Stablecoins: Digital Dollars or the Future of Money? | TU Research

Editorial Note: While we adhere to strict Editorial Integrity, this post may contain references to products from our partners. Here's an explanation for How We Make Money. None of the data and information on this webpage constitutes investment advice according to our Disclaimer.

TU research suggests that stablecoins are rapidly evolving from a cryptocurrency trading tool into a broader financial instrument for savings and payments. In a survey of 1,500 cryptocurrency investors, 41% said they primarily use stablecoins to protect their savings from inflation, compared with 34% who use them mainly for trading. Meanwhile, 46% continue to store most of their stablecoins on centralized exchanges despite growing awareness of self-custody risks, and 38% trust stablecoins more than traditional banks for holding part of their savings. The research also found that 66% of respondents already use stablecoins for payments or international money transfers, while 54% believe they will become a mainstream financial tool within the next five years.

Stablecoins have evolved far beyond their original role as a tool for cryptocurrency trading. Once primarily used to move funds between exchanges without converting into fiat currencies, they are now becoming an important part of global digital finance.

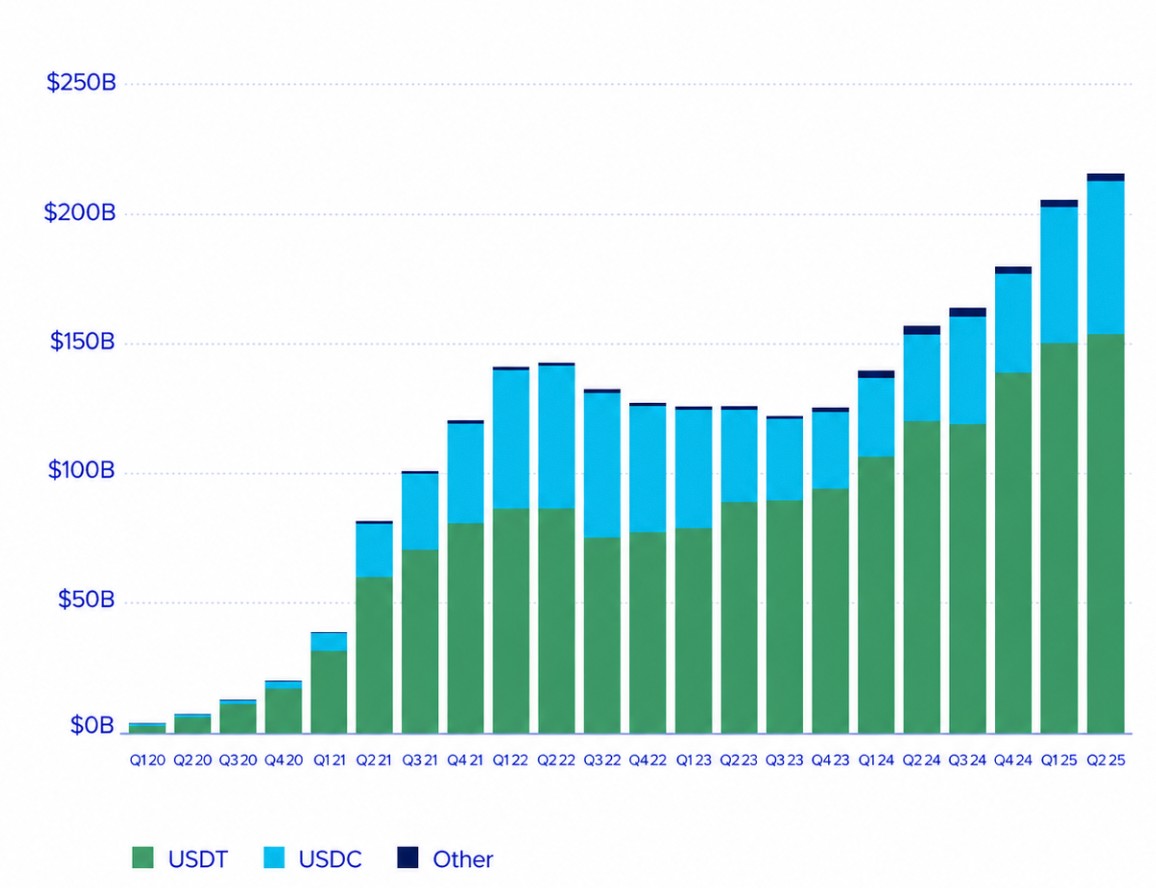

Today, payment companies, banks, fintech firms, and institutional investors increasingly view stablecoins as financial infrastructure for cross-border payments, settlement, treasury management, and tokenized assets. This shift is reflected in the rapid growth of the market, with stablecoin capitalization reaching record levels and adoption expanding well beyond the crypto ecosystem.

Institutional interest has accelerated alongside regulatory progress. Companies such as Visa, Circle, PayPal, and JPMorgan are actively developing stablecoin-based payment solutions, while governments continue to establish legal frameworks for digital dollar assets.

Despite this momentum, relatively little is known about how retail investors actually use stablecoins. Are they still primarily a trading tool, or have they become a preferred vehicle for savings and payments? Do users trust them more than traditional banks? And do retail adoption patterns align with institutional trends?

To answer these questions, TU conducted proprietary research examining how investors use stablecoins, how they store them, what risks they perceive, and whether they expect stablecoins to become a mainstream financial tool. The findings were compared with research published by Coinbase Institutional, Visa, Circle, Artemis, Castle Island Ventures, TRM Labs, and other leading organizations.

The research aims to answer six key questions:

How widely are stablecoins used for payments and international money transfers?

Do investors believe stablecoins will become a mainstream financial tool?

Findings

Based on TU research, several important patterns emerge regarding the evolving role of stablecoins in retail finance:

Inflation protection has become the primary reason for stablecoin adoption.41% of respondents said they primarily use stablecoins to preserve purchasing power, while 34% still use them mainly for cryptocurrency trading and portfolio management. This suggests that stablecoins are increasingly viewed as digital dollars rather than simply trading tools.

Centralized exchanges remain the preferred storage option. Nearly 46% of users keep most of their stablecoins on centralized exchanges, compared with 24% using non-custodial wallets and 18% storing assets in hardware wallets. Convenience continues to outweigh self-custody despite growing awareness of security risks.

Confidence in stablecoins is approaching confidence in traditional banks.38% of respondents trust stablecoins more than banks when holding part of their savings, while another 33% said their trust depends on the issuer and reserve transparency. Only 21% continue to prefer traditional banking institutions.

Stablecoins are already becoming an active payment instrument.66% of respondents reported using stablecoins for payments or international money transfers either frequently (29%) or occasionally (37%). This supports institutional research indicating that stablecoins are expanding beyond cryptocurrency trading into real-world financial transactions.

Regulatory uncertainty remains the biggest obstacle to wider adoption.36% of respondents identified future government regulation as their primary concern, ahead of potential de-pegging events (29%) and issuer solvency risks (25%). Investors appear more concerned about regulatory developments than technological vulnerabilities.

Retail investors expect stablecoins to become mainstream. More than half of respondents (54%) believe stablecoins will become a widely accepted financial tool within the next five years, while another 31% consider this outcome likely. Only 10% do not expect mainstream adoption, reflecting growing confidence in the long-term role of stablecoins within the global financial system.

Institutional validation

Stablecoins have moved from a crypto-native trading tool to a subject of direct interest for payment companies, asset managers, regulators, and macro-financial institutions. Institutional research increasingly treats stablecoins not only as part of the digital-asset market, but also as a potential payments, settlement, and treasury-management layer.

Coinbase Institutional reports that stablecoin interest among professional investors has accelerated sharply. In its 2025 Institutional Investor Digital Assets Survey, Coinbase found that 84% of institutions are either already using stablecoins or interested in using them, mainly for yield, transactional convenience, and foreign-exchange efficiency. This supports the view that stablecoins are becoming relevant beyond crypto trading desks and may increasingly serve treasury and payment functions.

Visa’s stablecoin research also supports this infrastructure thesis. Visa’s Onchain Analytics Dashboard, developed with Allium, tracks fiat-backed stablecoin activity across major blockchains and highlights that stablecoin transfers operate continuously, including weekends, unlike many traditional payment rails. Visa notes that stablecoins can enable near-continuous settlement 24/7/365, which is especially relevant for cross-border payments and global liquidity movement.

Circle, the issuer of USDC, positions stablecoins as a “software upgrade” to global finance. In its State of the USDC Economy report, Circle argues that stablecoins can make global commerce and finance faster, more open, and more internet-native. The company also reports that USDC circulation grew by more than 78% year over year, and that since launch Circle has bridged more than $850 billion between fiat and supported blockchains.

Artemis provides a more granular view of actual payment usage. Its stablecoin payments research shows that stablecoin payments increased from $6.0 billion in February to $10.2 billion in August, a 70% increase, and estimates that more than $136 billion in payments have been settled since 2023. This is important because it separates stablecoin use for payments from broader on-chain activity, much of which may still be related to trading, arbitrage, DeFi, or exchange flows.

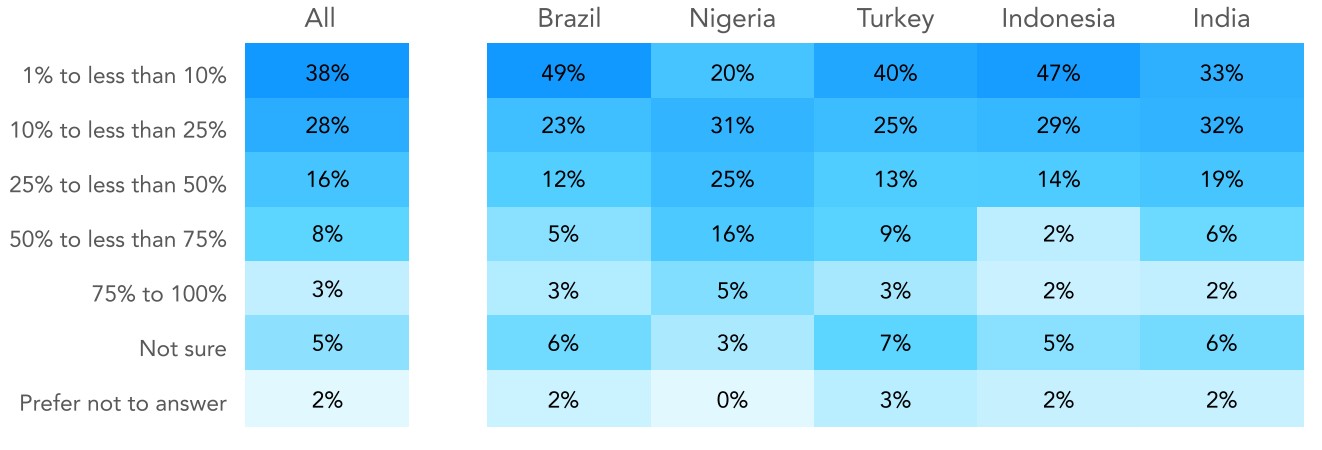

Research from Castle Island Ventures and Brevan Howard Digital, sponsored by Visa, highlights the importance of stablecoins in emerging markets. Their report found that while access to crypto remains the most common motivation for using stablecoins, non-crypto use cases are also significant: 47% of surveyed users cited access to dollars, 39% cited yield generation, and transactional purposes were also widely reported. This suggests that in countries with inflation, weak banking access, or capital controls, stablecoins may function less like speculative crypto assets and more like digital dollar accounts.

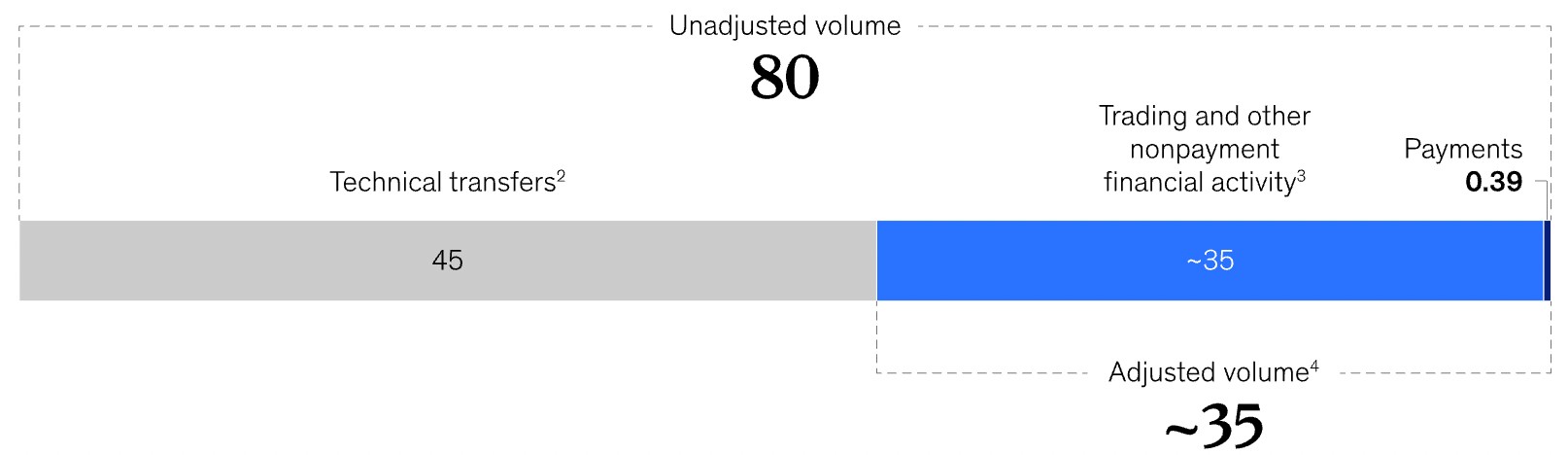

McKinsey takes a more cautious view of stablecoin payment data. Its analysis warns that headline transaction volumes can be misleading because much on-chain stablecoin activity is not tied to real-world payments. According to McKinsey, stablecoin volumes are often cited in trillions of dollars, but a substantial part of this activity reflects trading, liquidity management, exchange transfers, and other crypto-native use cases rather than consumer or business payments. This distinction is critical for interpreting stablecoin adoption realistically.

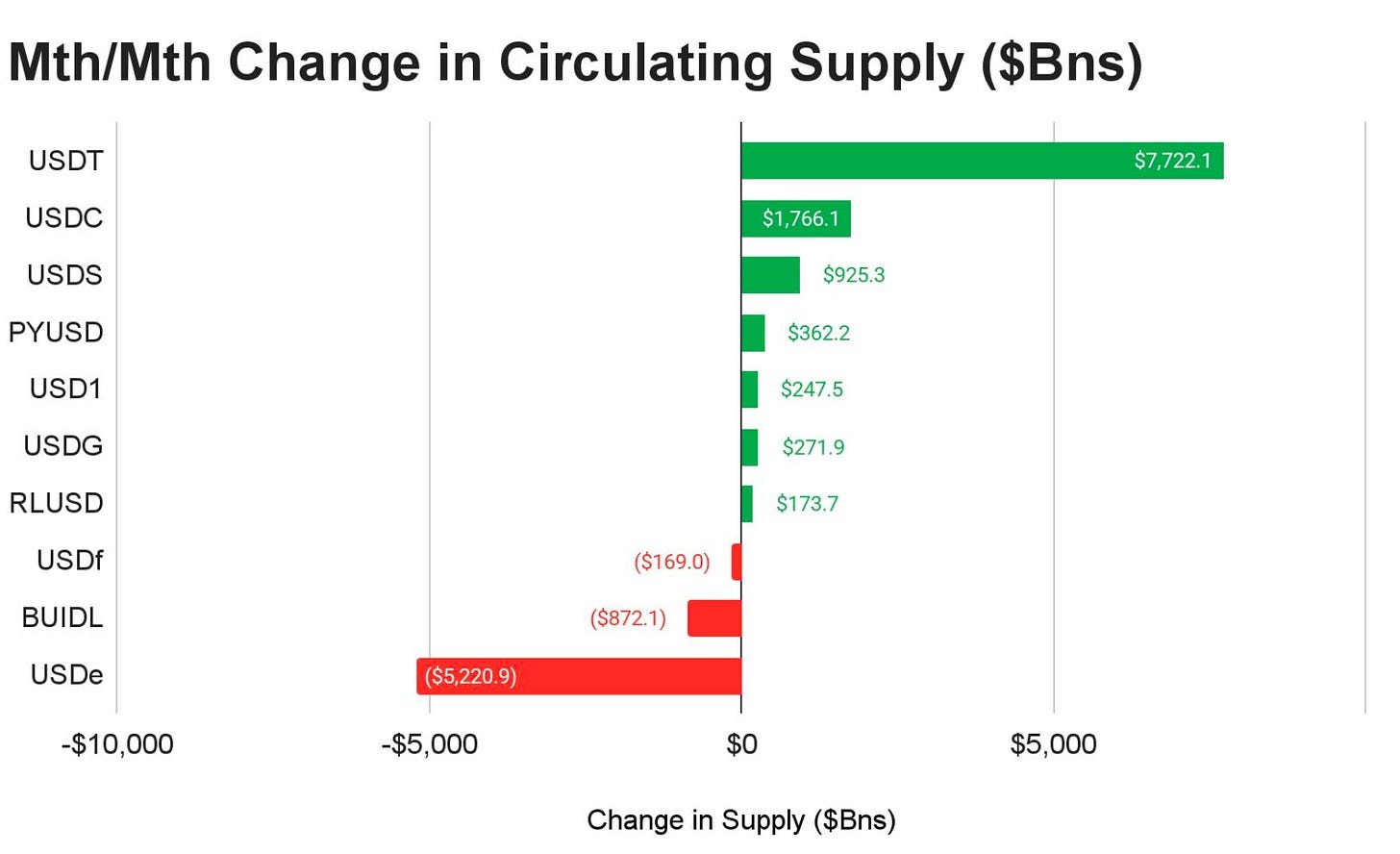

TRM Labs adds another important dimension: compliance and illicit finance. Its 2025 crypto adoption and stablecoin usage report states that stablecoins now account for 30% of all on-chain crypto transaction volume, with more than $4 trillion in volume recorded year-to-date by August 2025, an 83% increase compared with the same period in 2024. At the same time, TRM notes that illicit stablecoin activity remains a major regulatory concern, although sanctions-related activity in stablecoins declined by 60% between 2024 and 2025.

Traditional financial institutions and regulators remain divided. The IMF recognizes that stablecoins could support digital payments in areas where banking infrastructure is limited or expensive, but also emphasizes risks related to regulation, reserves, monetary sovereignty, and financial stability. Its 2025 paper notes that stablecoin issuance has doubled over the previous two years, driven mainly by crypto trading, while future demand may depend on legal clarity and broader payment use cases.

The Bank for International Settlements is more skeptical. BIS research argues that the rapid growth of stablecoins creates potential implications for monetary policy and financial stability, especially because large issuers hold significant short-term safe assets such as U.S. Treasury bills. This means stablecoins are no longer isolated from traditional finance: growth or stress in the stablecoin market may affect money markets, safe-asset demand, and broader financial conditions.

Taken together, institutional evidence suggests that stablecoins are entering a new phase. They remain deeply connected to crypto trading, but their role is expanding into payments, savings, cross-border transfers, treasury operations, and financial access in emerging markets. The key research question is no longer whether stablecoins have product-market fit, but whether retail users, institutions, and regulators are moving toward the same vision of stablecoins as a mainstream financial infrastructure layer.

Theoretical research

From an economic perspective, stablecoins combine characteristics of traditional money, payment infrastructure, and digital financial assets. Unlike highly volatile cryptocurrencies such as Bitcoin or Ethereum, fiat-backed stablecoins are designed to maintain a stable value, making them suitable for transactions, savings, and settlement rather than speculation alone.

One of the most relevant concepts associated with stablecoin adoption is currency substitution, commonly referred to as digital dollarization. In countries experiencing high inflation, capital controls, or volatile exchange rates, households and businesses often seek alternative stores of value. Historically this role has been fulfilled by foreign currencies, particularly the U.S. dollar. Stablecoins provide a digital version of dollarization, allowing users to access dollar-denominated assets without opening foreign bank accounts or relying on local financial institutions.

An important concept is the store of value behavior. Traditional financial theory defines a store of value as an asset capable of preserving purchasing power over time. Although stablecoins do not generate investment returns on their own, they may protect holders from rapid depreciation of local currencies. This characteristic explains why stablecoin adoption has accelerated in countries experiencing persistent inflation, foreign exchange restrictions, or banking instability.

Another relevant framework is payment infrastructure theory. Traditional international payments often involve multiple correspondent banks, settlement delays, and relatively high transaction costs. Stablecoins operating on public blockchains enable near-instant settlement without relying on legacy banking infrastructure. Visa has highlighted that blockchain-based settlement operates continuously, allowing transactions to be processed 24 hours a day, seven days a week, unlike conventional banking systems.

Finally, stablecoins illustrate the broader transition toward tokenized finance. Increasingly, financial institutions view them not merely as crypto assets but as programmable digital cash capable of supporting tokenized securities, decentralized finance, and global payment networks. As tokenization expands across capital markets, stablecoins may become the primary settlement asset connecting traditional finance with blockchain-based infrastructure.

Survey data

To better understand how retail investors actually use stablecoins, TU conducted a proprietary quantitative study examining user behavior, adoption patterns, trust, storage preferences, payment activity, and risk perception.

Unlike institutional reports, which primarily focus on infrastructure development and market trends, this research explores how individual investors use stablecoins in practice and whether their behavior aligns with the direction of institutional adoption.

Methodology

The study was conducted using a structured online survey based on the CAWI (Computer-Assisted Web Interviewing) methodology.

Sample composition: 1,500 cryptocurrency investors.

Coverage: North America, Europe, Asia, Latin America, Africa, and emerging markets.

Age: 18–60 years old.

Participation criteria: respondents who had used at least one fiat-backed stablecoin (USDT, USDC, DAI, FDUSD, USDe, or similar) during the previous 24 months.

Statistical confidence: 95%.

Estimated sampling deviation: ±2.5%.

Research team

The study was conducted by the analytical team at Traders Union:

Anastasiia Chabaniuk (Author, TU Research) – research design and interpretation.

Chinmay Soni (Fact-checker) – data validation and statistical verification.

Dan Blystone (Editor-in-Chief) – editorial and methodological supervision.

TU Research Team (Andrey Mastykin, Oleg Tkachenko) – data collection and analysis.

Why do investors use stablecoins?

Stablecoins were initially introduced as a tool for cryptocurrency trading, allowing users to move funds between exchanges without converting assets into fiat currencies. However, their role has expanded considerably over the past few years. Today, stablecoins are increasingly used for savings, cross-border payments, decentralized finance, and everyday financial transactions.

To better understand what motivates adoption today, respondents were asked about the primary reason they use stablecoins.

| Reason | Share of users |

|---|---|

| Protect savings from inflation | 41% |

| Crypto trading and portfolio management | 34% |

| International money transfers | 27% |

| DeFi and earning yield | 19% |

| Online payments | 15% |

| Payroll or business settlements | 7% |

Insight: Preserving purchasing power has become the leading use case for stablecoins, surpassing cryptocurrency trading. This suggests that many users increasingly view stablecoins as digital dollars rather than purely trading instruments.

Where do users keep their stablecoins?

Choosing where to store stablecoins is one of the most important security decisions for cryptocurrency investors. While self-custody offers greater control over digital assets, centralized exchanges continue to provide convenience, liquidity, and easy access to trading services.

To better understand current storage preferences, respondents were asked where they keep most of their stablecoin holdings.

Where users store stablecoins:

Centralized exchanges – 46%.

Mobile non-custodial wallets – 24%.

Hardware wallets – 18%.

DeFi protocols – 8%.

Custodial banking or fintech services – 4%.

Insight: Despite growing awareness of self-custody, centralized exchanges remain the dominant storage solution, indicating that convenience continues to outweigh security considerations for many retail investors.

Do investors trust stablecoins more than traditional banks?

Trust plays a central role in financial decision-making. In regions experiencing high inflation, currency depreciation, or banking instability, stablecoins may increasingly compete with traditional financial institutions as a preferred store of value.

To evaluate investor sentiment, respondents were asked whether they trust stablecoins more than banks for holding part of their savings.

| Response | Share of users |

|---|---|

| Yes | 38% |

| Depends on the issuer | 33% |

| No | 21% |

| Unsure | 8% |

Insight: More than one-third of respondents already place greater trust in stablecoins than in traditional banks, while another third believe trust depends largely on the issuer and reserve transparency.

How are stablecoins used for payments?

Although stablecoins were originally developed for crypto markets, payment companies increasingly position them as infrastructure for cross-border transactions and digital commerce.

Respondents were asked how frequently they use stablecoins for payments or money transfers.

Stablecoin payment activity:

Frequently – 29%.

Occasionally – 37%.

Rarely – 22%.

Never – 12%.

Insight: Nearly two-thirds of respondents have already used stablecoins for payments or transfers, supporting the growing institutional narrative that stablecoins are evolving into a global payment network.

What concerns investors the most?

Despite rapid adoption, stablecoins continue to face regulatory, technological, and issuer-related risks. Understanding these concerns helps explain what may slow broader adoption.

Respondents were asked to identify the greatest risk associated with holding stablecoins.

| Concern | Share of users |

|---|---|

| Government regulation | 36% |

| Loss of peg | 29% |

| Issuer insolvency or insufficient reserves | 25% |

| Exchange hacks or custody risks | 18% |

| Smart contract vulnerabilities | 11% |

| I have no major concerns | 9% |

Insight: Regulatory uncertainty remains the largest concern among retail investors, while confidence in reserve backing and price stability also plays a major role in adoption decisions.

Will stablecoins become mainstream money?

Institutional adoption has accelerated rapidly, but retail investors ultimately determine whether stablecoins become part of everyday financial life.

Respondents were asked whether they believe stablecoins will become a widely accepted payment method within the next five years.

Will stablecoins become mainstream:

Yes – 54%.

Possibly – 31%.

No – 10%.

Unsure – 5%.

Insight: Most respondents expect stablecoins to become a mainstream financial tool over the coming years, reflecting growing confidence in their long-term role beyond cryptocurrency markets.

PDF version of the TU research

Download the full PDF version of the TU research to access additional analysis, detailed survey data, and extended findings from our analytical team. The report includes complete methodology, charts, and behavioral insights referenced throughout the study.

Practical implications for investors

The findings suggest that stablecoins are rapidly evolving from a cryptocurrency trading tool into a broader financial instrument used for savings, payments, and international transfers. However, adoption also introduces new risks that investors should carefully evaluate.

Several practical conclusions emerge from the research:

Stablecoins should no longer be viewed solely as an instrument for moving funds between crypto exchanges. They are increasingly used as digital dollars for savings, payments, and treasury management.

Choosing the right issuer is becoming as important as choosing the right bank. Investors should evaluate reserve transparency, regulatory oversight, redemption mechanisms, and audit reports before holding significant balances.

Diversifying across multiple stablecoin issuers may help reduce counterparty risk. Concentrating all funds in a single issuer exposes investors to operational, regulatory, or liquidity risks.

Self-custody offers greater control over digital assets but requires strong security practices. Investors holding significant amounts of stablecoins should consider hardware wallets and secure backup procedures instead of relying exclusively on centralized exchanges.

Stablecoins can significantly reduce the cost and settlement time of international payments compared with traditional banking services, particularly in regions with limited access to U.S. dollars or expensive remittance infrastructure.

Regulatory developments are likely to become one of the main drivers of future adoption. Clear legal frameworks could increase institutional participation, while restrictive policies may influence issuer availability across different jurisdictions.

Stablecoins are increasingly becoming part of personal financial planning. Many users now treat them as a digital cash allocation within a diversified portfolio rather than as speculative cryptocurrency exposure.

Investors should remember that price stability does not eliminate investment risk. Counterparty risk, reserve management, regulatory intervention, and custody security remain critical considerations.

The findings also suggest that the choice of platform plays an increasingly important role in the overall stablecoin experience. While the stablecoin itself determines price stability and issuer-related risks, the platform influences accessibility, transaction costs, available networks, custody options, and additional services such as staking, lending, and fiat on- and off-ramps.

For retail investors, factors including supported stablecoins, withdrawal fees, regulatory compliance, proof of reserves, wallet infrastructure, and payment integrations can significantly affect both security and convenience. Institutional users may additionally prioritize liquidity, settlement capabilities, and treasury management tools.

As stablecoins continue to expand beyond cryptocurrency trading into payments and digital cash management, selecting a reliable platform becomes just as important as choosing the right stablecoin. The following comparison highlights leading cryptocurrency exchanges that provide broad stablecoin support and services for retail investors.

| Coinbase | OKX | Crypto.com | Kraken | Cryptohopper | |

|---|---|---|---|---|---|

|

Demo account |

No | Yes | No | No | No |

|

Min. Deposit, $ |

10 | 10 | 1 | 10 | No |

|

Coins Supported |

249 | 329 | 250 | 278 | 1000 |

|

Spot Taker fee, % |

0.5 | 0.1 | 0.5 | 0.4 | 0 |

|

Spot Maker Fee, % |

0.5 | 0.08 | 0.25 | 0.25 | 0 |

|

Alerts |

Yes | Yes | Yes | Yes | Yes |

|

Copy trading |

No | Yes | No | Yes | Yes |

|

TU overall score |

8.6 | 8.48 | 8.44 | 8.32 | 7.85 |

|

Open an account |

Go to broker Your capital is at risk. |

Go to broker Your capital is at risk. |

Go to broker Your capital is at risk. |

Go to broker Your capital is at risk. |

Go to broker Your capital is at risk. |

Data sources and methodology references

Coinbase Institutional. 2025 Institutional Investor Digital Assets Survey.

EY-Parthenon & Coinbase. Institutional Investor Digital Assets Survey.

Visa & Allium. Visa Onchain Analytics Dashboard.

Circle. State of the USDC Economy 2025.

Artemis. Stablecoin Update: October 2025.

Castle Island Ventures, Brevan Howard Digital & Visa. Stablecoins: The Emerging Market Story.

TRM Labs. Crypto Adoption and Stablecoin Usage Report.

McKinsey & Company. Stablecoins in Payments: What the Raw Transaction Numbers Miss.

International Monetary Fund (IMF). Understanding Stablecoins.

International Monetary Fund (IMF). Decrypting Crypto: How to Estimate International Stablecoin Flows.

Bank for International Settlements (BIS). Stablecoins and Safe Asset Holdings.

Previous volumes in this series

Conclusion

Stablecoins are rapidly transitioning from niche trading instruments to powerful digital financial tools reshaping savings, payments, and cross-border transfers. TU’s research highlights that both retail and institutional users increasingly view stablecoins as a reliable store of value—especially for inflation protection and efficient international transactions. While regulatory uncertainty remains the primary hurdle to broader adoption, widespread trust in stablecoins and their integration by major payment firms like Visa and Circle underscore their mainstream potential. Investors should recognize that stablecoins are becoming digital dollars in practice, signaling a fundamental shift in how money moves globally. As stablecoins continue to bridge traditional finance and blockchain technology, they stand poised to redefine what we consider modern money.

FAQs

What are the main differences between using stablecoins and traditional banking for everyday transactions?

How do storage options for stablecoins affect security and accessibility for users?

In what ways do regulatory developments influence stablecoin adoption and usage?

Why are stablecoins considered an important tool in regions affected by inflation or limited banking access?

Editors' Top Picks and Insights

Hunting crypto owners: Why criminals have gone offline

BitMEX is shutting down: Why Trump could not save the exchange

Do governments need crypto workers?

Brent nears $100: Why oil prices are rising

Gram Wallet launch: Can Telegram bring crypto to the masses?

AI without limits: How dangerous are neural networks?

Related Articles

Team that worked on the article

Anastasiia has 17 years of experience in finance and content marketing. She believes that the support of information and expert opinion is very important for the success of investors and new traders.

Dan Blystone began his trading career in 1998 as an arbitrage clerk on the floor of the Chicago Mercantile Exchange (CME). He later traded bond and Eurex futures at proprietary firms such as Altea Trading, gaining valuable experience in high-frequency trading and risk management.

Chinmay Soni is a financial analyst with more than 5 years of experience in working with stocks, Forex, derivatives, and other assets. As a founder of a boutique research firm and an active researcher, he covers various industries and fields, providing insights backed by statistical data.

-

Afghanistan

Afghanistan

-

Albania

Albania

-

Algeria

Algeria

-

Angola

Angola

-

Argentina

Argentina

-

Armenia

Armenia

-

Australia

Australia

-

Austria

Austria

-

Azerbaijan

Azerbaijan

-

Bahamas

Bahamas

-

Bahrain

Bahrain

-

Bangladesh

Bangladesh

-

Belarus

Belarus

-

Belgium

Belgium

-

Bolivia

Bolivia

-

Botswana

Botswana

-

Brazil

Brazil

-

Brunei

Brunei

-

Bulgaria

Bulgaria

-

Cambodia

Cambodia

-

Cameroon

Cameroon

-

Canada

Canada

-

Chile

Chile

-

China

China

-

Colombia

Colombia

-

Congo

Congo

-

Costa Rica

Costa Rica

-

Cote d'Ivoire

Cote d'Ivoire

-

Croatia

Croatia

-

Cuba

Cuba

-

Cyprus

Cyprus

-

Czechia

Czechia

-

DR Congo

DR Congo

-

Denmark

Denmark

-

Dominican Republic

Dominican Republic

-

Ecuador

Ecuador

-

Egypt

Egypt

-

El Salvador

El Salvador

-

Estonia

Estonia

-

Eswatini

Eswatini

-

Ethiopia

Ethiopia

-

Finland

Finland

-

France

France

-

Georgia

Georgia

-

Germany

Germany

-

Ghana

Ghana

-

Greece

Greece

-

Haiti

Haiti

-

Hong Kong

Hong Kong

-

Hungary

Hungary

-

India

India

-

Indonesia

Indonesia

-

Iran, Islamic republic

Iran, Islamic republic

-

Iraq

Iraq

-

Ireland

Ireland

-

Israel

Israel

-

Italy

Italy

-

Jamaica

Jamaica

-

Japan

Japan

-

Jordan

Jordan

-

Kazakhstan

Kazakhstan

-

Kenya

Kenya

-

Korea

Korea

-

Kuwait

Kuwait

-

Kyrgyzstan

Kyrgyzstan

-

Laos

Laos

-

Latvia

Latvia

-

Lebanon

Lebanon

-

Lesotho

Lesotho

-

Libya

Libya

-

Lithuania

Lithuania

-

Luxembourg

Luxembourg

-

Madagascar

Madagascar

-

Malaysia

Malaysia

-

Malta

Malta

-

Mauritius

Mauritius

-

Mexico

Mexico

-

Moldova

Moldova

-

Mongolia

Mongolia

-

Montenegro

Montenegro

-

Morocco

Morocco

-

Mozambique

Mozambique

-

Myanmar

Myanmar

-

Namibia

Namibia

-

Nepal

Nepal

-

Netherlands

Netherlands

-

New Zealand

New Zealand

-

Nigeria

Nigeria

-

North Macedonia

North Macedonia

-

Norway

Norway

-

Oman

Oman

-

Pakistan

Pakistan

-

Palestine

Palestine

-

Panama

Panama

-

Papua New Guinea

Papua New Guinea

-

Paraguay

Paraguay

-

Peru

Peru

-

Philippines

Philippines

-

Poland

Poland

-

Portugal

Portugal

-

Puerto Rico

Puerto Rico

-

Qatar

Qatar

-

Reunion

Reunion

-

Romania

Romania

-

Rwanda

Rwanda

-

Saudi Arabia

Saudi Arabia

-

Serbia

Serbia

-

Singapore

Singapore

-

Slovakia

Slovakia

-

Slovenia

Slovenia

-

Somalia

Somalia

-

South Africa

South Africa

-

Spain

Spain

-

Sri Lanka

Sri Lanka

-

Sweden

Sweden

-

Switzerland

Switzerland

-

Syria

Syria

-

Taiwan

Taiwan

-

Tajikistan

Tajikistan

-

Tanzania

Tanzania

-

Thailand

Thailand

-

Trinidad and Tobago

Trinidad and Tobago

-

Tunisia

Tunisia

-

Turkey

Turkey

-

UAE

UAE

-

Uganda

Uganda

-

Ukraine

Ukraine

-

United Kingdom

United Kingdom

-

United States

-

Uruguay

Uruguay

-

Uzbekistan

Uzbekistan

-

Venezuela

Venezuela

-

Vietnam

Vietnam

-

Yemen

Yemen

-

Zambia

Zambia

-

Zimbabwe

Zimbabwe

- Forex

- Crypto