Is Meta Undervalued Or Overvalued After Market Crash?

Editorial Note: While we adhere to strict Editorial Integrity, this post may contain references to products from our partners. Here's an explanation for How We Make Money. None of the data and information on this webpage constitutes investment advice according to our Disclaimer.

Meta’s stock is now trading in a clear downtrend after breaking below its key moving averages. While the ad business remains strong, recent selling shows that investors are less willing to pay for long term bets like the metaverse when price action weakens. If margins slip or spending stays high, the market could pressure the stock further, which matters for anyone assessing how much Meta is worth today.

Meta’s current stock price depends on how much confidence investors place in parts of the business that still earn very little. The core apps continue to drive profits, but the market is also valuing future results from the metaverse and AI. These areas are at an early stage, which creates a gap between expectations and real performance. When that gap widens, even small disappointments can pressure the stock. This becomes important when reviewing Meta’s valuation today.

Understanding Meta

Meta has recovered sharply from its 2022 lows after lowering costs, improving ad performance and expanding AI tools across its apps. This rebound has pushed the stock higher and brought renewed attention to how the market is valuing Meta today.

Meta’s shift toward core advertising and AI has helped restore profitability and lift its market cap above the one trillion dollar mark. The company now posts some of the strongest margins in large tech, but rising regulatory pressure and tougher competition from TikTok and YouTube have raised questions about how long this strength can last.

This article reviews Meta’s financial performance, market behavior and analyst views to help you understand whether Meta’s valuation reflects current results or expectations that may be hard to maintain.

Meta's current market position

Meta has climbed back to the top tier of global tech companies after a major recovery from its post-2021 lows. Its core apps still dominate social media, and new investments in AI and virtual reality are shaping its long term plans. Before judging Meta’s valuation, it helps to see how the business is currently positioned.

Overview of Meta Platforms Inc. and its subsidiaries

Meta is more than just Facebook. It is a multi-product digital empire built around user data, advertising, and communication tools used by billions every day.

Core business areas:

Family of apps. This includes Facebook, Instagram, WhatsApp, and Messenger, platforms used by over 3.8 billion people monthly. This division generates nearly all of Meta’s profits through ad revenue.

Reality Labs. The company’s virtual reality and metaverse division includes the Quest headset and AR initiatives. While it is still in the investment phase, this segment represents Meta’s long-term tech bet.

AI infrastructure. Meta has shifted major internal resources toward building and integrating generative AI across its apps and advertising tools.

Most of Meta’s revenue still comes from digital ads, but the company is preparing for changes in how people use online platforms. Its structure allows it to shift resources quickly, which helps with long term planning across different parts of the business.

Recent stock performance and market capitalization

Meta’s stock has been one of the best performers in the S&P 500 since early 2023. A renewed focus on profitability, combined with excitement over AI tools and efficiency gains, has pushed the stock to new highs.

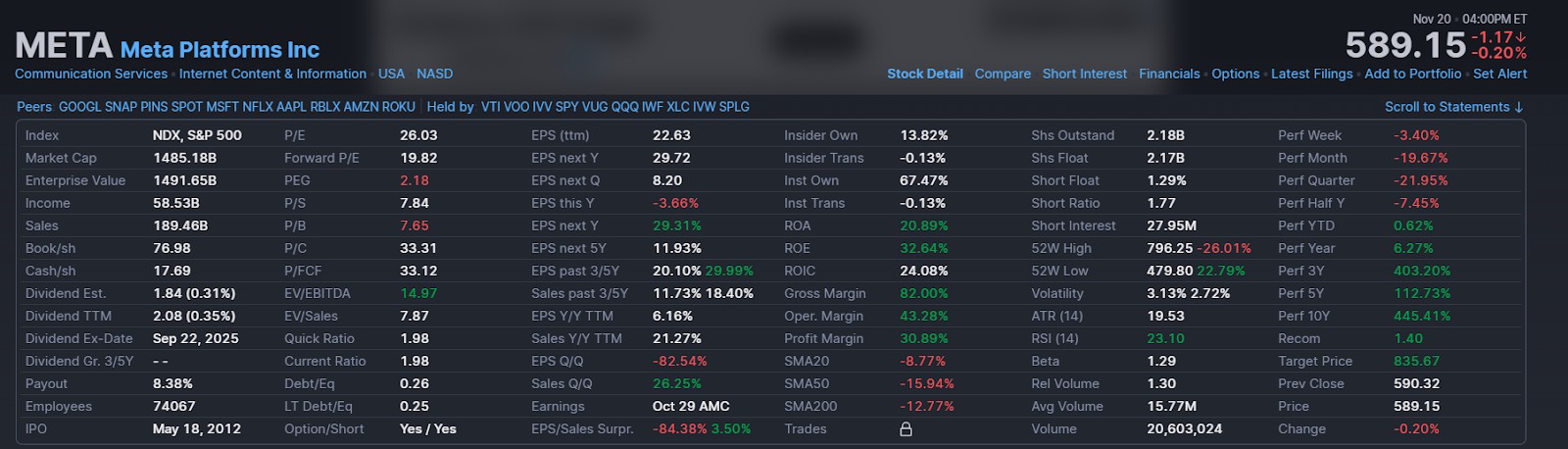

Meta now trades with a market cap of about $1.48 trillion, supported by strong revenue and high margins. The forward P/E is near 19.8x, which is lower than many large tech names even after the recent price drop. Over the past year, the stock is up roughly 6%, but most gains were earlier in the year before the current decline.

Meta continues to benefit from strong operating performance, with an operating margin near 43% and a profit margin above 30%. The company remains active with buybacks, lifting per share earnings, and new AI tools are helping advertisers improve results. These trends support investor interest even as the stock loses momentum.

The market still sees Meta as a mix of value and growth, but the recent drop shows that expectations may be adjusting. With the stock breaking below key levels, investors are watching how Meta’s valuation holds up if results or guidance soften.

Valuation of Meta

Meta’s stock has surged in recent quarters, but is it still fairly priced? To answer that, we look at the company’s core financials, what it's truly worth based on long-term projections, and how its stock is behaving in the market. This three-part view helps investors decide if Meta is valued right or running ahead of its fundamentals.

Fundamental analysis of Meta

For investors trying to figure out if Meta is overvalued, a closer look at key valuation ratios and financial health indicators can help. These metrics reveal how the stock is priced compared to its earnings, how much growth is priced in, and how efficiently the company is generating profit and cash.

Price to earnings (P/E) ratio

Meta now trades at a trailing P/E of about 26, with a forward P/E near 19.8. This places it below many large tech peers that trade at higher multiples. The current levels are also well below the peaks Meta reached during its 2021 rally.

The present P/E shows that the market still views Meta as a profitable and established business. The valuation is not cheap, but it remains reasonable for a company with steady earnings and a large customer base.

This P/E level is supported by Meta’s solid profits and healthy cash flow, and it continues to shape how investors judge Meta’s valuation in the current market.

Price to earnings growth (PEG) ratio

Meta’s PEG stands near 2.18, supported by earnings growth estimates of about 29% for next year and close to 12% over the next five years. A PEG near one is usually seen as fair. A higher PEG shows that the stock trades at a premium to its expected earnings pace.

This PEG level suggests that the market expects Meta to keep posting strong earnings gains, especially next year. It is not low, but it could be supported if margins remain high and spending stays controlled.

If earnings growth falls below these estimates, the higher PEG could become harder to justify, which may affect how investors view Meta’s valuation in the coming quarters.

Operating margins and free cash flow

Beyond valuation ratios, operational efficiency and free cash flow show how well Meta is converting revenue into profits and long-term value. Meta’s operating margin now stands near 43%, which is one of the highest levels in large tech. Profit margin remains strong at about 31%, reflecting solid ad performance and tighter cost control. Free cash flow is close to $48 billion, giving the company steady support for buybacks and long term investment.

Strong margins and steady cash flow allow Meta to fund growth, buy back shares and invest in AI and infrastructure without taking on pressure from debt. This financial position helps the company stay flexible as markets and user trends shift.

Meta’s leaner cost base and efficient cash use have strengthened its financial foundation. This helps support how investors look at Meta’s valuation, even if revenue or earnings growth cools in the short term.

Meta intrinsic valuation

To see what Meta is really worth, discounted cash flow (DCF) models help estimate its fair value based on future profits. These models strip away hype and focus on fundamentals.

Most updated DCF models, using revenue growth near 8 to 10% and margins in the mid-30% range, place Meta’s fair value between $480 and $520 per share. With the stock trading near $589, the price now sits above many fair value estimates, supported by strong cash flow and optimism around AI and future monetization.

Meta trades at a forward P/E of about 19.8, which keeps it below many large tech names. The EV to EBITDA ratio is close to 14, placing Meta above Alphabet but still below Microsoft on this measure.

Meta does not appear extremely overvalued, but its price assumes that revenue and earnings growth will stay solid. Any slowdown in ad spending or user trends could shift how the market views Meta’s valuation.

Meta technical analysis

Technical signals can help short-term traders understand momentum and entry points. Meta’s chart has shown consistent strength but may be approaching a breather.

Meta is now trading well below the 200-day EMA near $672, which confirms a strong downtrend. The RSI is near 23, placing the stock in oversold territory. Nearby support sits around the $560 to $575 range, while resistance has formed near $615 to $630.Momentum is still tilted to the downside, and the chart suggests the stock may test deeper support if selling continues. Long term investors may wait for signs of stabilizing price action before reassessing Meta’s valuation at current levels.

Analyst perspectives and market sentiment

Analysts are split on Meta after its sharp pullback. Some view the drop as a reset after strong gains earlier in the year, while others see it as the start of a tougher period. Market sentiment has turned more cautious as the stock trades below major support levels.

Bullish viewpoints

Supporters of Meta’s strategy believe the company is finally hitting its stride. After cutting costs, improving margins, and leaning into AI, they see more upside ahead.

Why some analysts are optimistic:

Improved profitability. Analysts at JPMorgan and Jefferies note that Meta’s return to operating margins above 35% is a major driver behind renewed investor confidence.

AI integration at scale. Meta is rolling out AI tools across Facebook, Instagram, and ad platforms, a move analysts believe will lift both engagement and monetization.

User base remains unmatched. With over 3.8 billion monthly users across its apps, Meta’s reach is a major competitive edge that supports future ad revenue growth.

Strong balance sheet. Meta’s cash position and aggressive buybacks give it both financial stability and the ability to boost per-share earnings.

Meta is delivering on both growth and efficiency, making it one of the most attractive tech plays heading into the next cycle. Analysts expect continued margin expansion, even without major user growth

Bearish viewpoints

Skeptics argue that while Meta has recovered, much of the good news is already priced in, and the risks are building.

Concerns raised by analysts:

Ad revenue risks. Some analysts point out that Meta’s business still relies heavily on ad spending, which could take a hit if the economy slows.

Regulatory pressures. Meta faces antitrust scrutiny in the U.S. and privacy rules in the EU, which could limit data use or increase compliance costs.

Overdependence on AI narrative. Critics say the stock’s rally is fueled more by AI enthusiasm than by actual revenue contribution from those tools, at least for now.

Valuation running hot. With the stock up nearly 70% over the last year, some fear that future gains may be limited unless Meta consistently beats expectations.

Meta is in a better place operationally, but the stock may already reflect most of that improvement. Any miss on earnings or regulatory shock could trigger a pullback.

We also suggest reading our analysts’ forecast:

| Year | Price in the middle of the year | Price at the end of the year |

|---|---|---|

| 2026 | $560 | $640 |

| 2027 | $880 | $850 |

| 2028 | $1100 | $1100 |

| 2029 | $1200 | $1300 |

| 2030 | $1900 | $2000 |

| 2031 | $1400 | $1500 |

| 2032 | $2100 | $2200 |

| 2033 | $2800 | $2700 |

| 2034 | $3500 | $3400 |

| 2035 | $1200 | $1300 |

| 2036 | $1800 | $2600 |

| 2037 | $3000 | $3800 |

| 2038 | $3400 | $2900 |

| 2039 | $4100 | $4400 |

| 2040 | $6100 | $5800 |

Consensus and price targets

Most analysts remain positive on Meta’s long term outlook, although the tone has cooled after the recent drop. The company is still viewed as financially strong, but the market is now more focused on how it performs quarter by quarter.

Current analyst estimates place the average price target around $630, compared to the stock trading near $589. About 78% of analysts rate Meta as a buy, around 19% suggest holding, and only a few maintain a sell rating. High end targets reach $720, reflecting confidence in long term AI monetization and continued efficiency gains. On the lower end, some analysts see fair value near $520, especially if revenue growth slows or spending in Reality Labs remains elevated.

For investors, the data shows that analysts still expect moderate upside, but the margin for error is smaller now. The company’s strong financial base provides support, yet sustaining these expectations depends on consistent earnings and clear progress across its AI and advertising strategy. These factors play an important role in how the market approaches Meta’s valuation today.

After understanding the valuation picture, investors often want a straightforward place to begin. That is where the list of best stock brokers for investing in stocks becomes useful, giving you an easy way to find a dependable platform for buying and managing your positions.

| eToro USA | Plus500 | eOption | Revolut | Interactive Brokers | |

|---|---|---|---|---|---|

|

Account min. |

50 | EUR500 | No | No | No |

|

Research and data |

Yes | Yes | Yes | Yes | Yes |

|

Basic stock/ETF fee |

No | $0.006 | $0 | 0.12%-0.25% | 0-0,0035% |

|

Deposit Fee |

No | No | Not specified | No | No |

|

Withdrawal fee |

No | No | Not specified | No charge up to a limit | No |

|

Regulation |

SEC, FINRA | CySEC, FCA, ASIC, FMA, FSCA, FSA Seychelles, EFSA, MAS, DFSA, SCB | FINRA, SIPC | FCA, SEC, FINRA | SEC, FINRA, SIPC, FCA, NSE, BSE, SEBI, SEHK, HKFE, IIROC, ASIC, CFTC, NFA |

|

TU overall score |

8.8 | 8.48 | 7.93 | 8.6 | 8.53 |

|

Open an account |

Go to broker Your capital is at risk. |

Go to broker 80% of retail CFD accounts lose money. |

Study review | Study review | Study review |

Meta Platforms News and Technology Updates

Wall Street rotation lifts cyber and Meta shares as chip stocks retreat

Oversold conditions may limit further declines for Meta stock, slowing the drop

-3.8% for Meta stock as buyers hesitate near $629.75 resistance

U.S. markets brace for jobs data, trade uncertainty and AI moves before Thursday open

U.S. stocks brace for payrolls data and Trump CNBC interview

U.S. markets pause at start of third quarter as crude falls and tech momentum cools

Why Meta’s future vision could weigh down today’s stock

From what I have seen following Meta for years, the pressure on this stock comes from the gap between what the business earns today and what investors expect it to become. The ad engine is working well, but the share price leans heavily on the hope that AI and the metaverse turn into real revenue drivers sooner rather than later. When a company trades on future wins that have not shown scale yet, even small delays can shake confidence fast.

I also pay close attention to how often Meta adjusts its products to keep up with rivals. A company that once set the tone is now working harder to maintain attention, and that shift matters when growth is slowing. None of this makes Meta weak, but it does mean the stock carries expectations that require steady proof every quarter. For anyone investing now, the real question is whether you trust Meta to deliver meaningful gains from both its core platforms and its long term tech bets at the same time. That is where the real weight on the valuation sits.

Conclusion

Meta’s recent decline below key moving averages has undeniably reset investor expectations, but the company's core business remains robust. Despite short-term volatility, Meta continues to command an immense user base and steady advertising revenue, evidence that foundational strengths are intact. While the stock may no longer possess the high-growth allure it once had, its current valuation offers a compelling entry point for long-term investors willing to weather further fluctuations. Ultimately, patient investors who look past the noise may find that the market’s skepticism is short-sighted—and that Meta’s value, though tested, is far from diminished.

FAQs

How does Meta’s reliance on advertising revenue affect its valuation risk?

In what ways do Meta’s AI and metaverse initiatives contribute to its stock valuation?

How do regulatory and competitive pressures impact Meta’s valuation outlook?

What financial metrics indicate whether Meta is fairly valued compared to peers?

Editors' Top Picks and Insights

Three trends that could reshape the crypto market over the next decade

Trump financial disclosure: How the president's crypto income became a U.S. ethics issue

Code red: What's behind Bitcoin’s sharp selloff?

MiCA is live: How EU new rules are changing crypto market

Bitcoin price prediction based on MVRV: Indicator points to BTC undervaluation

Amazon flooded with AI books: Crisis of trust in literature market

Related Articles

Team that worked on the article

Ashutosh Sureka is a finance professional specializing in financial research, credit assessment, and equity analysis.

Dan Blystone began his trading career in 1998 as an arbitrage clerk on the floor of the Chicago Mercantile Exchange (CME). He later traded bond and Eurex futures at proprietary firms such as Altea Trading, gaining valuable experience in high-frequency trading and risk management.

Chinmay Soni is a financial analyst with more than 5 years of experience in working with stocks, Forex, derivatives, and other assets. As a founder of a boutique research firm and an active researcher, he covers various industries and fields, providing insights backed by statistical data.

Fundamental analysis is a method or tool that investors use that seeks to determine the intrinsic value of a security by examining economic and financial factors. It considers macroeconomic factors such as the state of the economy and industry conditions.

Bitcoin is a decentralized digital cryptocurrency that was created in 2009 by an anonymous individual or group using the pseudonym Satoshi Nakamoto. It operates on a technology called blockchain, which is a distributed ledger that records all transactions across a network of computers.

Day trading involves buying and selling financial assets within the same trading day, with the goal of profiting from short-term price fluctuations, and positions are typically not held overnight.

CFD is a contract between an investor/trader and seller that demonstrates that the trader will need to pay the price difference between the current value of the asset and its value at the time of contract to the seller.

Risk management is a risk management model that involves controlling potential losses while maximizing profits. The main risk management tools are stop loss, take profit, calculation of position volume taking into account leverage and pip value.

-

Afghanistan

Afghanistan

-

Albania

Albania

-

Algeria

Algeria

-

Angola

Angola

-

Argentina

Argentina

-

Armenia

Armenia

-

Australia

Australia

-

Austria

Austria

-

Azerbaijan

Azerbaijan

-

Bahamas

Bahamas

-

Bahrain

Bahrain

-

Bangladesh

Bangladesh

-

Belarus

Belarus

-

Belgium

Belgium

-

Bolivia

Bolivia

-

Botswana

Botswana

-

Brazil

Brazil

-

Brunei

Brunei

-

Bulgaria

Bulgaria

-

Cambodia

Cambodia

-

Cameroon

Cameroon

-

Canada

Canada

-

Chile

Chile

-

China

China

-

Colombia

Colombia

-

Congo

Congo

-

Costa Rica

Costa Rica

-

Cote d'Ivoire

Cote d'Ivoire

-

Croatia

Croatia

-

Cuba

Cuba

-

Cyprus

Cyprus

-

Czechia

Czechia

-

DR Congo

DR Congo

-

Denmark

Denmark

-

Dominican Republic

Dominican Republic

-

Ecuador

Ecuador

-

Egypt

Egypt

-

El Salvador

El Salvador

-

Estonia

Estonia

-

Eswatini

Eswatini

-

Ethiopia

Ethiopia

-

Finland

Finland

-

France

France

-

Georgia

Georgia

-

Germany

Germany

-

Ghana

Ghana

-

Greece

Greece

-

Haiti

Haiti

-

Hong Kong

Hong Kong

-

Hungary

Hungary

-

India

India

-

Indonesia

Indonesia

-

Iran, Islamic republic

Iran, Islamic republic

-

Iraq

Iraq

-

Ireland

Ireland

-

Israel

Israel

-

Italy

Italy

-

Jamaica

Jamaica

-

Japan

Japan

-

Jordan

Jordan

-

Kazakhstan

Kazakhstan

-

Kenya

Kenya

-

Korea

Korea

-

Kuwait

Kuwait

-

Kyrgyzstan

Kyrgyzstan

-

Laos

Laos

-

Latvia

Latvia

-

Lebanon

Lebanon

-

Lesotho

Lesotho

-

Libya

Libya

-

Lithuania

Lithuania

-

Luxembourg

Luxembourg

-

Madagascar

Madagascar

-

Malaysia

Malaysia

-

Malta

Malta

-

Mauritius

Mauritius

-

Mexico

Mexico

-

Moldova

Moldova

-

Mongolia

Mongolia

-

Montenegro

Montenegro

-

Morocco

Morocco

-

Mozambique

Mozambique

-

Myanmar

Myanmar

-

Namibia

Namibia

-

Nepal

Nepal

-

Netherlands

Netherlands

-

New Zealand

New Zealand

-

Nigeria

Nigeria

-

North Macedonia

North Macedonia

-

Norway

Norway

-

Oman

Oman

-

Pakistan

Pakistan

-

Palestine

Palestine

-

Panama

Panama

-

Papua New Guinea

Papua New Guinea

-

Paraguay

Paraguay

-

Peru

Peru

-

Philippines

Philippines

-

Poland

Poland

-

Portugal

Portugal

-

Puerto Rico

Puerto Rico

-

Qatar

Qatar

-

Reunion

Reunion

-

Romania

Romania

-

Rwanda

Rwanda

-

Saudi Arabia

Saudi Arabia

-

Serbia

Serbia

-

Singapore

Singapore

-

Slovakia

Slovakia

-

Slovenia

Slovenia

-

Somalia

Somalia

-

South Africa

South Africa

-

Spain

Spain

-

Sri Lanka

Sri Lanka

-

Sweden

Sweden

-

Switzerland

Switzerland

-

Syria

Syria

-

Taiwan

Taiwan

-

Tajikistan

Tajikistan

-

Tanzania

Tanzania

-

Thailand

Thailand

-

Trinidad and Tobago

Trinidad and Tobago

-

Tunisia

Tunisia

-

Turkey

Turkey

-

UAE

UAE

-

Uganda

Uganda

-

Ukraine

Ukraine

-

United Kingdom

United Kingdom

-

United States

-

Uruguay

Uruguay

-

Uzbekistan

Uzbekistan

-

Venezuela

Venezuela

-

Vietnam

Vietnam

-

Yemen

Yemen

-

Zambia

Zambia

-

Zimbabwe

Zimbabwe

- Forex

- Crypto