Is Bitcoin’s 4-Year Cycle Dead?

Editorial Note: While we adhere to strict Editorial Integrity, this post may contain references to products from our partners. Here's an explanation for How We Make Money. None of the data and information on this webpage constitutes investment advice according to our Disclaimer.

Bitcoin’s traditional 4-year cycle – driven by halving events that cut new coin issuance – may be fading as institutional capital reshapes market behavior. Analysts note that halvings now have a smaller effect on supply, while ETFs and macroeconomic factors exert greater influence on price movements. Instead of repeating predictable boom-and-bust patterns, Bitcoin appears to be evolving into a more mature, liquidity-driven asset whose performance increasingly mirrors global financial markets.

Throughout the history of the crypto market, everything has tended to move in four-year cycles around Bitcoin’s halving events. This is a preprogrammed aspect of bitcoin’s issuance policy where the amount of new bitcoin created every 210,000 blocks, which comes out to roughly every four years based on the targeted ten-minute block time, is cut in half.

Notably, this aspect of bitcoin’s monetary policy tends to control the movements of the entire crypto market rather than just bitcoin itself. While other crypto assets have their own internal dynamics at play, they still tend to follow the lead of the world’s first and largest cryptocurrency when it comes to longer-term trends.

For example, Ethereum (ETH) performed rather poorly in the lead up to the finalization of its move to proof-of-stake in September 2022, despite the deflationary effects the change was going to have on the ETH asset itself. This should have been viewed as a positive development for ETH’s supply dynamics, but the bitcoin bull market had ended after peaking around $69,000 in November 2021 and brought the rest of the crypto market down with it as it eventually fell below $20,000 one year later – around the time of crypto exchange FTX’s bankruptcy filing.

With all that said, there are many analysts who now agree that the four-year crypto cycle that has been centered around Bitcoin’s halving events is coming to an end. This is due to two main contributing factors: the halvings themselves are less impactful on bitcoin’s rate of issuance and the institutional money that has entered the market is simply too overwhelming.

Halvings are less impactful

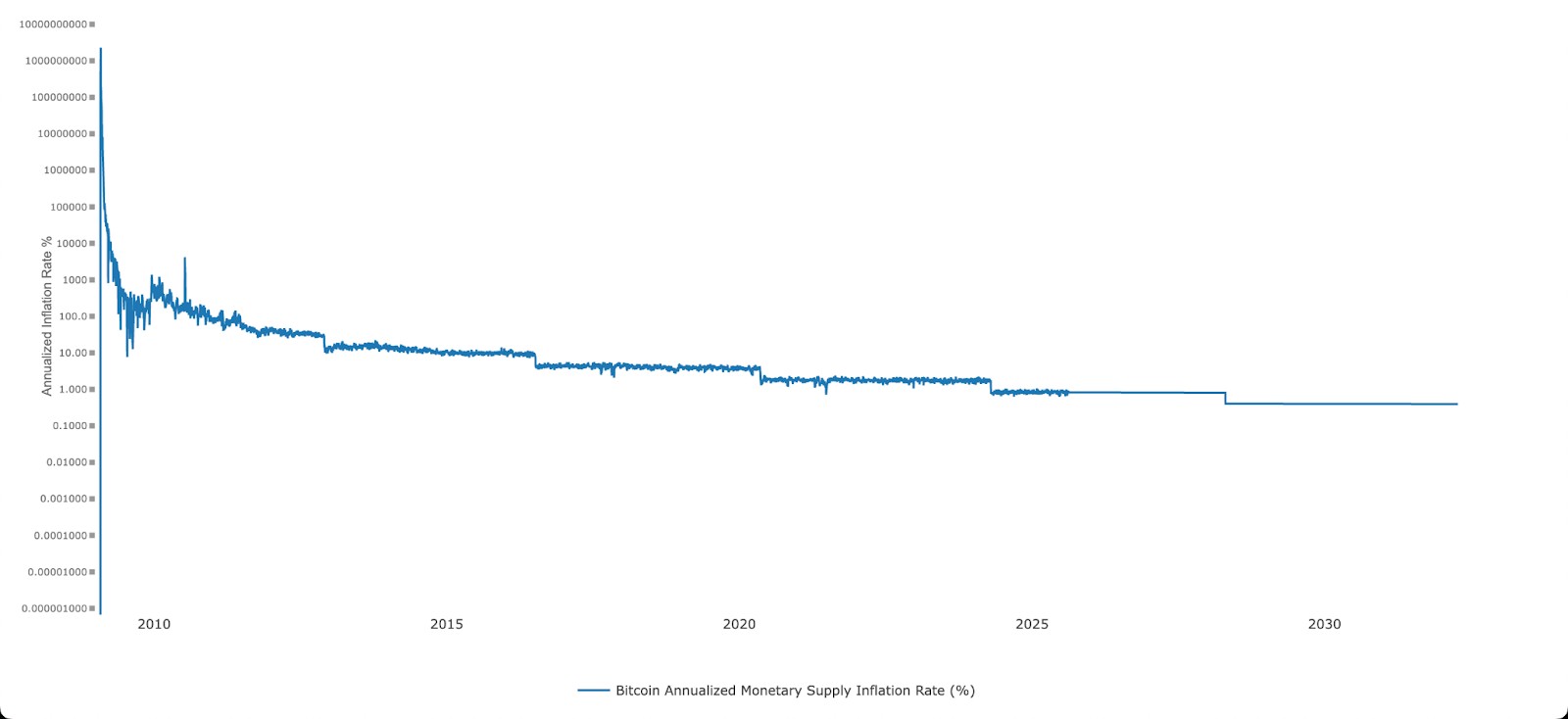

The issuance rate of new bitcoin declines over time, but that rate has already declined quite substantially from the early days. Bitcoin’s rate of issuance was astronomical when the crypto network first launched, as was required for an asset going from zero to a few million units in a matter of years. After settling down to roughly 10% in the early 2010s, the annual rate of issuance has now fallen below 1% for the first time after the most recent halving in April 2024.

In the past, Bitcoin halvings have caused supply shocks on the market, as the amount of new bitcoin being generated by miners was cut in half overnight. However, the actual change in the issuance rate also declines over time. The first halving cut the amount of new bitcoin created in each block by 25, while the most recent halving only saw a decline of 3.125 bitcoin. Additionally, that smaller cut in issuance is also measured against a further expanded supply of existing bitcoin.

Notably, the magnitude of each major bitcoin bull cycle up to this point – with local tops hit in 2013, 2017, 2021, and 2025 – has been smaller than the previous cycle’s, as bitcoin has followed a process of diminishing returns. Additionally, the most recent halving was the first time the bitcoin price had hit a new all-time high prior to the halving event (rather than in the months that followed it).

| Month | Minimum Price, $ | Average Price, $ | Maximum Price, $ |

|---|---|---|---|

| August 2026 | 28 | 28 | 29 |

| September 2026 | 30 | 30 | 31 |

| October 2026 | 29 | 30 | 30 |

| November 2026 | 31 | 32 | 32 |

| December 2026 | 28 | 29 | 29 |

Institutional money has entered the market

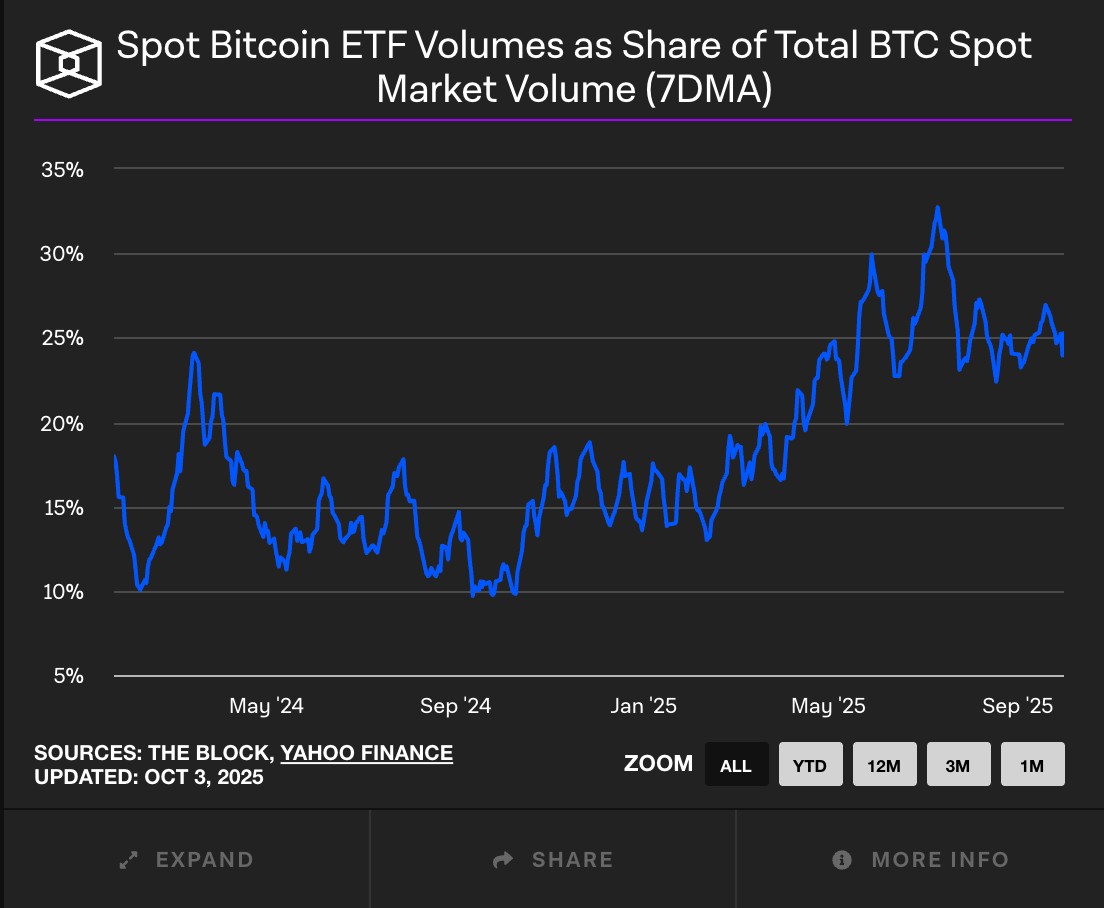

On top of the halving dynamics, much larger amounts of money are now affecting bitcoin price movements, especially with the introduction of the Bitcoin exchange-traded funds (ETFs) in the U.S. According to data from The Block, the U.S.-based ETFs now account for roughly 25% of spot bitcoin trading volume. BlackRock’s iShares BitcoinTrust (IBIT) has been the main driver of institutional demand, holding more than $90 billion worth of bitcoin in its fund.

The scale of institutional money that has entered the market dwarfs the kind of money that used to be associated with the sector, which provides greater levels of liquidity and makes it more difficult for one entity to move the price in either direction.

Now that bitcoin is more closely associated with traditional markets, it’s clear that the whims of these institutional players and macroeconomic considerations will have more say over the bitcoin price than the cryptocurrency’s own supply dynamics. These altered dynamics enabled by bitcoin ETF approvals in the U.S. were explained in a report from Coinbase prior to the most recent halving event.

As Bitcoin increasingly integrates with global financial markets, access to reliable trading platforms becomes an important consideration for both retail and institutional participants. Liquidity, trading fees, available derivatives, and security standards can significantly affect trading efficiency and risk management. The comparison below highlights several cryptocurrency exchanges where investors can trade Bitcoin and other digital assets under competitive conditions.

| Kraken | OKX | BTCC | Coinbase | Nebeus | |

|---|---|---|---|---|---|

|

Demo account |

No | Yes | Yes | No | No |

|

Coins Supported |

278 | 329 | 399 | 249 | 30 |

|

Min. Deposit, $ |

10 | 10 | 10 | 10 | 5 |

|

Spot leverage |

1:5 | 1:10 | 1:1 | 1:3 | 1:Not available |

|

Spot Maker Fee, % |

0.25 | 0.08 | 0.2 | 0.5 | Not available |

|

Spot Taker fee, % |

0.4 | 0.1 | 0.3 | 0.5 | Not available |

|

TU overall score |

9.2 | 8.9 | 7.84 | 7.68 | 7.6 |

|

Open an account |

Go to broker Your capital is at risk. |

Go to broker Your capital is at risk. |

Go to broker Your capital is at risk.

|

Go to broker Your capital is at risk. |

Go to broker Your capital is at risk.

|

What happens next?

To be clear, whether the four-year cycles are over for bitcoin is still unknown, as this current cycle has yet to reach its final stages. That said, market observers should have a better grasp on whether the four-year cycle will continue or if there is a “new normal” by the end of the year. In the previous three cycles, the bull market reversed course in the last quarter of the calendar year in rather dramatic fashion.

While some have theorized that a collapse in the digital asset treasury (DAT) company market could cause a sharp reversal in bitcoin’s upward trajectory this time around, there has yet to be much sign of trouble in that sector up to this point.

As indicated by a new joint report from Checkonchain and Unchained, it’s still possible bitcoin could rise much further from its current price level around $120,000; however, it’s less clear if the usual mania will occur in the closing months of the year or if a slow and steady rise could continue beyond the usual four-year window.

Bitcoin News

Bitcoin stabilizes as geopolitical risks offset improving institutional demand

Crypto test drive: How automakers are exploring digital assets

Solo miner earns about $200,000 with $150 Bitcoin mining device

Why is Bitcoin flat today? Support test at $62,603 keeps buyers active

U.S. government transfers $300 million in seized crypto assets to Coinbase

Strategy sells $467 million in stock but leaves Bitcoin untouched

Investors should stop fixating on the calendar and start focusing on liquidity cycles

As someone who has followed Bitcoin’s evolution for over a decade, I believe we’re entering an entirely new phase – one defined less by programmed scarcity and more by global capital flows. The four-year cycle was a product of Bitcoin’s adolescence: a simple feedback loop between halving events, media attention, and retail speculation. That rhythm worked when liquidity was thin and narratives drove sentiment. But today, the market’s heartbeat is set by different forces – interest rate policy, ETF inflows, and institutional allocation strategies.

From my perspective, investors should stop fixating on the calendar and start focusing on liquidity cycles and risk appetite across global markets. Bitcoin has effectively become a macro asset, and its price behavior will increasingly mirror the same patterns that govern equities, bonds, and gold. This doesn’t mean the halving is irrelevant – it still affects miner economics and long-term supply – but its role as a timing mechanism for bull and bear markets is fading.

If I had to make a forward-looking call, I’d say we’re heading into an era where Bitcoin trades more like digital gold than a speculative tech bet. Price growth may become steadier, less explosive, but also more sustainable. Those expecting another “post-halving moonshot” might be disappointed, but those who adapt to this structural maturity will likely find greater stability – and potentially longer-term opportunity – in the years ahead.

Conclusion

The era when Bitcoin’s price action was dictated by its rigid 4-year halving cycle may be coming to a close, as institutional investors and ETFs introduce fresh forces to the market. With each halving appearing to wield less influence, recent surges and corrections now often correlate more closely with institutional activity—such as spot ETF approvals—than code-driven supply shocks. This shift challenges long-held assumptions and signals that market participants must adapt, analyzing broader financial flows and sentiment over simplistic cycle predictions. Ultimately, Bitcoin’s future may depend less on mathematical inevitability and more on its adoption by mainstream capital, redefining what drives the digital gold’s value in a new era.

FAQs

How have liquidity cycles started to influence Bitcoin’s price movements?

What are the implications of Bitcoin behaving more like a macro asset?

How might miner economics be affected as halving events become less impactful?

What changes should investors consider in their approach as Bitcoin transitions to a mature market?

Editors' Top Picks and Insights

Crypto test drive: How automakers are exploring digital assets

Lindsey Graham death: U.S. senator’s crypto legacy

Tether under pressure: USDT in Europe, audit questions, and the fight for trust

Lean Ethereum: Why Buterin wants to rebuild the network

SK Hynix debuts on Nasdaq: Largest U.S. offering by foreign company

SpaceX falls out of orbit: Does anyone still want Musk’s stock?

Related Articles

Team that worked on the article

Kyle began exploring Bitcoin in 2013, when public interest in cryptocurrencies was just beginning to grow. At first, it was more of a hobby.

Dan Blystone began his trading career in 1998 as an arbitrage clerk on the floor of the Chicago Mercantile Exchange (CME). He later traded bond and Eurex futures at proprietary firms such as Altea Trading, gaining valuable experience in high-frequency trading and risk management.

Chinmay Soni is a financial analyst with more than 5 years of experience in working with stocks, Forex, derivatives, and other assets. As a founder of a boutique research firm and an active researcher, he covers various industries and fields, providing insights backed by statistical data.

Index in trading is the measure of the performance of a group of stocks, which can include the assets and securities in it.

Cryptocurrency is a type of digital or virtual currency that relies on cryptography for security. Unlike traditional currencies issued by governments (fiat currencies), cryptocurrencies operate on decentralized networks, typically based on blockchain technology.

CFD is a contract between an investor/trader and seller that demonstrates that the trader will need to pay the price difference between the current value of the asset and its value at the time of contract to the seller.

Forex leverage is a tool enabling traders to control larger positions with a relatively small amount of capital, amplifying potential profits and losses based on the chosen leverage ratio.

A bear market is a period of time in which an investment asset, such as stocks, bonds, or commodities, experiences a decline in price for an extended period of time.

-

Afghanistan

Afghanistan

-

Albania

Albania

-

Algeria

Algeria

-

Angola

Angola

-

Argentina

Argentina

-

Armenia

Armenia

-

Australia

Australia

-

Austria

Austria

-

Azerbaijan

Azerbaijan

-

Bahamas

Bahamas

-

Bahrain

Bahrain

-

Bangladesh

Bangladesh

-

Belarus

Belarus

-

Belgium

Belgium

-

Bolivia

Bolivia

-

Botswana

Botswana

-

Brazil

Brazil

-

Brunei

Brunei

-

Bulgaria

Bulgaria

-

Cambodia

Cambodia

-

Cameroon

Cameroon

-

Canada

Canada

-

Chile

Chile

-

China

China

-

Colombia

Colombia

-

Congo

Congo

-

Costa Rica

Costa Rica

-

Cote d'Ivoire

Cote d'Ivoire

-

Croatia

Croatia

-

Cuba

Cuba

-

Cyprus

Cyprus

-

Czechia

Czechia

-

DR Congo

DR Congo

-

Denmark

Denmark

-

Dominican Republic

Dominican Republic

-

Ecuador

Ecuador

-

Egypt

Egypt

-

El Salvador

El Salvador

-

Estonia

Estonia

-

Eswatini

Eswatini

-

Ethiopia

Ethiopia

-

Finland

Finland

-

France

France

-

Georgia

Georgia

-

Germany

Germany

-

Ghana

Ghana

-

Greece

Greece

-

Haiti

Haiti

-

Hong Kong

Hong Kong

-

Hungary

Hungary

-

India

India

-

Indonesia

Indonesia

-

Iran, Islamic republic

Iran, Islamic republic

-

Iraq

Iraq

-

Ireland

Ireland

-

Israel

Israel

-

Italy

Italy

-

Jamaica

Jamaica

-

Japan

Japan

-

Jordan

Jordan

-

Kazakhstan

Kazakhstan

-

Kenya

Kenya

-

Korea

Korea

-

Kuwait

Kuwait

-

Kyrgyzstan

Kyrgyzstan

-

Laos

Laos

-

Latvia

Latvia

-

Lebanon

Lebanon

-

Lesotho

Lesotho

-

Libya

Libya

-

Lithuania

Lithuania

-

Luxembourg

Luxembourg

-

Madagascar

Madagascar

-

Malaysia

Malaysia

-

Malta

Malta

-

Mauritius

Mauritius

-

Mexico

Mexico

-

Moldova

Moldova

-

Mongolia

Mongolia

-

Montenegro

Montenegro

-

Morocco

Morocco

-

Mozambique

Mozambique

-

Myanmar

Myanmar

-

Namibia

Namibia

-

Nepal

Nepal

-

Netherlands

Netherlands

-

New Zealand

New Zealand

-

Nigeria

Nigeria

-

North Macedonia

North Macedonia

-

Norway

Norway

-

Oman

Oman

-

Pakistan

Pakistan

-

Palestine

Palestine

-

Panama

Panama

-

Papua New Guinea

Papua New Guinea

-

Paraguay

Paraguay

-

Peru

Peru

-

Philippines

Philippines

-

Poland

Poland

-

Portugal

Portugal

-

Puerto Rico

Puerto Rico

-

Qatar

Qatar

-

Reunion

Reunion

-

Romania

Romania

-

Rwanda

Rwanda

-

Saudi Arabia

Saudi Arabia

-

Serbia

Serbia

-

Singapore

Singapore

-

Slovakia

Slovakia

-

Slovenia

Slovenia

-

Somalia

Somalia

-

South Africa

South Africa

-

Spain

Spain

-

Sri Lanka

Sri Lanka

-

Sweden

Sweden

-

Switzerland

Switzerland

-

Syria

Syria

-

Taiwan

Taiwan

-

Tajikistan

Tajikistan

-

Tanzania

Tanzania

-

Thailand

Thailand

-

Trinidad and Tobago

Trinidad and Tobago

-

Tunisia

Tunisia

-

Turkey

Turkey

-

UAE

UAE

-

Uganda

Uganda

-

Ukraine

Ukraine

-

United Kingdom

United Kingdom

-

United States

-

Uruguay

Uruguay

-

Uzbekistan

Uzbekistan

-

Venezuela

Venezuela

-

Vietnam

Vietnam

-

Yemen

Yemen

-

Zambia

Zambia

-

Zimbabwe

Zimbabwe

- Forex

- Crypto