Drivers Behind Indonesia’s Equity Market Rally in July 2025

Editorial Note: While we adhere to strict Editorial Integrity, this post may contain references to products from our partners. Here's an explanation for How We Make Money. None of the data and information on this webpage constitutes investment advice according to our Disclaimer.

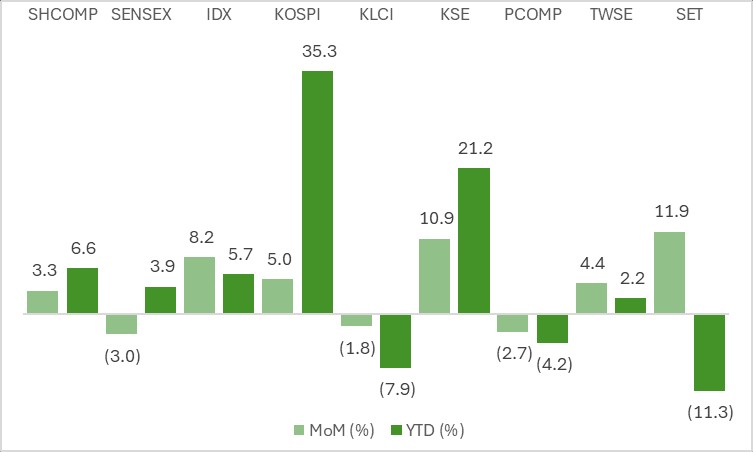

Indonesia’s Jakarta Composite Index (JCI) staged a standout rally in July 2025, emerging as one of the top-performing markets in Asia. The index jumped +8.23% MoM and turned positive at +5.71% YTD as of end-July, recovering from first-half losses. This performance placed JCI among the leaders in MSCI Emerging Market Asia.

JCI is still undervalued considering that many large-cap stocks have corrected YTD and valuations look inexpensive. Supportive central bank policy (2 rate cuts so far) and higher government spending is also projected to boost economic growth and drive the Indonesian MSCI Index to re-rate from the current valuation at over -2 S.D. below historical mean.

Low free-float conglomerates lead the rally

Indonesia, as one of the constituents of the MSCI Emerging Market (EM) Asia, bounced back in the beginning of 2H25. As of July 2025, the JCI reported +8.23% and +5.71% gains compared to June 2025 and EOY24. Such performance put the JCI in fourth place for YTD gains, behind Korea at +35.26%, Pakistan at +21.2% and China at +6.61%. For monthly gains, the JCI was behind SET and KSE, which reported +11.92% and +10.9% increases, respectively.

Indonesia’s impressive headline numbers tell only half the story. The JCI’s climb has been disproportionately driven by illiquid low free-float stocks. Key players include Barito Pacific group stocks such as Barito Pacific (BRPT), Chandra Asri Pacific (TPIA), Barito Renewables Energy (BREN), and Petrindo Jaya Kreasi (CUAN), Chandra Daya Investasi (CDIA)] along with other conglomerates like DCI Indonesia (DCII), Dian Swastatika Sentosa (DSSA).

| Code | Market Cap (IDRtr) | Price change (MoM) | Points to JCI |

|---|---|---|---|

| DCII | 826.5 | 128.11% | 209.7 |

| BREN | 1,046.9 | 33.19% | 73.8 |

| BRPT | 246.6 | 58.43% | 60.2 |

| DSSA | 499.3 | 20.95% | 43.0 |

| CDIA | 185.4 | 681.58% | 39.4 |

| ASII | 206.5 | 13.33% | 26.6 |

| PANI | 278.6 | 46.02% | 21.6 |

| GOTO | 74.1 | 12.07% | 15.0 |

| TLKM | 285.3 | 3.60% | 11.4 |

| CUAN | 172.6 | 21.63% | 11.2 |

| Code | Market Cap (IDRtr) | Price change (MoM) | Points to JCI |

|---|---|---|---|

| DCII | 826.5 | 723.57% | 355.02 |

| DSSA | 499.3 | 75.14% | 106.97 |

| BRPT | 246.6 | 185.87% | 106.09 |

| TPIA | 802.4 | 23.67% | 39.89 |

| CDIA | 185.4 | 681.58% | 39.36 |

| ANTM | 68.5 | 86.89% | 27.17 |

| MDKA | 57.8 | 46.13% | 20.81 |

| CASA | 56.4 | 83.19% | 20.05 |

| BNLI | 116.1 | 239.68% | 19.94 |

| TLKM | 285.3 | 6.27% | 18.85 |

A closer look at the JCI’s top three YTD mover

DCII is a leading data center operator and runs 7 data centers in 3 locations in the Java island, with total installed capacity 119 MW in 2023 – the largest in Indonesia. DCII plans to expand further toward a massive 1,000 MW capacity, mainly via new “hyperscale” campuses to meet booming digital demand. It boasts Tier IV facilities (the highest standard in reliability) and counts Amazon Web Services (AWS) as a strategic partner, positioning DCII to benefit from surging cloud and AI computing needs in Indonesia.

It is majority-owned by Otto Toto Sugiri with 30% ownership, followed by Marina Budiman (22.5%), Han Arming Hanafia (14%) and Anthoni Salim (11%). Meanwhile, public investors hold 22.5% of shares in the company.

The second major mover, Dian Swastatika Sentosa (DSSA), is a diversified conglomerate under the giant Sinarmas Group. Founded as a power utility arm, DSSA now operates across coal mining, power generation, digital services, chemicals, and renewables. Its core engine, however, remains coal: through subsidiaries like Golden Energy Mines (GEMS), DSSA produced 53.1 million tons in 2024, with coal sales accounting for a hefty 92% of revenue.

It is majority-owned by the Sinarmas Group (via Sinarmas Tunggal) with a 60% stake, followed by the public at 20%, with the remainder held as treasury shares.

Rounding out the top three is Barito Pacific (BRPT) – the flagship of the Barito Pacific Group controlled by billionaire Prajogo Pangestu. BRPT is a holding company with interests in petrochemicals, energy, and infrastructure. Its crown jewel is a majority stake in Chandra Asri (TPIA), Indonesia’s largest petrochemical producer. Barito Pacific also owns Star Energy (a leading geothermal energy producer, partially spun off as BREN in a recent IPO) and other assets, making it a proxy for both industrial and renewable themes.

Crucially, BRPT and its sister companies have become known for their stock market theatrics. The “Barito group” stocks earned a reputation in 2023–2025 as serial multi-baggers, with Pangestu’s Barito Group dubbed the market’s “ultimate commander” due to the sheer number of high-flying tickers under its umbrella.

Beware of the gap between value and price

Despite a scorching rally in July 2025, Indonesia’s equity market remains fundamentally undervalued. The headline index strength masks an important disconnect between value and price as much of the JCI’s recent climb has been driven by a few thinly traded conglomerate stocks rather than broad-based gains.

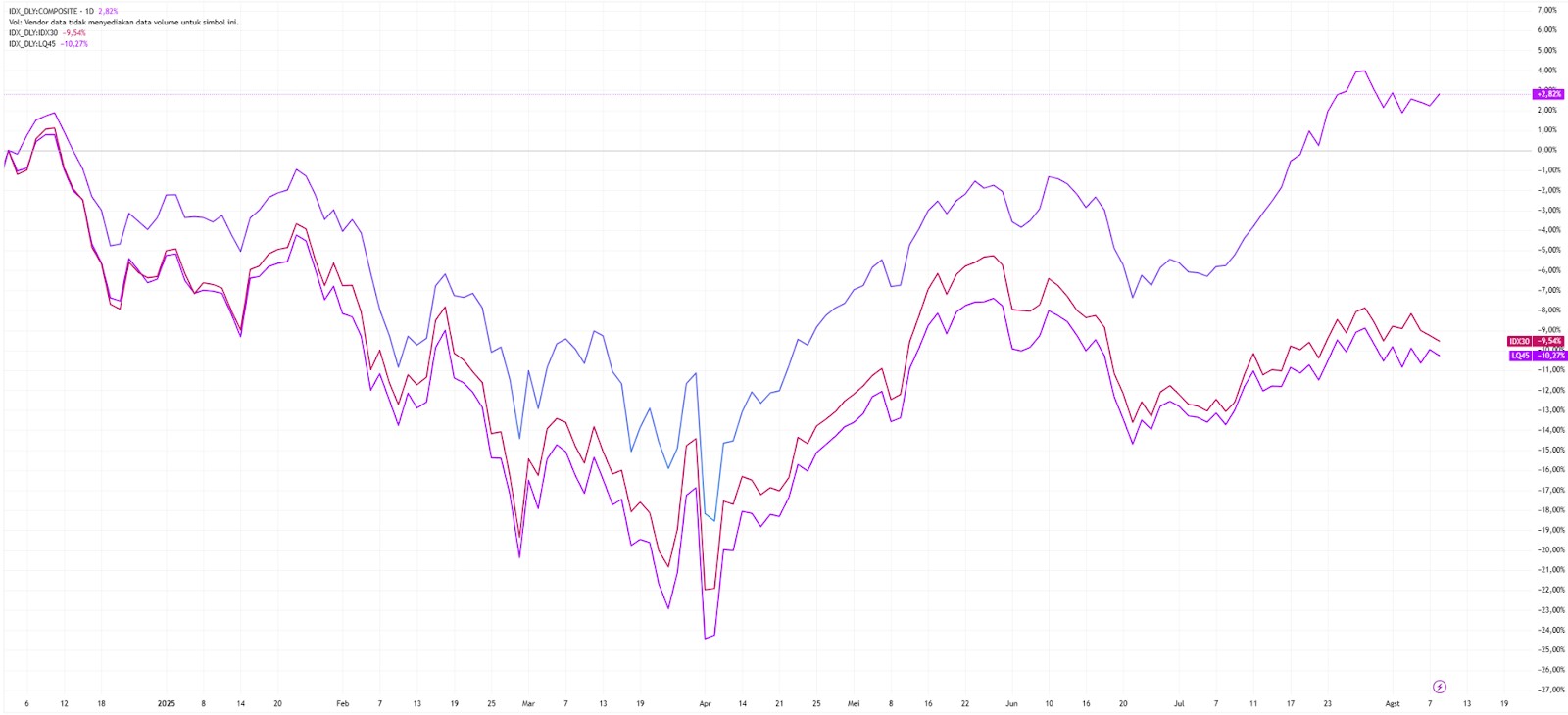

A handful of low free-float names have skewed the JCI’s performance, creating a misleading picture of resilience. The YTD top three market movers contributed roughly 568 points to the index on their own. If these speculative high-fliers are stripped out, the “real” JCI would be slightly above the 6,000 level – more than 20% lower than the official index reading. The divergence is also evident when comparing the JCI to Indonesia’s blue-chip indices like the LQ45 (top 45 liquid stocks) and IDX30 (top 30 by market cap).

Secondly, the MSCI Indonesia Index is currently trading at a forward P/E multiple more than two standard deviations below its historical mean. Such an extreme deviation into undervalued territory is rare and suggests oversold conditions. In the past, when valuations have fallen this far below long-term norms, the market often saw a strong rebound in subsequent periods as sentiment and value re-converged.

Part of the reason value lags price is continued foreign investor skepticism. Overseas investors have been net sellers of Indonesian stocks for most of the year, with especially heavy outflows from large-cap counters. This has left blue-chip valuations at multi-year lows. Many of Indonesia’s most prominent companies now trade at undemanding multiples while offering elevated dividend yields. For instance, an industry leader like Astra International (ASII) trades at only about 6x forward earnings with a P/B well under 1. A top state-owned bank is valued at roughly 9x earnings and 1.7x book, boasting a dividend yield near 9% – a yield even higher than the 10-year government bond rate. These figures underscore how pessimism and foreign selling have overshot fundamentals, leaving a wide gulf between current prices and intrinsic values.

Hold momentum stocks only short-term with high risk tolerance

I’ve been following emerging markets for years, and what’s happening in Indonesia right now is both exciting and tricky. I understand the temptation: a low-float stock in a growth sector can become a speculative darling and deliver eye-popping returns. However, I personally would be cautious chasing these names at current levels. Their valuations have disconnected from reality, and the rallies are built on very narrow trading activity. In my experience, such spikes can reverse violently when sentiment shifts. If you weren’t in them already, you’re taking on significant risk buying at the top.

On the other side, Indonesia’s blue-chip stocks look genuinely attractive now. Many large-cap stocks including big banks are trading at valuations I haven’t seen in a long time – low P/Es, high dividend yields – despite solid balance sheets and earnings. With the Bank Indonesia cutting rates and likely to cut more, the macro environment is turning supportive for these traditional sectors.

This divergence creates a sweet spot: I’d focus on accumulating quality large-caps on dips, rather than chasing the “hot” conglomerates. In practice, I recommend a barbell approach: keep a small exposure to a couple of the momentum names only if you have high risk tolerance and a short-term trading mindset, but anchor your portfolio in the fundamentally strong, undervalued blue-chips.

Conclusion

The JCI’s July 2025 rally was extraordinary on the surface. A cadre of low-float conglomerates engineered a sharp rise, masking the fact that many Indonesian equities remain depressed. Without those high-fliers, the JCI would be significantly lower, reflecting a market that is still finding its footing. The concentration of gains presents risks, but also opportunities: as monetary easing and improving sentiment draw attention back to fundamentals, the unloved majority of stocks could see a catch-up rally. A prudent strategy is to stay diversified, be mindful of the narrow breadth, and focus on long-term value. The rally in conglomerate stocks has been a spectacle, but the next leg for Indonesia may well belong to the broader market.

FAQs

Is it safe for me to put my money in those conglomerate stocks?

Investing in low-free-float and illiquid conglomerate stocks carries elevated risk. These shares have surged on speculative momentum and thin trading, so their prices can swing wildly. If you already have profits in them, it’s wise to set tight risk management. New investors should exercise caution – while gains have been huge, a sharp correction is possible since the valuations aren’t supported by fundamentals.

What are the signs that the rally in these conglomerate stocks might run out of gas?

Watch for liquidity and news catalysts. Signs include a noticeable drop in trading volumes (fewer buyers willing to pay higher prices), or if expected catalysts – like an index inclusion or stock split – actually occur (often the adage “buy the rumor, sell the news” applies). Also, if broader market sentiment improves and investors rotate back into blue-chip stocks, these high-fliers could lose steam as attention shifts elsewhere.

Are there any conglomerate stocks that potentially will move similarly to the abovementioned names?

Some market observers speculate that companies like PANI, CDIA, CBDK might attempt similar moves, as they also have low floats, hidden agenda (rights issue, stock split, or index inclusion) and influential owners.

Given the current condition, should I invest in conglomerate stocks or stick to blue-chip stocks?

It depends on your investment horizon and risk appetite. For short- to mid-term traders, the conglomerate stocks can be attractive for momentum plays – they’ve shown they can rally quickly (though the risks are high). For a long-term or more conservative investor, blue-chip stocks are generally the better choice now. Indonesia’s blue-chips (banks, consumer firms, etc.) offer solid fundamentals, dividends, and are trading at low valuations. They may not spike overnight, but they provide more stability and are well-positioned to rise as the economy and foreign investor sentiment improve.

Why does a low free float make a stock move so much?

“Free float” refers to the portion of shares available for public trading. When a stock has a low free float, there are relatively few shares that change hands. This means even small amounts of buying or selling can have a big impact on the price. In a low-float stock, if a wealthy investor or institution decides to buy aggressively, the scarcity of shares can push the price up extremely fast (and the reverse is true on selling). Low float, combined with bullish sentiment, is a recipe for volatility – that’s why stocks like DCII and DSSA, with most shares held by insiders, saw such outsized jumps in price.

Editors' Top Picks and Insights

Is Bitcoin right for you? Five traits shared by many cryptocurrency holders

Chasing hits: Why investors are losing interest in Netflix

Tokenized stocks in the spotlight: How do they work and are they worth trading?

Do politicians make the best stock traders?

Crypto test drive: How automakers are exploring digital assets

Lindsey Graham death: U.S. senator’s crypto legacy

Related Articles

Team that worked on the article

Andreas Kristo Saragih is a seasoned equity research analyst with over a decade of experience across both buy-side and sell-side roles, focused on the Indonesian capital market. He has extensive sector coverage, including banking, consumer goods, retail, real estate, healthcare, transportation, poultry, cement, pharmaceuticals, construction, and infrastructure.

One of the most widely respected and quoted currency experts, Marc Chandler has been analyzing and advising on the global capital markets for more than 30 years. Throughout his career on Wall Street, Chandler has advised private businesses, hedge funds and asset managers on navigating the foreign exchange market.

Chinmay Soni is a financial analyst with more than 5 years of experience in working with stocks, Forex, derivatives, and other assets. As a founder of a boutique research firm and an active researcher, he covers various industries and fields, providing insights backed by statistical data.

-

Afghanistan

Afghanistan

-

Albania

Albania

-

Algeria

Algeria

-

Angola

Angola

-

Argentina

Argentina

-

Armenia

Armenia

-

Australia

Australia

-

Austria

Austria

-

Azerbaijan

Azerbaijan

-

Bahamas

Bahamas

-

Bahrain

Bahrain

-

Bangladesh

Bangladesh

-

Belarus

Belarus

-

Belgium

Belgium

-

Bolivia

Bolivia

-

Botswana

Botswana

-

Brazil

Brazil

-

Brunei

Brunei

-

Bulgaria

Bulgaria

-

Cambodia

Cambodia

-

Cameroon

Cameroon

-

Canada

Canada

-

Chile

Chile

-

China

China

-

Colombia

Colombia

-

Congo

Congo

-

Costa Rica

Costa Rica

-

Cote d'Ivoire

Cote d'Ivoire

-

Croatia

Croatia

-

Cuba

Cuba

-

Cyprus

Cyprus

-

Czechia

Czechia

-

DR Congo

DR Congo

-

Denmark

Denmark

-

Dominican Republic

Dominican Republic

-

Ecuador

Ecuador

-

Egypt

Egypt

-

El Salvador

El Salvador

-

Estonia

Estonia

-

Eswatini

Eswatini

-

Ethiopia

Ethiopia

-

Finland

Finland

-

France

France

-

Georgia

Georgia

-

Germany

Germany

-

Ghana

Ghana

-

Greece

Greece

-

Haiti

Haiti

-

Hong Kong

Hong Kong

-

Hungary

Hungary

-

India

India

-

Indonesia

Indonesia

-

Iran, Islamic republic

Iran, Islamic republic

-

Iraq

Iraq

-

Ireland

Ireland

-

Israel

Israel

-

Italy

Italy

-

Jamaica

Jamaica

-

Japan

Japan

-

Jordan

Jordan

-

Kazakhstan

Kazakhstan

-

Kenya

Kenya

-

Korea

Korea

-

Kuwait

Kuwait

-

Kyrgyzstan

Kyrgyzstan

-

Laos

Laos

-

Latvia

Latvia

-

Lebanon

Lebanon

-

Lesotho

Lesotho

-

Libya

Libya

-

Lithuania

Lithuania

-

Luxembourg

Luxembourg

-

Madagascar

Madagascar

-

Malaysia

Malaysia

-

Malta

Malta

-

Mauritius

Mauritius

-

Mexico

Mexico

-

Moldova

Moldova

-

Mongolia

Mongolia

-

Montenegro

Montenegro

-

Morocco

Morocco

-

Mozambique

Mozambique

-

Myanmar

Myanmar

-

Namibia

Namibia

-

Nepal

Nepal

-

Netherlands

Netherlands

-

New Zealand

New Zealand

-

Nigeria

Nigeria

-

North Macedonia

North Macedonia

-

Norway

Norway

-

Oman

Oman

-

Pakistan

Pakistan

-

Palestine

Palestine

-

Panama

Panama

-

Papua New Guinea

Papua New Guinea

-

Paraguay

Paraguay

-

Peru

Peru

-

Philippines

Philippines

-

Poland

Poland

-

Portugal

Portugal

-

Puerto Rico

Puerto Rico

-

Qatar

Qatar

-

Reunion

Reunion

-

Romania

Romania

-

Rwanda

Rwanda

-

Saudi Arabia

Saudi Arabia

-

Serbia

Serbia

-

Singapore

Singapore

-

Slovakia

Slovakia

-

Slovenia

Slovenia

-

Somalia

Somalia

-

South Africa

South Africa

-

Spain

Spain

-

Sri Lanka

Sri Lanka

-

Sweden

Sweden

-

Switzerland

Switzerland

-

Syria

Syria

-

Taiwan

Taiwan

-

Tajikistan

Tajikistan

-

Tanzania

Tanzania

-

Thailand

Thailand

-

Trinidad and Tobago

Trinidad and Tobago

-

Tunisia

Tunisia

-

Turkey

Turkey

-

UAE

UAE

-

Uganda

Uganda

-

Ukraine

Ukraine

-

United Kingdom

United Kingdom

-

United States

-

Uruguay

Uruguay

-

Uzbekistan

Uzbekistan

-

Venezuela

Venezuela

-

Vietnam

Vietnam

-

Yemen

Yemen

-

Zambia

Zambia

-

Zimbabwe

Zimbabwe

- Forex

- Crypto