Why This Is The Time To Accumulate Indonesian Bank Stocks

Editorial Note: While we adhere to strict Editorial Integrity, this post may contain references to products from our partners. Here's an explanation for How We Make Money. None of the data and information on this webpage constitutes investment advice according to our Disclaimer.

Foreign investors have yanked USD3.75bn out of Indonesian equities so far in 1H25, the largest net-sell in the region, knocking the Jakarta Composite Index 2% lower in USD terms and dragging bank valuations back to multi-year lows.

For global traders hunting durable yield and EM rebound plays, that capitulation is creating a rare entry point. Indonesia’s leading lenders now combine dividend yields that reach 8%, surpassing the 10-year Indonesian Government bond yield of 6.5%, with system-wide NPLs below 2%, and they just received an additional tail-wind from Bank Indonesia’s fresh 25bp rate cut to 5.25%. Past easing cycles in 2016-17, 2019 and 2020 preceded double-digit rallies in bank shares – trends this article will revisit in detail. We’ll show why beaten-down valuations, policy support and improving trade sentiment make it time to buy Indonesian bank stocks and how you can position for the next leg higher.

Risk warning: All investments carry risk, including potential capital loss. Economic fluctuations and market changes affect returns, and 40-50% of investors underperform benchmarks. Diversification helps but does not eliminate risks. Invest wisely and consult professional financial advisors.

Foreign investors flee, creating value gaps

International investors have been pulling money out of Indonesian equities, which drove down prices of bank stocks to compelling levels. In late 2024 and early 2025, foreigners were net sellers for six consecutive months – an unusually prolonged exodus not seen since 2017. They offloaded approximately USD3.85bn worth of Indonesian stocks from October 2024 through March 2025. Such massive outflows were driven by global risk aversion – concerns about Indonesia’s fiscal policy shifts, prolonged high interest rates, and political uncertainty.

Sentiment swung to an extreme of pessimism, but this wave of selling appears overdone relative to fundamentals. Once the panic subsided, foreign inflows returned: during the five weeks from mid‑April to the end of May 2025, foreign investors posted a net buy of USD320mn, and the JCI rallied from its trough of roughly 6,400 to a peak of around 7,200. The rebound highlights how quickly flows can reverse when valuations and macro conditions turn more attractive. Meanwhile, foreigners reported net sales of USD950mn and USD3.75bn in June-mid July 2025, and YTD, reflecting a huge impact when the trend will reverse. Learn how Indonesia’s Nutritious Free Meal program helps eliminate poultry oversupply, drives stronger demand for feed and chicken products, and improves profit margins for CPIN, JPFA, and MAIN.

Valuations at multi-year lows for major and mid-tier banks

Thanks to the sell-off, valuations of Indonesian banks are now cheap relative to their own history. Price-to-book ratios (P/B) and price-to-earnings ratios (P/E) have compressed to levels not seen in years. For instance, Bank Negara Indonesia (BBNI) – one of the big-four state-owned lenders – trades around 0.9× P/B, which is 1.5 standard deviation (S.D.) below its 10-year mean. This comes even as BBNI’s profitability is improving (return on equity is consistently higher than the pre-pandemic’s level), suggesting a disconnect where price has fallen more than fundamentals.

Even market leader Bank Central Asia (BBCA), long esteemed for its premium valuation, has seen its P/E multiple compress. BBCA’s stock underperformed peers over 2021–2023, and now trades at 4.27× P/B, slightly below its 10-year mean of 4.4×, with its trailing twelve months (TTM) P/E around 18.7× which is about 1.5 S.D. below its 10-year historical mean. In other words, BBCA is no longer priced at an excessive premium; after the pullback it “is no longer fully valued” and offers upside despite short-term rate headwinds.

Crucially, mid-tier and specialized lenders are even more deeply discounted. For example, Bank Tabungan Negara (BBTN) – a mid-sized bank focusing on mortgages – currently trades at only 0.5× P/B. Such a P/B well below 1 indicates investors are pricing in substantial pessimism about future growth or asset quality, yet BBTN’s niche (government-backed housing loans) and potential benefit from lower rates suggest the pessimism may be overdone.

Industry-wide ROEs are trending upward post-pandemic, yet many bank stocks are priced for very low growth. The valuation case is clear: prices have fallen while earnings have remained solid, leaving many bank stocks at undemanding multiples. This offers a significant upside if sentiment and liquidity normalize.

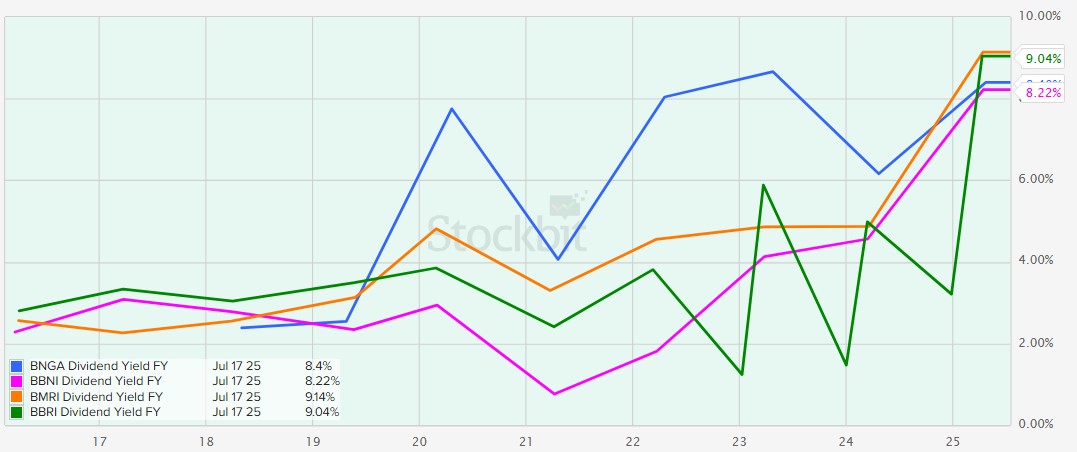

Attractive dividend yields vs history and government bonds

One immediate benefit of lower prices is higher dividend yields. Indonesian banks have a long track record of robust payouts, and with share prices depressed, those yields have climbed to attractive levels – in some cases now exceeding government bond yields or historical norms. For example, Bank CIMB Niaga (BNGA), noted above, has maintained a dividend payout over 50%, resulting in a high single-digit dividend yield for investors at the current stock price. A yield in the ~7–9% range (IDR terms) is extremely enticing, effectively rivaling the Indonesian 10-year government bond yield, which is currently at around 6.5%, while still offering equity upside. Indeed, BNGA’s generous payout and strong earnings have led analysts to call its dividend “highly attractive”, expecting this to help catalyze a re-rating of the stock.

Large banks are also boosting returns to shareholders. BBNI, for instance, is increasing its dividend payout ratio to 50% (up from a historical 20–30%). With capital levels strong (CAR ~19%), BBNI has room to nearly double its payout, which will significantly raise its yield going forward. Even Bank Rakyat Indonesia (BBRI) – the country’s biggest microfinance lender – has been paying out higher dividends; in 2023 it distributed 85% of earnings as dividends, an unusually high payout that pushed its yield into the mid-single digits. For context, BBRI’s yield had historically been in the 2–3% range, but after the recent price drop and payout boost, investors can get around 5% or more yield from BBRI stock.

Likewise, Bank Mandiri (BMRI) often yields ~6% at recent prices due to a combination of price weakness and a ~60% payout ratio. These yields are high relative to the past – just a few years ago, most Indonesian banks yielded only low-single-digit percentages because valuations were richer.

Several bank stocks that can match or beat the Indonesia 10-year government yield are BNGA and BBNI (~8%), BMRI and BBRI (~9%). This makes bank equities attractive not just to equity investors but also to income-focused investors who might see them as bond proxies with growth potential. As a result, once confidence returns, yield-hungry funds could rotate into these stocks, supporting their prices.

In short, Indonesian banks offer a rare combination of high dividend income and low valuations. The dividend yields are at multi-year highs, providing a cushion and incentive for investors to hold the stocks while waiting for price recovery. This yield support limits downside and is a strong catalyst for renewed interest – especially as local rates fall (driving bond yields down and making equity yields even more attractive by comparison).

Rate cuts: Easing cycle bodes well for bank stocks

After a period of monetary tightening, Bank Indonesia (BI) has begun cutting interest rates – a trend that historically boosts banking sector performance. The central bank hiked its benchmark rate aggressively in 2022–2023 (from a pandemic low of 3.5% up to 6.25% by Aug 2024) to combat inflation. But by late 2024, inflation was subdued and the tide turned: BI kicked off a new easing cycle in September 2024 with a surprise 25 bps rate cut to 6.00%, its first cut in over three years. This marked a policy shift from a “pro-stability” stance to a more growth-supportive stance.

Further cuts followed – BI has since trimmed the benchmark rate four times (as of July 2025) down to 5.25%. The central bank signaled room for more easing, citing low inflation and a stable IDR outlook. Lower interest rates are generally positive for banks and the broader market. They reduce funding costs, stimulate loan demand, and improve borrowers’ ability to repay loans (lower credit costs).

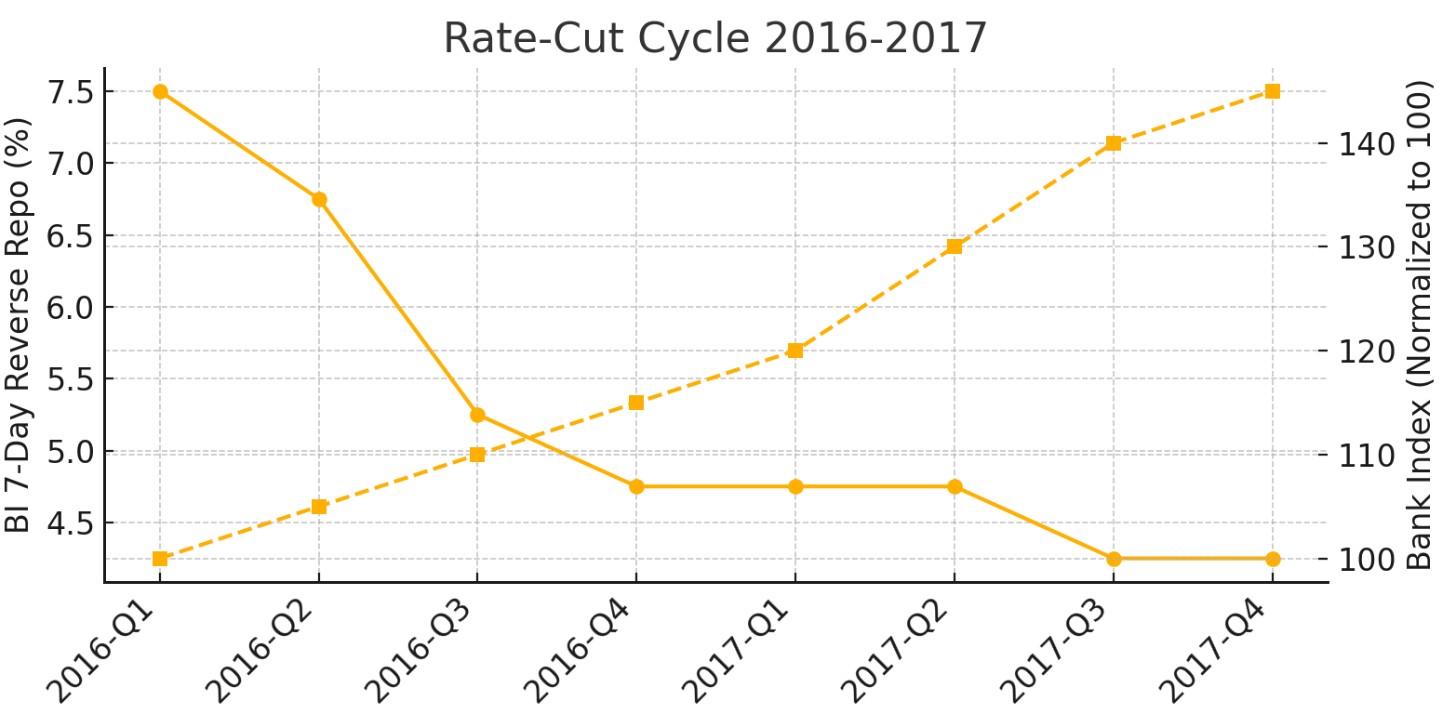

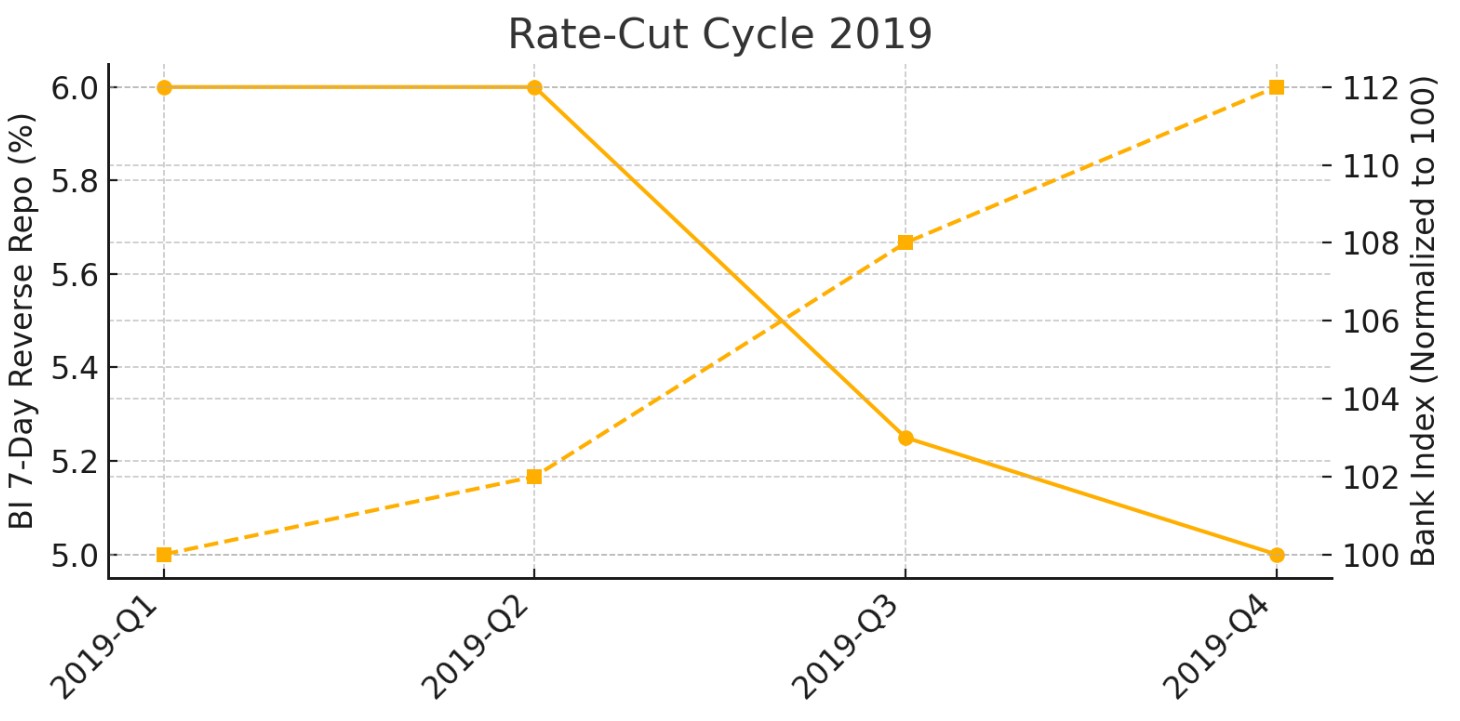

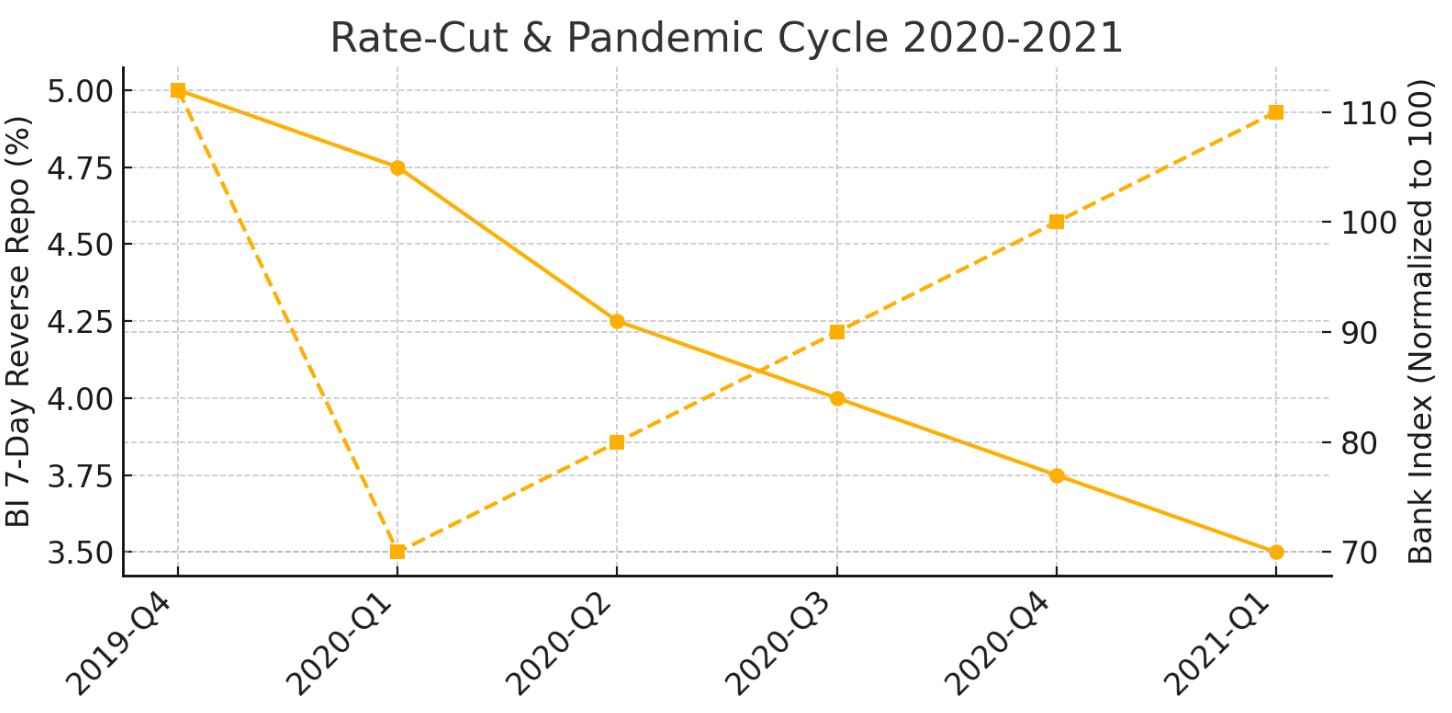

Historically, rate-cut cycles have aligned with strong bank stock performance (barring external shocks). For example, in the last major easing phase (2016–2017), BI slashed rates by 200+ bps and banks enjoyed a robust rally as economic growth picked up. Again in 2019, BI cuts helped lift bank shares (until the unforeseen COVID shock intervened). During the pandemic in 2020, BI’s rapid cuts to record-low rates initially coincided with market turmoil, but critically laid the groundwork for the sharp rebound in bank stocks in 2021 as recovery took hold. Now, with the 2024–2025 easing cycle underway, bank stocks are expected to repeat history.

2016-2017 rate cut cycle and bank share price index:

2019 rate cut cycle and bank share price index:

2020-2021 rate cut and pandemic cycle, and bank share price index:

For international investors who want to take advantage of these discounted valuations and high dividend yields, access to the Indonesian equity market usually comes through global stock brokers that provide trading on Asian exchanges or ADR instruments. Choosing a platform with reliable market access, competitive fees, and strong investor protection is an important step before building exposure to Indonesian bank stocks. The comparison below highlights several brokers that offer access to Indonesian equities and other global markets.

| Plus500 | CapTrader | EXANTE | UTEX | Freedom24 | Easy Equities | TradeZero | Revolut | Interactive Brokers | |

|---|---|---|---|---|---|---|---|---|---|

|

Foundation year |

2008 | 2001 | 2011 | 2020 | 2013 | 1998 | 2015 | 2015 | 1978 |

|

Account min. |

EUR500 | 2,000 | EUR10,000 | 10 | 1 | No | 500 | No | No |

|

Interest rate |

No | 1% | Varies | No | 7,08 | 3.50% | 9% | 0%-4% | 4.83% |

|

Basic stock/ETF fee |

$0.006 | $0.01 | From $0.02 | 0,02-0,04% | 0,02$/€+2 EUR / 0,25%+10HK$ | 0.25% | $0.005 | 0.12%-0.25% | 0-0,0035% |

|

Min. stock/ETF fee |

Not specified | $2 | $1 | 0,02% | 0,25% | R0.01 | $0.99 | £1.00/€1.00 | $1,00 |

|

Basic futures fee |

Not specified | €1 | From $1.5 | Not provided | Varies | Not specified | Not specified | No | $0,25 |

|

Min. futures fee |

Not specified | €1 | Not specified | Not provided | Varies | Not specified | Not specified | No | $0,25 |

|

Open an account |

Go to broker 80% of retail CFD accounts lose money. |

Go to broker Your capital is at risk.

|

Go to broker Your capital is at risk. |

Go to broker Your capital is at risk.

|

Go to broker Your capital is at risk.

|

Go to broker Your capital is at risk. |

Go to broker Your capital is at risk. |

Study review | Study review |

Indonesian bank stocks are undervalued

Accounting for the beginning of interest rate cut cycle (3x25bps rate cuts so far) and dividend yields exceeding the 10-year Indonesian Government Bond (INDOGB) yield, I recommend gradually accumulating positions in the sector. Indonesian bank shares now look mis‑priced, and the risk‑reward profile has become favourable for long‑term investors.

Indonesia’s major bank stocks appear to be undervalued: they are roughly 15% lower year‑over‑year, whereas the Jakarta Composite Index (JCI) is already up by almost 3%, driven mainly by conglomerates and the Prajogo Pangestu group stocks. Tight liquidity, decelerating loan growth, and massive net foreign outflow have all contributed to the correction.

However, the share price is expected to go north in the near future, supported by the cessation of foreign selling, attractive dividend yield – higher than both historical averages and long‑term government bond yields – and the dovish stance by the central bank.

Conclusion

Indonesian bank stocks are poised to deliver superior returns as the country enters a rate cut cycle, with dividend yields nearing 8% offering a compelling alternative to traditional fixed-income instruments. Investors seeking resilient growth and regular income should consider leading banks like Bank Central Asia and Bank Rakyat Indonesia, which combine strong fundamentals with attractive payouts. These financial giants are well-positioned to benefit from both expanding credit demand and improving margins in a lowering rate environment. Ultimately, reallocating capital from bonds into select Indonesian banks could unlock significantly higher total returns in the years ahead—making now the time to act for those aiming to stay ahead of the curve.

FAQs

What are the risks associated with investing in Indonesian bank stocks during periods of foreign capital outflow?

How do Indonesian bank stock valuations compare to historical averages?

Why might high dividend yields in Indonesian bank stocks be sustainable at current levels?

What impact does Indonesia's monetary policy have on the outlook for bank stocks?

Editors' Top Picks and Insights

Do politicians make the best stock traders?

Crypto test drive: How automakers are exploring digital assets

Lindsey Graham death: U.S. senator’s crypto legacy

Tether under pressure: USDT in Europe, audit questions, and the fight for trust

Lean Ethereum: Why Buterin wants to rebuild the network

SK Hynix debuts on Nasdaq: Largest U.S. offering by foreign company

Related Articles

Team that worked on the article

Andreas Kristo Saragih is a seasoned equity research analyst with over a decade of experience across both buy-side and sell-side roles, focused on the Indonesian capital market. He has extensive sector coverage, including banking, consumer goods, retail, real estate, healthcare, transportation, poultry, cement, pharmaceuticals, construction, and infrastructure.

Dan Blystone began his trading career in 1998 as an arbitrage clerk on the floor of the Chicago Mercantile Exchange (CME). He later traded bond and Eurex futures at proprietary firms such as Altea Trading, gaining valuable experience in high-frequency trading and risk management.

Chinmay Soni is a financial analyst with more than 5 years of experience in working with stocks, Forex, derivatives, and other assets. As a founder of a boutique research firm and an active researcher, he covers various industries and fields, providing insights backed by statistical data.

Ethereum is a decentralized blockchain platform and cryptocurrency that was proposed by Vitalik Buterin in late 2013 and development began in early 2014. It was designed as a versatile platform for creating decentralized applications (DApps) and smart contracts.

Index in trading is the measure of the performance of a group of stocks, which can include the assets and securities in it.

An investor is an individual, who invests money in an asset with the expectation that its value would appreciate in the future. The asset can be anything, including a bond, debenture, mutual fund, equity, gold, silver, exchange-traded funds (ETFs), and real-estate property.

Bitcoin is a decentralized digital cryptocurrency that was created in 2009 by an anonymous individual or group using the pseudonym Satoshi Nakamoto. It operates on a technology called blockchain, which is a distributed ledger that records all transactions across a network of computers.

Risk management is a risk management model that involves controlling potential losses while maximizing profits. The main risk management tools are stop loss, take profit, calculation of position volume taking into account leverage and pip value.

-

Afghanistan

Afghanistan

-

Albania

Albania

-

Algeria

Algeria

-

Angola

Angola

-

Argentina

Argentina

-

Armenia

Armenia

-

Australia

Australia

-

Austria

Austria

-

Azerbaijan

Azerbaijan

-

Bahamas

Bahamas

-

Bahrain

Bahrain

-

Bangladesh

Bangladesh

-

Belarus

Belarus

-

Belgium

Belgium

-

Bolivia

Bolivia

-

Botswana

Botswana

-

Brazil

Brazil

-

Brunei

Brunei

-

Bulgaria

Bulgaria

-

Cambodia

Cambodia

-

Cameroon

Cameroon

-

Canada

Canada

-

Chile

Chile

-

China

China

-

Colombia

Colombia

-

Congo

Congo

-

Costa Rica

Costa Rica

-

Cote d'Ivoire

Cote d'Ivoire

-

Croatia

Croatia

-

Cuba

Cuba

-

Cyprus

Cyprus

-

Czechia

Czechia

-

DR Congo

DR Congo

-

Denmark

Denmark

-

Dominican Republic

Dominican Republic

-

Ecuador

Ecuador

-

Egypt

Egypt

-

El Salvador

El Salvador

-

Estonia

Estonia

-

Eswatini

Eswatini

-

Ethiopia

Ethiopia

-

Finland

Finland

-

France

France

-

Georgia

Georgia

-

Germany

Germany

-

Ghana

Ghana

-

Greece

Greece

-

Haiti

Haiti

-

Hong Kong

Hong Kong

-

Hungary

Hungary

-

India

India

-

Indonesia

Indonesia

-

Iran, Islamic republic

Iran, Islamic republic

-

Iraq

Iraq

-

Ireland

Ireland

-

Israel

Israel

-

Italy

Italy

-

Jamaica

Jamaica

-

Japan

Japan

-

Jordan

Jordan

-

Kazakhstan

Kazakhstan

-

Kenya

Kenya

-

Korea

Korea

-

Kuwait

Kuwait

-

Kyrgyzstan

Kyrgyzstan

-

Laos

Laos

-

Latvia

Latvia

-

Lebanon

Lebanon

-

Lesotho

Lesotho

-

Libya

Libya

-

Lithuania

Lithuania

-

Luxembourg

Luxembourg

-

Madagascar

Madagascar

-

Malaysia

Malaysia

-

Malta

Malta

-

Mauritius

Mauritius

-

Mexico

Mexico

-

Moldova

Moldova

-

Mongolia

Mongolia

-

Montenegro

Montenegro

-

Morocco

Morocco

-

Mozambique

Mozambique

-

Myanmar

Myanmar

-

Namibia

Namibia

-

Nepal

Nepal

-

Netherlands

Netherlands

-

New Zealand

New Zealand

-

Nigeria

Nigeria

-

North Macedonia

North Macedonia

-

Norway

Norway

-

Oman

Oman

-

Pakistan

Pakistan

-

Palestine

Palestine

-

Panama

Panama

-

Papua New Guinea

Papua New Guinea

-

Paraguay

Paraguay

-

Peru

Peru

-

Philippines

Philippines

-

Poland

Poland

-

Portugal

Portugal

-

Puerto Rico

Puerto Rico

-

Qatar

Qatar

-

Reunion

Reunion

-

Romania

Romania

-

Rwanda

Rwanda

-

Saudi Arabia

Saudi Arabia

-

Serbia

Serbia

-

Singapore

Singapore

-

Slovakia

Slovakia

-

Slovenia

Slovenia

-

Somalia

Somalia

-

South Africa

South Africa

-

Spain

Spain

-

Sri Lanka

Sri Lanka

-

Sweden

Sweden

-

Switzerland

Switzerland

-

Syria

Syria

-

Taiwan

Taiwan

-

Tajikistan

Tajikistan

-

Tanzania

Tanzania

-

Thailand

Thailand

-

Trinidad and Tobago

Trinidad and Tobago

-

Tunisia

Tunisia

-

Turkey

Turkey

-

UAE

UAE

-

Uganda

Uganda

-

Ukraine

Ukraine

-

United Kingdom

United Kingdom

-

United States

-

Uruguay

Uruguay

-

Uzbekistan

Uzbekistan

-

Venezuela

Venezuela

-

Vietnam

Vietnam

-

Yemen

Yemen

-

Zambia

Zambia

-

Zimbabwe

Zimbabwe

- Forex

- Crypto