How Fed Market Interventions Shape Markets And The Economy

Editorial Note: While we adhere to strict Editorial Integrity, this post may contain references to products from our partners. Here's an explanation for How We Make Money. None of the data and information on this webpage constitutes investment advice according to our Disclaimer.

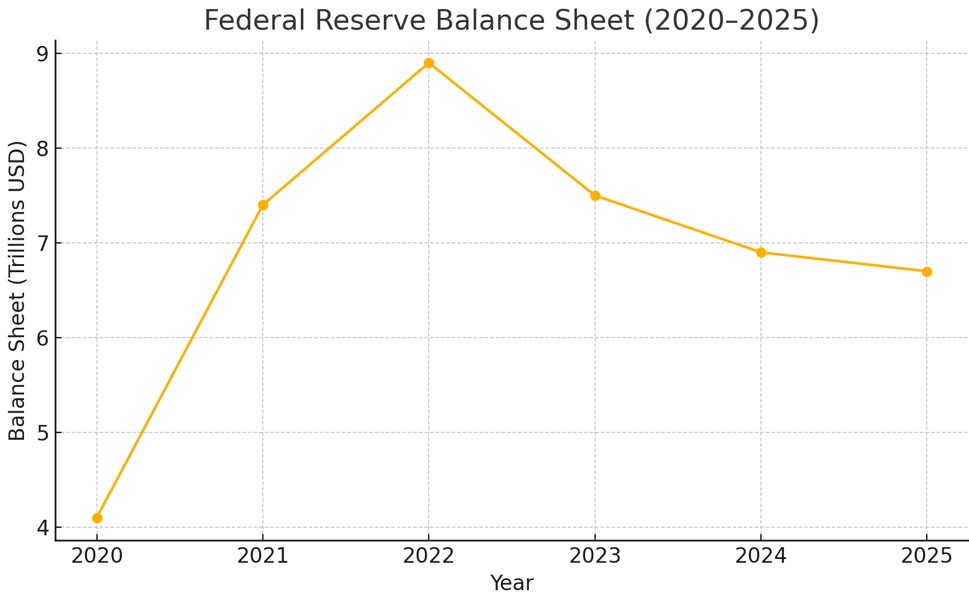

In 2020, the Fed expanded its balance sheet by more than $3.3 trillion, reaching $7.4 trillion, supported by $1.5 trillion in repo operations and credit support programs. By 2025, as quantitative tightening resumed, the balance sheet fell to $6.7 trillion. These Fed interventions played a key role in stabilizing corporate credit and restoring investor confidence during turbulent times.

Actions by the Federal Reserve are crucial for maintaining stability in the U.S. financial system, particularly in periods of economic stress. These measures include liquidity operations, emergency lending, and asset purchases. A significant wave of such measures occurred during the COVID-19 pandemic, reshaping market dynamics and influencing investor behavior.

The term “Fed intervention” generally refers to policy actions designed to ensure market functionality rather than solely targeting inflation. In certain circumstances, these interventions can affect the behavior of entire asset classes. Similar operations involving the U.S. dollar, often called dollar intervention, can also influence exchange rates and international capital flows, highlighting the Fed’s broad impact on both domestic and global markets.

Historical context

The Fed’s modern intervention toolkit emerged during the 2008–2009 financial crisis. When traditional rate cuts hit the zero lower bound, the Fed pioneered quantitative easing (QE), buying long-term Treasuries and mortgages to lower yields and stimulate borrowing. It also introduced forward guidance to reassure markets about future policy. Between 2008 and 2014, the Fed’s balance sheet expanded to roughly $4.5 trillion, normalizing only gradually after 2015. This period provided crucial lessons in crisis management and the importance of acting decisively.

By 2020, the Fed was able to apply these lessons rapidly. As markets froze in mid-March, the Fed cut rates to zero, launched open-ended asset purchases, and activated both old and new emergency facilities within weeks, a far more aggressive pace than during the 2008 crisis. This demonstrated the maturity of the Fed’s crisis playbook and its readiness to deploy liquidity tools at record speed to stabilize markets.

A practical illustration of Fed intervention can be seen in corporate liquidity support during the pandemic. Investment-grade credit markets seized up, leaving even high-grade companies facing steep borrowing costs. The Fed’s emergency facilities, such as the Secondary Market Corporate Credit Facility (SMCCF), restored confidence and reopened funding channels.

How Fed intervention “saved” Carnival

What the Fed did

Announced bond backstops (PMCCF/SMCCF) on Mar 23 and expanded them Apr 9, signaling it would buy corporate bonds/ETFs and restore secondary-market liquidity. Spreads fell and dealers re-entered the market.

What that changed in markets

The announcements compressed credit and bid-ask spreads and reopened primary issuance, especially for firms suddenly shut out of funding.

How Carnival used the window

With the market thawing, Carnival raised $4.0B of 11.5% first-lien secured notes (due 2023), plus $2.0125B of 5.75% convertible notes, and $575M of equity – a total ~$6.6B liquidity bridge while operations were largely halted.

The Fed didn’t bail out Carnival directly; it stabilized credit conditions so Carnival could access private capital at very high – but available – terms. In short: the Fed intervention saved Carnival.

By 2025, quantitative tightening (QT) had run down the asset stock by roughly $2.3T from peak. The composition of the Fed’s holdings also shifted. As of early 2025, roughly $4.24T were U.S. Treasury securities and $2.19T were agency mortgage-backed securities. Facilities set up for the crisis (such as corporate or municipal credit backstops) have largely wound down, leaving the Fed holding mostly traditional liquid securities.

Overall, the Fed’s balance sheet actions from 2020–2025 underline a cycle of explosive expansion (to stabilize markets) followed by gradual normalization. By holding securities and rolling over maturing debt, the Fed flooded the financial system with reserves in the crisis’s early phase, then later allowed those securities to mature without reinvestment, shrinking the balance sheet.

Current tools and strategies

In 2020, the Fed executed unprecedented purchase programs, buying nearly $2 trillion in Treasuries, far exceeding any prior QE program. Purchases were conducted at prices significantly lower than market offers, demonstrating the Fed’s capacity to influence yields across the curve and anchor market expectations.

Repo and reserve management. The Fed shifted to an “ample reserves” regime, using administered rates and daily repos to manage reserve supply. Repos ensured that reserves remained sufficient and supported the smooth functioning of short-term U.S. dollar funding markets. In July 2021, the Fed institutionalized a Standing Repo Facility (SRF), offering overnight liquidity against collateral to serve as a permanent backstop for money markets.

Interest on reserves and reverse repurchase program. To maintain control over policy rates in an abundant-reserves environment, the Fed relies on interest on excess reserves (IOR) and an overnight reverse repurchase program (ON RRP). These tools set a floor for money markets, providing a mechanism to anchor short-term rates. For instance, in March 2020, the Fed set ON RRP rates at 0% with very high counterparty limits to ensure smooth functioning.

Forward guidance and inflation framework. The Fed implemented new signaling strategies, including average inflation targeting, to communicate that rates would remain low until employment and inflation objectives were met. Although not a balance sheet tool, forward guidance magnified the impact of liquidity injections by shaping market expectations about future policy.

Integration of quantitative and technical tools. The Fed’s toolkit now combines large-scale asset purchases with technical mechanisms such as the floor system and SRF. These tools were tested under periods of market stress and later institutionalized to provide a reliable funding backstop.

Crisis preparedness and liquidity safety net. By blending traditional quantitative interventions with modern technical instruments, the Fed has created a more robust framework to respond to future crises. The combination of liquidity provision, policy signaling, and structural facilities ensures that funding markets have a standing safety net, reducing the likelihood of disruptions seen in prior decades.

The evolution of the Fed’s operating toolkit reflects a shift from reactive measures to a proactive, structured system. Open market purchases, repo operations, IOR/ON RRP tools, and forward guidance collectively strengthen the Fed’s ability to manage liquidity and maintain financial stability. Institutionalizing mechanisms like the SRF ensures readiness for future stress events, enhancing the resilience of U.S. short-term funding markets.

Fed market intervention

Short-term funding markets were a focal point. In late 2019 money markets briefly spiked, prompting the Fed to resume significant repo operations. By March 2020 the situation intensified: U.S. repo rates had surged due to cash shortages. On March 12–13, 2020 the Fed announced massive repo injections, effectively $1.5 trillion over just a few days. For example, on March 12 it offered $500 billion in 3‑month repos, then on March 13 an additional $500 billion (3‑month) and $500 billion (1‑month). Simultaneously it increased daily overnight repo to $175 billion. These steps flooded the banking system with dollars so that institutions could meet liquidity needs. The result: repo rates quickly normalized and a broader money-market freeze was averted.

This intervention underscores how the Fed will pump reserves into any plumbing that threatens systemic stability. By contrast to price-only tools, these operations inject liquidity directly where needed. The Fed has since made such backstops permanent: its standing repo facility (SRF, as noted above) provides a guaranteed daily avenue for eligible institutions to obtain cash. These repo actions (both emergency injections and the new facility) are central to the Fed’s toolkit for ensuring short-term funding markets never seize up again.

Key impacts on corporate credit and bond markets

Fed interventions in 2020 had a profound effect on corporate credit, transforming a frozen market into a functioning one and lowering borrowing costs across the spectrum. Key outcomes include:

Narrowed spreads. Credit spreads, which represent the extra yield over Treasuries, spiked to historic levels in early 2020 as liquidity dried up. For instance, the Bloomberg U.S. Corporate IG index spread exceeded 400 bps in March 2020; by July it tightened to below 150 bps, an over-250 bp decline. Even riskier “BBB” bonds saw yields drop from ~6% to under 3.5%. By late 2024, IG spreads reached 19-year lows, reflecting strong market confidence.

Resumed issuance. High-grade issuers quickly returned to the market following Fed programs. Boeing raised $25B and Carnival ~$6B within months of announcements, while many other corporations and banks used the liquidity to refinance debt or fund operations. The availability of capital encouraged widespread issuance.

Backstop effect. The Fed’s direct purchases of corporate bonds were relatively small, yet the signaling effect was enormous. Announcements of the PMCCF and SMCCF programs reassured investors that the Fed was effectively insuring the market. The NY Fed noted that spreads collapsed immediately after the announcement, even before any actual purchases.

Support for fallen angels. Companies downgraded from investment grade (“fallen angels”) found willing buyers, stabilizing a segment that might otherwise have faced prohibitively high borrowing costs. This ensured continued access to credit across the risk spectrum.

Restored market confidence. Targeted interventions restored normal market functioning by reducing panic, enhancing liquidity, and reassuring investors. Credit markets, initially closed due to uncertainty, reopened efficiently.

Stock market response

Equity markets rebounded sharply after the March 2020 lows. The S&P 500 fell 34% from its February peak but regained its previous high within six months. While the Fed did not buy stocks, the perception of a Fed intervention and its stock market effect emerged as investors anticipated support during downturns.

This expectation, referred to as the Fed put, differs from other central bank strategies that rarely prioritize asset price stability directly.

Political and currency dimensions

Although the Federal Reserve did not engage in formal dollar intervention, meaning direct buying or selling of USD in foreign exchange markets, as its extraordinary liquidity measures in 2020 had a significant impact on the dollar's value.

The U.S. Dollar Index (DXY) peaked at 102.8 in March 2020 during the market panic.

Following Fed asset purchases and credit facility launches, DXY fell steadily, reaching 89.2 by December 2020, a decline of over 13% in less than 9 months.

This depreciation occurred without official currency operations and was driven by increased dollar supply and reduced demand for dollar-denominated safe assets. The weaker dollar:

Boosted U.S. exporters by making American goods more competitive.

Provided relief to emerging markets, many of which have debt obligations denominated in USD.

By 2023, as the Fed transitioned to quantitative tightening, DXY recovered slightly, hovering around 103–104 in mid-2024, reflecting a shift back to a more neutral stance. Want to trade around Fed-driven moves? Start with a broker that’s regulated in your country, offers tight spreads on USD pairs, fast execution during volatile news, and easy funding/withdrawals. Prioritize platforms with solid risk tools (guaranteed stops, margin alerts) and dependable data feeds so balance-sheet headlines don’t become slippage. Below are the best Forex brokers to invest and trade on; pick the one that matches your platform preference and budget.

| Demo | Min. deposit, $ | Max. leverage | Deposit fee, % | Withdrawal fee, % | Regulation | TU overall score | Open an account | |

|---|---|---|---|---|---|---|---|---|

| Yes | 10 | 1:1000 | No | No | No | 7.89 | Go to broker Your capital is at risk.

|

|

| Yes | 100 | 1:300 | No | No | CySEC, FCA, ASIC, FMA, FSCA, FSA Seychelles, EFSA, MAS, DFSA, SCB | 7.52 | Go to broker 80% of retail CFD accounts lose money. |

|

| Yes | 50 | 1:50 | No | No | CFTC, NFA | 6.81 | Go to broker Your capital is at risk. |

|

| Yes | No | 1:200 | No | No | FSC (BVI), ASIC, IIROC, FCA, CFTC, NFA | 6.8 | Go to broker Your capital is at risk. |

|

| Yes | 100 | 1:50 | No | No | CIMA, FCA, FSA (Japan), NFA, IIROC, ASIC, CFTC | 6.74 | Study review |

Comparing central banks

The scale and scope of Fed actions were unusual relative to other major central banks. The ECB rolled out PEPP and enlarged CSPP – €1.85 trillion by end-2020 – but kept its remit tight, concentrating on euro-area sovereign and investment-grade private debt and avoiding speculative-grade paper or bond ETFs. The BoJ held to yield-curve control and modest equity-ETF buying, without open-ended interventions beyond Japan’s debt markets.

This contrast helps explain how the Fed differs from other central bank interventions: it combines broad asset-class coverage with global reach. Alongside domestic purchases, the Fed opened dollar swap lines (≈$450B) to 14 economies, reinforcing the market’s belief that it will step in to prevent systemic stress. In short, the Fed’s toolkit is larger, faster, and more diversified – shaped by the dollar’s reserve role and the Fed’s dual mandate – while the ECB stays inflation-and-bond focused and the BoJ centers on yen debt and disinflation.

Liquidity signals and asset risks

From 2020 to 2025, the Federal Reserve’s balance sheet didn’t just grow, it reshaped liquidity in ways most beginners miss. The total size grabs attention, but the real story is in the mix of assets. Large holdings of mortgage-backed securities during 2021–2022 created hidden leverage that affected credit for businesses beyond housing. Beginners who watch not just the total but the breakdown of assets can better understand how changes in the Fed’s portfolio impact bond yields, mortgage rates, and corporate borrowing costs.

Another key insight is that the Fed communicates policy through its balance-sheet actions, not just interest rates. For example, Fed repo market intervention – alongside changes in QE/QT – signals liquidity intent: when the Fed accelerates Treasury runoff, it tightens conditions before any official rate hike, creating ripple effects in the repo and money markets. Beginners who watch these moves can anticipate short-term USD liquidity swings and global market impacts. Paying attention to these signals offers a practical edge beyond surface-level numbers.

Conclusion

Understanding Fed intervention is essential for traders aiming to capitalize on currency market movements. Historical trends reveal that signals from the central bank, such as interest rate adjustments or forward guidance, often trigger significant reactions in correlated currency pairs like EUR/USD or USD/JPY. The key takeaway is that traders who interpret these signals early can position themselves advantageously before broader market shifts occur. In a landscape shaped by both predictability and uncertainty, mastering the reading of central bank cues stands as a powerful tool for smarter, more resilient trading decisions.

FAQs

How did the Fed's intervention during the COVID-19 crisis affect corporate borrowing and bond market conditions?

What role does forward guidance play in amplifying the effects of Fed intervention?

How does the Fed's approach to market intervention differ from that of other central banks?

What are some practical indicators traders can monitor to anticipate the impact of Fed market interventions?

Editors' Top Picks and Insights

Hunting crypto owners: Why criminals have gone offline

BitMEX is shutting down: Why Trump could not save the exchange

Do governments need crypto workers?

Brent nears $100: Why oil prices are rising

Gram Wallet launch: Can Telegram bring crypto to the masses?

AI without limits: How dangerous are neural networks?

Related Articles

Team that worked on the article

Andrey Mastykin is an experienced author, editor, and content strategist who has been with Traders Union since 2020. As an editor, he is meticulous about fact-checking and ensuring the accuracy of all information published on the Traders Union platform.

Dan Blystone began his trading career in 1998 as an arbitrage clerk on the floor of the Chicago Mercantile Exchange (CME). He later traded bond and Eurex futures at proprietary firms such as Altea Trading, gaining valuable experience in high-frequency trading and risk management.

Chinmay Soni is a financial analyst with more than 5 years of experience in working with stocks, Forex, derivatives, and other assets. As a founder of a boutique research firm and an active researcher, he covers various industries and fields, providing insights backed by statistical data.

Forex trading, short for foreign exchange trading, is the practice of buying and selling currencies in the global foreign exchange market with the aim of profiting from fluctuations in exchange rates. Traders speculate on whether one currency will rise or fall in value relative to another currency and make trading decisions accordingly. However, beware that trading carries risks, and you can lose your whole capital.

An investor is an individual, who invests money in an asset with the expectation that its value would appreciate in the future. The asset can be anything, including a bond, debenture, mutual fund, equity, gold, silver, exchange-traded funds (ETFs), and real-estate property.

Forex leverage is a tool enabling traders to control larger positions with a relatively small amount of capital, amplifying potential profits and losses based on the chosen leverage ratio.

Copy trading is an investing tactic where traders replicate the trading strategies of more experienced traders, automatically mirroring their trades in their own accounts to potentially achieve similar results.

Xetra is a German Stock Exchange trading system that the Frankfurt Stock Exchange operates. Deutsche Börse is the parent company of the Frankfurt Stock Exchange.

-

Afghanistan

Afghanistan

-

Albania

Albania

-

Algeria

Algeria

-

Angola

Angola

-

Argentina

Argentina

-

Armenia

Armenia

-

Australia

Australia

-

Austria

Austria

-

Azerbaijan

Azerbaijan

-

Bahamas

Bahamas

-

Bahrain

Bahrain

-

Bangladesh

Bangladesh

-

Belarus

Belarus

-

Belgium

Belgium

-

Bolivia

Bolivia

-

Botswana

Botswana

-

Brazil

Brazil

-

Brunei

Brunei

-

Bulgaria

Bulgaria

-

Cambodia

Cambodia

-

Cameroon

Cameroon

-

Canada

Canada

-

Chile

Chile

-

China

China

-

Colombia

Colombia

-

Congo

Congo

-

Costa Rica

Costa Rica

-

Cote d'Ivoire

Cote d'Ivoire

-

Croatia

Croatia

-

Cuba

Cuba

-

Cyprus

Cyprus

-

Czechia

Czechia

-

DR Congo

DR Congo

-

Denmark

Denmark

-

Dominican Republic

Dominican Republic

-

Ecuador

Ecuador

-

Egypt

Egypt

-

El Salvador

El Salvador

-

Estonia

Estonia

-

Eswatini

Eswatini

-

Ethiopia

Ethiopia

-

Finland

Finland

-

France

France

-

Georgia

Georgia

-

Germany

Germany

-

Ghana

Ghana

-

Greece

Greece

-

Haiti

Haiti

-

Hong Kong

Hong Kong

-

Hungary

Hungary

-

India

India

-

Indonesia

Indonesia

-

Iran, Islamic republic

Iran, Islamic republic

-

Iraq

Iraq

-

Ireland

Ireland

-

Israel

Israel

-

Italy

Italy

-

Jamaica

Jamaica

-

Japan

Japan

-

Jordan

Jordan

-

Kazakhstan

Kazakhstan

-

Kenya

Kenya

-

Korea

Korea

-

Kuwait

Kuwait

-

Kyrgyzstan

Kyrgyzstan

-

Laos

Laos

-

Latvia

Latvia

-

Lebanon

Lebanon

-

Lesotho

Lesotho

-

Libya

Libya

-

Lithuania

Lithuania

-

Luxembourg

Luxembourg

-

Madagascar

Madagascar

-

Malaysia

Malaysia

-

Malta

Malta

-

Mauritius

Mauritius

-

Mexico

Mexico

-

Moldova

Moldova

-

Mongolia

Mongolia

-

Montenegro

Montenegro

-

Morocco

Morocco

-

Mozambique

Mozambique

-

Myanmar

Myanmar

-

Namibia

Namibia

-

Nepal

Nepal

-

Netherlands

Netherlands

-

New Zealand

New Zealand

-

Nigeria

Nigeria

-

North Macedonia

North Macedonia

-

Norway

Norway

-

Oman

Oman

-

Pakistan

Pakistan

-

Palestine

Palestine

-

Panama

Panama

-

Papua New Guinea

Papua New Guinea

-

Paraguay

Paraguay

-

Peru

Peru

-

Philippines

Philippines

-

Poland

Poland

-

Portugal

Portugal

-

Puerto Rico

Puerto Rico

-

Qatar

Qatar

-

Reunion

Reunion

-

Romania

Romania

-

Rwanda

Rwanda

-

Saudi Arabia

Saudi Arabia

-

Serbia

Serbia

-

Singapore

Singapore

-

Slovakia

Slovakia

-

Slovenia

Slovenia

-

Somalia

Somalia

-

South Africa

South Africa

-

Spain

Spain

-

Sri Lanka

Sri Lanka

-

Sweden

Sweden

-

Switzerland

Switzerland

-

Syria

Syria

-

Taiwan

Taiwan

-

Tajikistan

Tajikistan

-

Tanzania

Tanzania

-

Thailand

Thailand

-

Trinidad and Tobago

Trinidad and Tobago

-

Tunisia

Tunisia

-

Turkey

Turkey

-

UAE

UAE

-

Uganda

Uganda

-

Ukraine

Ukraine

-

United Kingdom

United Kingdom

-

United States

-

Uruguay

Uruguay

-

Uzbekistan

Uzbekistan

-

Venezuela

Venezuela

-

Vietnam

Vietnam

-

Yemen

Yemen

-

Zambia

Zambia

-

Zimbabwe

Zimbabwe

- Forex

- Crypto