei

Brunei

-

Bulgaria

Bulgaria

-

Cambodia

Cambodia

-

Cameroon

Cameroon

-

Canada

Canada

-

Chile

Chile

-

China

China

-

Colombia

Colombia

-

Congo

Congo

-

Costa Rica

Costa Rica

-

Cote d'Ivoire

Cote d'Ivoire

-

Croatia

Croatia

-

Cuba

Cuba

-

Cyprus

Cyprus

-

Czechia

Czechia

-

DR Congo

DR Congo

-

Denmark

Denmark

-

Dominican Republic

Dominican Republic

-

Ecuador

Ecuador

-

Egypt

Egypt

-

El Salvador

El Salvador

-

Estonia

Estonia

-

Eswatini

Eswatini

-

Ethiopia

Ethiopia

-

Finland

Finland

-

France

France

-

Georgia

Georgia

-

Germany

Germany

-

Ghana

Ghana

-

Greece

Greece

-

Haiti

Haiti

-

Hong Kong

Hong Kong

-

Hungary

Hungary

-

India

India

-

Indonesia

Indonesia

-

Iran, Islamic republic

Iran, Islamic republic

-

Iraq

Iraq

-

Ireland

Ireland

-

Israel

Israel

-

Italy

Italy

-

Jamaica

Jamaica

-

Japan

Japan

-

Jordan

Jordan

-

Kazakhstan

Kazakhstan

-

Kenya

Kenya

-

Korea

Korea

-

Kuwait

Kuwait

-

Kyrgyzstan

Kyrgyzstan

-

Laos

Laos

-

Latvia

Latvia

-

Lebanon

Lebanon

-

Lesotho

Lesotho

-

Libya

Libya

-

Lithuania

Lithuania

-

Luxembourg

Luxembourg

-

Madagascar

Madagascar

-

Malaysia

Malaysia

-

Malta

Malta

-

Mauritius

Mauritius

-

Mexico

Mexico

-

Moldova

Moldova

-

Mongolia

Mongolia

-

Montenegro

Montenegro

-

Morocco

Morocco

-

Mozambique

Mozambique

-

Myanmar

Myanmar

-

Namibia

Namibia

-

Nepal

Nepal

-

Netherlands

Netherlands

-

New Zealand

New Zealand

-

Nigeria

Nigeria

-

North Macedonia

North Macedonia

-

Norway

Norway

-

Oman

Oman

-

Pakistan

Pakistan

-

Palestine

Palestine

-

Panama

Panama

-

Papua New Guinea

Papua New Guinea

-

Paraguay

Paraguay

-

Peru

Peru

-

Philippines

Philippines

-

Poland

Poland

-

Portugal

Portugal

-

Puerto Rico

Puerto Rico

-

Qatar

Qatar

-

Reunion

Reunion

-

Romania

Romania

-

Rwanda

Rwanda

-

Saudi Arabia

Saudi Arabia

-

Serbia

Serbia

-

Singapore

Singapore

-

Slovakia

Slovakia

-

Slovenia

Slovenia

-

Somalia

Somalia

-

South Africa

South Africa

-

Spain

Spain

-

Sri Lanka

Sri Lanka

-

Sweden

Sweden

-

Switzerland

Switzerland

-

Syria

Syria

-

Taiwan

Taiwan

-

Tajikistan

Tajikistan

-

Tanzania

Tanzania

-

Thailand

Thailand

-

Trinidad and Tobago

Trinidad and Tobago

-

Tunisia

Tunisia

-

Turkey

Turkey

-

UAE

UAE

-

Uganda

Uganda

-

Ukraine

Ukraine

-

United Kingdom

United Kingdom

-

United States

-

Uruguay

Uruguay

-

Uzbekistan

Uzbekistan

-

Venezuela

Venezuela

-

Vietnam

Vietnam

-

Yemen

Yemen

-

Zambia

Zambia

-

Zimbabwe

Zimbabwe

- Forex

- Crypto