Devaluation And Revaluation: A Complete Guide For Traders

Editorial Note: While we adhere to strict Editorial Integrity, this post may contain references to products from our partners. Here's an explanation for How We Make Money. None of the data and information on this webpage constitutes investment advice according to our Disclaimer.

Devaluation reduces a currency's value to make exports more competitive, while revaluation strengthens it to help control inflation. Since 2000, more than 45 countries have opted for devaluation, while fewer than 10 have chosen revaluation. These policy moves are closely monitored by traders, who adapt their strategies in Forex.

As part of a country’s broader economic strategy, currency value changes can significantly influence trade balances, investment flows, and inflation levels. Central banks operating under fixed or managed exchange rate regimes often rely on these mechanisms. Understanding the difference between devaluation and revaluation is crucial for traders, as both actions impact global market behavior in very different ways. Staying informed on these shifts helps market participants navigate changing economic landscapes with more confidence.

What is devaluation?

Devaluation is a policy-driven downward adjustment of a currency’s official exchange rate. It typically occurs within a fixed or semi‑fixed regime where authorities decide the exchange value instead of letting market forces do so. Countries generally use devaluation to boost exports and reduce trade deficits, as it lowers the price of domestic goods abroad and makes imports more expensive, encouraging local consumption. Devaluation can also ease the burden of sovereign debt by lowering the real value of domestic‑currency liabilities.

Why governments devalue their currency

Governments generally resort to devaluation when underlying fundamentals deteriorate:

Large and persistent current‑account deficits. If a country imports far more than it exports, foreign currency reserves may fall below critical levels. Many economists see deficits above 4–6% of GDP for several consecutive quarters as unsustainable.

Shrinking foreign reserves. The International Monetary Fund (IMF) warns that reserves below three months of import cover may signal liquidity stress. Devaluation reduces pressure by curbing imports and attracting foreign currency through exports.

High inflation and fiscal imbalances. Inflation erodes a currency’s real value; fiscal deficits above 6–8% of GDP can undermine investor confidence, triggering capital flight.

Political or geopolitical crises. Sanctions, civil unrest or regime changes can scare off investors. Devaluation is sometimes used to reset the currency and restore competitiveness.

How devaluation affects the economy and markets

Exports surge, imports become expensive. Following a devaluation, export volumes often rise 10–30% within a year because foreign buyers find local goods cheaper. Import prices may climb 15–25%, raising costs for consumers and manufacturers.

Inflation accelerates. Higher import costs feed into consumer prices. The CFI notes that devaluation increases aggregate demand, which lifts GDP but also stokes inflation. Consumer price inflation can rise 2–5% depending on how reliant the economy is on imports.

Bond yields and equity volatility jump. Investors demand a premium for holding local assets when the currency weakens. Bond yields can rise 200–500 basis points, and stock markets may swing 10–15% as sectors reprice.

External debt servicing worsens. When a country owes debt in foreign currency, devaluation increases the local‑currency cost of servicing that debt, straining public finances.

Real‑world example: Turkey’s lira crisis

Turkey illustrates the risks of unmanaged currency adjustments. Between 2013 and 2023 the lira slid steadily amid political turbulence, converging into a dramatic devaluation in 2021. The lira’s decline accelerated when President Erdogan pressured the central bank to cut interest rates despite soaring inflation. By June 2023, the lira had fallen to ₺23.3 per U.S. dollar, having traded around 10 per dollar just two years earlier.

Analysts interviewed by Al Jazeera said the lira’s plunge reflected years of suppressed inflation and heavy central‑bank interventions; selling foreign reserves kept the exchange rate artificially strong and delayed necessary monetary tightening. Inflation peaked at 85.5% in October 2022, eroding real incomes and forcing households to hold foreign currency or goods. The experience shows that persistent devaluation can undermine economic stability if not paired with credible fiscal and monetary reforms.

What is revaluation?

Revaluation is the opposite policy move, marked by an upward adjustment of a currency’s official value relative to a benchmark. It aims to strengthen a currency in order to curb imported inflation, rebalance massive trade surpluses or align artificially low exchange rates with global norms. Such action is only possible under a fixed or managed regime where authorities set the reference rate.

Drivers of revaluation

Prolonged current‑account surpluses. Surpluses above 5–7% of GDP over several quarters suggest a currency is undervalued relative to fundamentals. Allowing the currency to appreciate can reduce trade tensions and prevent overheating.

Rapid reserve accumulation. When foreign exchange reserves exceed 200–250% of short‑term external debt, policymakers may revalue to prevent excessive liquidity and imported inflation.

Low inflation and rising wages. If domestic inflation falls below 2–3%, strengthening the currency can keep import prices in check and preserve purchasing power.

External pressure or trade negotiations. International partners or institutions such as the U.S. Treasury sometimes press countries to revalue if their currencies are perceived as unfairly cheap.

Effects of revaluation

Imports become cheaper. A stronger currency lowers the local price of imported goods by 10–20%, helping moderate inflation and benefiting consumers.

Exports decline. Domestic goods become pricier for foreign buyers, often reducing export volumes by 5–15%. This trade‑off can slow economic growth in export‑dependent sectors.

Reduced inflation and debt burden. Stronger currency values dampen imported inflation and make it less costly to service foreign‑denominated debt, improving fiscal sustainability.

Higher capital inflows. Confidence in a stronger currency may attract foreign investment, boosting short‑term portfolio flows.

Real‑world example: China’s 2005 revaluation

China provides a textbook case of revaluation. After maintaining a fixed peg of RMB 8.28 per U.S. dollar for over a decade, the People’s Bank of China revalued the yuan by 2.1% on 21 July 2005 and switched to a managed float against a basket of currencies. Over the next three years, Beijing allowed the yuan to appreciate a further 19%. The move responded to rising trade surpluses and foreign pressure, helping curb imported inflation and signalling China’s willingness to move toward a more flexible exchange rate regime.

Devaluation vs revaluation: core differences

The difference between devaluation and revaluation lies in the direction and intent of the policy. While both require a fixed or managed exchange‑rate system, they respond to opposite macroeconomic conditions. Devaluation seeks to restore competitiveness when reserves and exports are weak; revaluation aims to cool an overheating economy and stem imported inflation. The table below summarises the contrasting impacts of revaluation and devaluation:

| Criterion | Devaluation | Revaluation |

|---|---|---|

| Direction of adjustment | Downward: currency value lowered relative to a benchmark | Upward: currency value increased relative to a benchmark |

| Policy objective | Boost exports, correct trade deficits, slow reserve depletion | Tame imported inflation, reduce trade surpluses, align undervalued currency |

| Typical economic backdrop | High deficits, falling reserves, high inflation, political or economic crises | Large surpluses, rapid reserve growth, low inflation, overheating economy |

| Impact on trade | Exports become cheaper and increase 10–30%; imports cost more and decline 15–25% | Imports become cheaper and grow 10–20%; exports may drop 5–15% |

| Inflation effect | Adds inflation; consumer prices typically rise 2–5% | Reduces inflation; consumer prices fall 2–4% |

| Currency confidence | Often undermined; may trigger capital outflows and higher risk premiums | Usually improves; attracts investment and reduces financing costs |

| Examples | Turkey’s repeated lira devaluations amid unorthodox monetary policy | China’s 2005 yuan revaluation and subsequent appreciation |

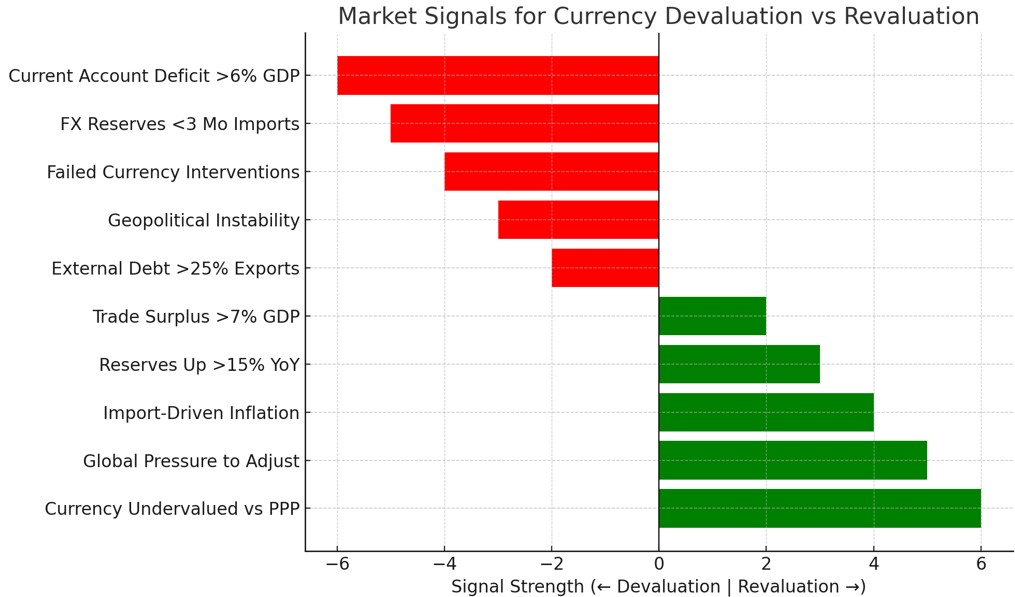

Market signals to watch

Because these policy moves are rare and consequential, traders watch leading indicators to anticipate them. Signals that may precede currency devaluation and revaluation include:

Current‑account trends. Persistent deficits or surpluses are early clues. When deficits exceed 4–6% of GDP for three or more quarters, devaluation pressure increases; surpluses above 5–7% flag potential revaluation.

Foreign reserve trajectories. Depleting reserves and frantic interventions to defend a peg suggest an unsustainable currency level. Conversely, rapidly rising reserves point to an undervalued currency.

Interest‑rate policy and inflation. Sharp divergence between domestic and foreign rates can trigger capital flows. High inflation without rate hikes may foreshadow devaluation, while low inflation and rate hikes can lead to revaluation.

Official rhetoric and trade negotiations. Statements from finance ministries, central banks or international bodies (like the IMF) often hint at looming adjustments. Trade disputes and accusations of “currency manipulation” can accelerate revaluation demands.

When a devaluation may be imminent

Devaluation often follows multiple quarters of economic strain, especially when foreign exchange reserves can no longer support an overvalued peg. Key red flags include:

Persistent current account deficits exceeding 4–6% of GDP for 3+ quarters. Suggests the country imports far more than it exports, draining reserves.

Central bank reserves falling below 3 months of import cover. The IMF regards this as a critical liquidity warning threshold.

Domestic currency interventions failed repeatedly. Frequent interventions (e.g., USD sales) without price stability signal an unsustainable peg.

Geopolitical instability or sanctions risk. Events like civil unrest, war, or global sanctions can drive sudden reserve outflows and debt service stress.

External debt repayments rising above 25% of annual exports. This ratio signals severe external vulnerability, often prompting IMF engagement.

Signs of a possible revaluation

Revaluation is rare and typically signals economic strength or an attempt to contain overheating. Signs that may precede revaluation include:

Export-led trade surpluses exceeding 5–7% of GDP. Indicates the local currency may be undervalued relative to its fundamentals.

Strong capital inflows and reserve accumulation. Reserves rising at over 10–15% YoY, especially in Asia-Pacific and oil-rich nations.

Inflation rising due to imported goods. Cheap currency makes imports more expensive, prompting policymakers to adjust value upward.

IMF or trade partners requesting currency alignment. Revaluation may follow G20 or IMF scrutiny, especially under managed exchange rates.

Undervalued currency based on purchasing power parity (PPP). A widening gap between PPP and official rate signals built-in appreciation pressure.

Why traders must track these trends

Anticipating devaluation vs revaluation scenarios is a key macro skill. It allows traders to:

Position early in key Forex pairs (e.g., shorting currencies ahead of devaluation like USD/EGP, or going long undervalued ones like SGD).

Hedge inflation risk using commodities or inflation-indexed bonds.

Avoid sovereign credit risk in debt-heavy economies approaching currency shocks.

Identify export/import sectors poised for repricing post-adjustment.

Currency devaluation and revaluation: trader strategy guide

Currency adjustments reshape market fundamentals across asset classes. Whether facing devaluation or revaluation, traders must realign their strategies to hedge risks, capture sectoral advantages, and avoid macro vulnerabilities.

Actions for traders during devaluation

Devaluation weakens the domestic currency, raising the cost of imports and encouraging exports. Key tactics include:

Long exporters and commodity producers. Companies that sell abroad benefit from a weaker currency, as their goods become cheaper for foreign buyers. Sectors like agriculture, mining and industrials often outperform.

Reduce exposure to import‑dependent sectors. Retail, automotive and technology companies reliant on imported components face margin pressure. Avoid or short these equities until input costs stabilize.

Hedge currency risk. Use futures, options or non‑deliverable forwards to protect against further declines in the local currency. For example, shorting the local currency against the U.S. dollar can offset losses in domestic investments.

Hold inflation hedges. Gold, real estate investment trusts and inflation‑linked bonds tend to perform well when devaluation fuels price increases. Actions for traders during revaluation.

Revaluation strengthens the domestic currency, lowering import costs and potentially hurting exports. Key positioning strategies:

Focus on import‑heavy industries. Consumer discretionary, retailers and tech manufacturers benefit from cheaper imported goods, improving margins.

Avoid overexposed exporters. Exporters may experience falling revenues as their products become pricier abroad. Assess which companies have diversified revenue streams or hedging programs.

Adjust carry trades. A stronger currency reduces the appeal of borrowing in low‑yield currencies to invest in high‑yield assets. Rebalance positions to avoid negative carry.

Play strong currency pairs. Enter long positions on the revalued currency in pairs such as USD/CNH or EUR/SGD, anticipating continued strength.

When you’re positioning for potential devaluations or revaluations, the broker you pick matters as much as your macro read. You want fast, reliable execution around policy headlines, access to the right pairs (including “exotics”), and risk tools that don’t buckle during squeezes. The options below are popular with macro-minded Forex traders because they combine deep market access with sensible costs and sturdy platforms.

| Currency pairs | Min. deposit, $ | Max. leverage | Deposit fee, % | Withdrawal fee, $ | Regulation | TU overall score | Open an account | |

|---|---|---|---|---|---|---|---|---|

| 50 | 10 | 1:1000 | No | No | No | 8.05 | Go to broker Your capital is at risk.

|

|

| 60 | 100 | 1:300 | No | No | CySEC, FCA, ASIC, FMA, FSCA, FSA Seychelles, EFSA, MAS, DFSA, SCB | 7.57 | Go to broker 80% of retail CFD accounts lose money. |

|

| 68 | No | 1:200 | No | 0-15 | FSC (BVI), ASIC, IIROC, FCA, CFTC, NFA | 6.89 | Go to broker Your capital is at risk. |

|

| 69 | 50 | 1:50 | No | No | CFTC, NFA | 6.15 | Go to broker Your capital is at risk. |

|

| 80 | 100 | 1:50 | No | No | CIMA, FCA, FSA (Japan), NFA, IIROC, ASIC, CFTC | 6.87 | Study review |

Revaluation vs devaluation in today’s context

Recent years highlight how devaluation and revaluation of currency policy plays out in practice:

Nigeria (2023–2024). The Nigerian central bank allowed the naira to drop more than 36% after unifying multiple exchange rates and removing fuel subsidies. Analysts described the move as a long‑overdue devaluation to reflect market realities and attract investment. It triggered inflation spikes but improved liquidity in the official Forex market.

Singapore (2024). The Monetary Authority of Singapore uses the exchange rate rather than interest rates to manage inflation. In 2024 it shifted its currency band upward to slow imported inflation, a form of managed revaluation. The move signalled confidence in economic growth and brought down the cost of imports.

These cases illustrate why traders monitor macro indicators: revaluations often come from positions of strength, while devaluations stem from imbalances and crises.

Spotting central bank signals and political motives in Forex

When traders hear devaluation or revaluation, they usually think about governments making an announcement, but the real edge comes from anticipating these moves before they’re declared. Beginners often miss that central banks rarely act out of the blue; they leave clues in trade balances, foreign reserve reports, and even political speeches. For example, if a country with a fixed exchange rate starts burning through reserves to defend its currency, it’s often a sign that devaluation is coming. Reading between the lines of these economic signals allows traders to position themselves before the crowd.

Another overlooked insight is that revaluation is not always about “strength.” Sometimes a government revalues to curb imported inflation or to maintain political credibility with trading partners. This means traders shouldn’t just celebrate a stronger currency, they should ask why it happened. If the revaluation is artificial and not backed by productivity or capital inflows, it often leads to volatility later. Beginners who train themselves to connect these monetary shifts with broader trade and political dynamics will see Forex markets less as random swings and more as calculated power plays.

Conclusion

Devaluation and revaluation are more than abstract economic tools. They are powerful levers that alter currency strength, trade flows, and capital movement. For traders, understanding the timing and effects of each, and recognizing the subtle cues from central banks, can mean the difference between gains and unexpected losses.

When facing devaluation and revaluation of currency, always analyze macroeconomic context, global sentiment, and regional risk factors to adapt your strategy with precision.

FAQs

Can central banks devalue their currency more than once in a year?

Yes. In cases of extreme economic stress or hyperinflation, a country may conduct multiple devaluations within a single year. For example, Argentina devalued its peso three times between August and December 2023 to meet IMF conditions and reflect market reality.

How does currency revaluation impact international students and expats?

Revaluation strengthens the local currency, making tuition fees, rent, and daily expenses costlier for foreign students and expats paying in weaker currencies. Conversely, locals studying abroad may benefit from improved purchasing power.

Do cryptocurrencies react to devaluation and revaluation events?

Yes. In economies experiencing rapid devaluation (like Nigeria or Lebanon), local demand for stablecoins or Bitcoin often surges as residents seek to hedge against currency collapse, leading to regional price premiums and increased volumes.

Can companies hedge against devaluation or revaluation risks?

Multinational companies often use forward contracts, currency swaps, and natural hedging to manage FX risk. Firms operating in volatile markets frequently report currency translation effects in earnings, and proactive hedging can reduce volatility by 20–40%.

Editors' Top Picks and Insights

SK Hynix debuts on Nasdaq: Largest U.S. offering by foreign company

SpaceX falls out of orbit: Does anyone still want Musk’s stock?

The crypto IPO problem: How high-profile listings became investor traps

U.S. Bitcoin reserve: Trump’s unrealized crypto promise

Aiming for leadership: Payment giants prepare a new stablecoin

Proof of Reserves: the new standard for cryptocurrency exchanges

Related Articles

Team that worked on the article

Emilio is a futures trader and financial writer who specializes in technical analysis, market news, and trading psychology. He began his career by completing the Cornerstone Traders Qualification under the mentorship of a gold futures veteran from Bank of America on Wall Street.

Dan Blystone began his trading career in 1998 as an arbitrage clerk on the floor of the Chicago Mercantile Exchange (CME). He later traded bond and Eurex futures at proprietary firms such as Altea Trading, gaining valuable experience in high-frequency trading and risk management.

Chinmay Soni is a financial analyst with more than 5 years of experience in working with stocks, Forex, derivatives, and other assets. As a founder of a boutique research firm and an active researcher, he covers various industries and fields, providing insights backed by statistical data.

Scalping in trading is a strategy where traders aim to make quick, small profits by executing numerous short-term trades within seconds or minutes, capitalizing on minor price fluctuations.

Yield refers to the earnings or income derived from an investment. It mirrors the returns generated by owning assets such as stocks, bonds, or other financial instruments.

A long position in Forex, represents a positive outlook on the future value of a currency pair. When a trader assumes a long position, they are essentially placing a bet that the base currency in the pair will appreciate in value compared to the quote currency.

Index in trading is the measure of the performance of a group of stocks, which can include the assets and securities in it.

An investor is an individual, who invests money in an asset with the expectation that its value would appreciate in the future. The asset can be anything, including a bond, debenture, mutual fund, equity, gold, silver, exchange-traded funds (ETFs), and real-estate property.

-

Afghanistan

Afghanistan

-

Albania

Albania

-

Algeria

Algeria

-

Angola

Angola

-

Argentina

Argentina

-

Armenia

Armenia

-

Australia

Australia

-

Austria

Austria

-

Azerbaijan

Azerbaijan

-

Bahamas

Bahamas

-

Bahrain

Bahrain

-

Bangladesh

Bangladesh

-

Belarus

Belarus

-

Belgium

Belgium

-

Bolivia

Bolivia

-

Botswana

Botswana

-

Brazil

Brazil

-

Brunei

Brunei

-

Bulgaria

Bulgaria

-

Cambodia

Cambodia

-

Cameroon

Cameroon

-

Canada

Canada

-

Chile

Chile

-

China

China

-

Colombia

Colombia

-

Congo

Congo

-

Costa Rica

Costa Rica

-

Cote d'Ivoire

Cote d'Ivoire

-

Croatia

Croatia

-

Cuba

Cuba

-

Cyprus

Cyprus

-

Czechia

Czechia

-

DR Congo

DR Congo

-

Denmark

Denmark

-

Dominican Republic

Dominican Republic

-

Ecuador

Ecuador

-

Egypt

Egypt

-

El Salvador

El Salvador

-

Estonia

Estonia

-

Eswatini

Eswatini

-

Ethiopia

Ethiopia

-

Finland

Finland

-

France

France

-

Georgia

Georgia

-

Germany

Germany

-

Ghana

Ghana

-

Greece

Greece

-

Haiti

Haiti

-

Hong Kong

Hong Kong

-

Hungary

Hungary

-

India

India

-

Indonesia

Indonesia

-

Iran, Islamic republic

Iran, Islamic republic

-

Iraq

Iraq

-

Ireland

Ireland

-

Israel

Israel

-

Italy

Italy

-

Jamaica

Jamaica

-

Japan

Japan

-

Jordan

Jordan

-

Kazakhstan

Kazakhstan

-

Kenya

Kenya

-

Korea

Korea

-

Kuwait

Kuwait

-

Kyrgyzstan

Kyrgyzstan

-

Laos

Laos

-

Latvia

Latvia

-

Lebanon

Lebanon

-

Lesotho

Lesotho

-

Libya

Libya

-

Lithuania

Lithuania

-

Luxembourg

Luxembourg

-

Madagascar

Madagascar

-

Malaysia

Malaysia

-

Malta

Malta

-

Mauritius

Mauritius

-

Mexico

Mexico

-

Moldova

Moldova

-

Mongolia

Mongolia

-

Montenegro

Montenegro

-

Morocco

Morocco

-

Mozambique

Mozambique

-

Myanmar

Myanmar

-

Namibia

Namibia

-

Nepal

Nepal

-

Netherlands

Netherlands

-

New Zealand

New Zealand

-

Nigeria

Nigeria

-

North Macedonia

North Macedonia

-

Norway

Norway

-

Oman

Oman

-

Pakistan

Pakistan

-

Palestine

Palestine

-

Panama

Panama

-

Papua New Guinea

Papua New Guinea

-

Paraguay

Paraguay

-

Peru

Peru

-

Philippines

Philippines

-

Poland

Poland

-

Portugal

Portugal

-

Puerto Rico

Puerto Rico

-

Qatar

Qatar

-

Reunion

Reunion

-

Romania

Romania

-

Rwanda

Rwanda

-

Saudi Arabia

Saudi Arabia

-

Serbia

Serbia

-

Singapore

Singapore

-

Slovakia

Slovakia

-

Slovenia

Slovenia

-

Somalia

Somalia

-

South Africa

South Africa

-

Spain

Spain

-

Sri Lanka

Sri Lanka

-

Sweden

Sweden

-

Switzerland

Switzerland

-

Syria

Syria

-

Taiwan

Taiwan

-

Tajikistan

Tajikistan

-

Tanzania

Tanzania

-

Thailand

Thailand

-

Trinidad and Tobago

Trinidad and Tobago

-

Tunisia

Tunisia

-

Turkey

Turkey

-

UAE

UAE

-

Uganda

Uganda

-

Ukraine

Ukraine

-

United Kingdom

United Kingdom

-

United States

-

Uruguay

Uruguay

-

Uzbekistan

Uzbekistan

-

Venezuela

Venezuela

-

Vietnam

Vietnam

-

Yemen

Yemen

-

Zambia

Zambia

-

Zimbabwe

Zimbabwe

- Forex

- Crypto