U.S. student-loan collections shift raises risks for borrowers in default

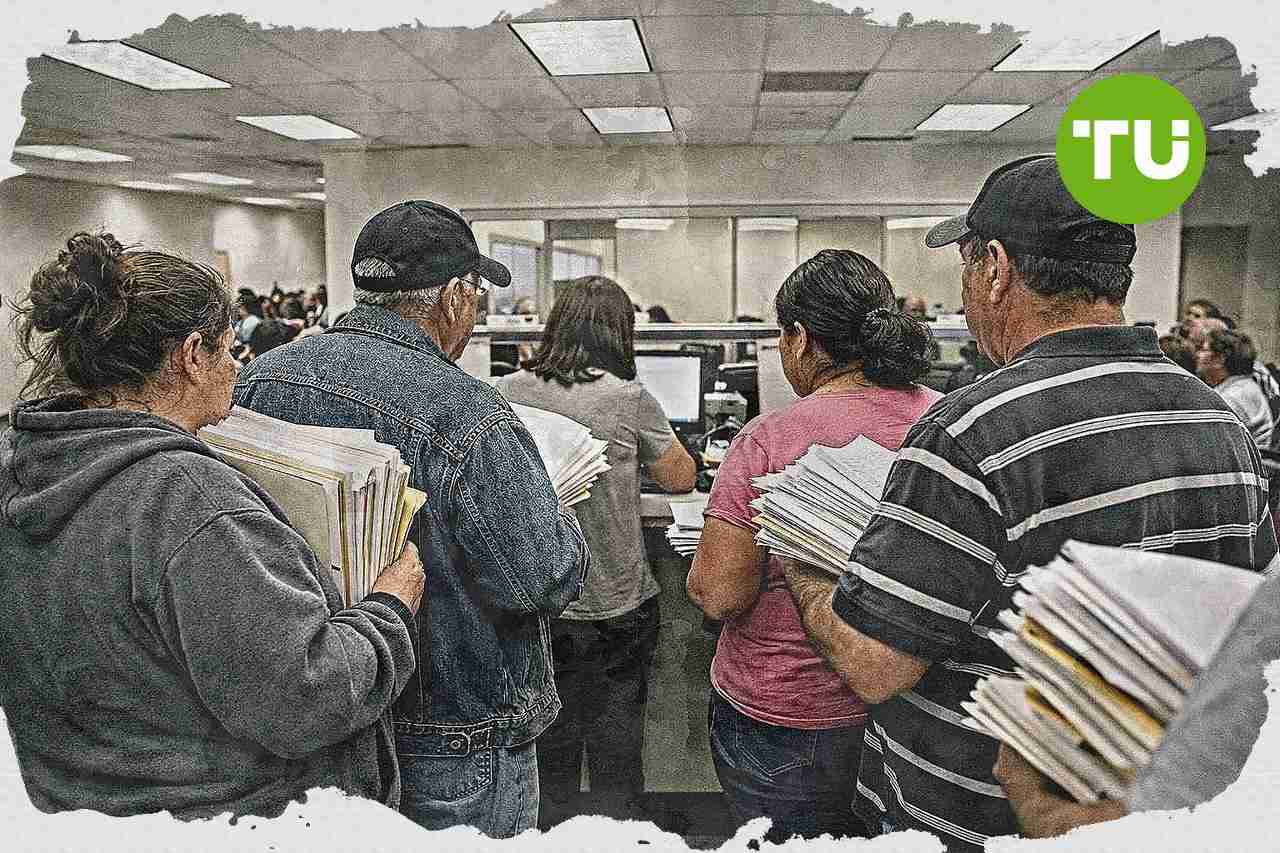

More than 10 million federal student-loan borrowers are in default or delinquency as the Trump administration moves defaulted accounts from the Department of Education to the Treasury Department for collection. The change could bring private debt collectors with a record of regulatory penalties back into the system, adding potential fees, confusion and redefault risks for borrowers.

Highlights

- Defaulted federal student loan borrowers will transfer to Treasury’s Cross-Servicing program, reviving the use of private collection agencies like Pioneer Credit Recovery and Transworld Systems.

- In 2024, Pioneer was ordered to pay $100 million and Transworld $2.5 million in penalties for prior deceptive or abusive debt collection practices affecting borrowers.

- Policy experts warn the shift raises risks of higher fees, weaker complaint resolution, and inadequate oversight as Treasury lacks proven student-loan-specific expertise.

Treasury transfer revives private collection concerns

As first reported by Business Insider, defaulted federal student-loan borrowers are set to move into the Treasury Department's Cross-Servicing program, which relies on private contractors to collect government debts. The Department of Education has not said when the current pause on involuntary collections will end, and it did not specify how extensively Pioneer Credit Recovery and Transworld Systems will be used once collections resume.Former officials and policy specialists say the operational shift could complicate repayment for borrowers already struggling to exit default. Bonnie Latreille, a former official in the Education Department's Federal Student Aid office, says there is little reason to expect these companies to fully protect borrower rights, while former Federal Student Aid loan portfolio executive Colleen Campbell says adding more agencies and vendors makes the process harder for borrowers to navigate.

The administration argues the Treasury is better positioned to run collections. Treasury Secretary Scott Bessent said in a March press release that the department has the experience and financial expertise to impose stronger discipline on the program, and Undersecretary Nicholas Kent said in April that Treasury is well equipped to manage federal student loans as the transfer begins with defaulted borrowers before expanding further.

Past enforcement actions and borrower impact

The return of private collectors revives scrutiny of companies previously accused by federal watchdogs of deceptive or abusive conduct. The Consumer Financial Protection Bureau said private agencies misrepresented options to borrowers, including implying lawsuits were likely and steering some people into more expensive repayment paths.In 2017, the CFPB sued Pioneer for what it described as deceptive and abusive practices, including directing borrowers toward costly forbearance instead of more favorable income-driven repayment plans. A court ordered the company in 2024 to pay $100 million to affected borrowers, while Transworld Systems was fined $2.5 million that year by the CFPB for filing debt-collection lawsuits without proof the debts were owed; Transworld said it settled to avoid costly litigation, and Navient, which oversaw Pioneer, denied wrongdoing.

Education policy experts say borrowers could now face higher collection fees, weaker complaint resolution and a greater chance of falling back into default. Campbell also points to concerns about poor coordination between agencies during the handoff, while Sara Partridge of the Center for American Progress says there is no evidence Treasury has the student-loan-specific expertise needed to oversee these contractors effectively.

Our earlier coverage of the U.S. gross national debt highlighted that total federal borrowing has climbed to $39.20 trillion, with the debt rising by about $8.19 billion per day and potentially reaching $40 trillion by late September 2026. We also noted that higher interest rates are increasing the government’s debt-servicing burden, adding pressure to federal finances.

Latest Retirement Policies News

-

Afghanistan

Afghanistan

-

Albania

Albania

-

Algeria

Algeria

-

Angola

Angola

-

Argentina

Argentina

-

Armenia

Armenia

-

Australia

Australia

-

Austria

Austria

-

Azerbaijan

Azerbaijan

-

Bahamas

Bahamas

-

Bahrain

Bahrain

-

Bangladesh

Bangladesh

-

Belarus

Belarus

-

Belgium

Belgium

-

Bolivia

Bolivia

-

Botswana

Botswana

-

Brazil

Brazil

-

Brunei

Brunei

-

Bulgaria

Bulgaria

-

Cambodia

Cambodia

-

Cameroon

Cameroon

-

Canada

Canada

-

Chile

Chile

-

China

China

-

Colombia

Colombia

-

Congo

Congo

-

Costa Rica

Costa Rica

-

Cote d'Ivoire

Cote d'Ivoire

-

Croatia

Croatia

-

Cuba

Cuba

-

Cyprus

Cyprus

-

Czechia

Czechia

-

DR Congo

DR Congo

-

Denmark

Denmark

-

Dominican Republic

Dominican Republic

-

Ecuador

Ecuador

-

Egypt

Egypt

-

El Salvador

El Salvador

-

Estonia

Estonia

-

Eswatini

Eswatini

-

Ethiopia

Ethiopia

-

Finland

Finland

-

France

France

-

Georgia

Georgia

-

Germany

Germany

-

Ghana

Ghana

-

Greece

Greece

-

Haiti

Haiti

-

Hong Kong

Hong Kong

-

Hungary

Hungary

-

India

India

-

Indonesia

Indonesia

-

Iran, Islamic republic

Iran, Islamic republic

-

Iraq

Iraq

-

Ireland

Ireland

-

Israel

Israel

-

Italy

Italy

-

Jamaica

Jamaica

-

Japan

Japan

-

Jordan

Jordan

-

Kazakhstan

Kazakhstan

-

Kenya

Kenya

-

Korea

Korea

-

Kuwait

Kuwait

-

Kyrgyzstan

Kyrgyzstan

-

Laos

Laos

-

Latvia

Latvia

-

Lebanon

Lebanon

-

Lesotho

Lesotho

-

Libya

Libya

-

Lithuania

Lithuania

-

Luxembourg

Luxembourg

-

Madagascar

Madagascar

-

Malaysia

Malaysia

-

Malta

Malta

-

Mauritius

Mauritius

-

Mexico

Mexico

-

Moldova

Moldova

-

Mongolia

Mongolia

-

Montenegro

Montenegro

-

Morocco

Morocco

-

Mozambique

Mozambique

-

Myanmar

Myanmar

-

Namibia

Namibia

-

Nepal

Nepal

-

Netherlands

Netherlands

-

New Zealand

New Zealand

-

Nigeria

Nigeria

-

North Macedonia

North Macedonia

-

Norway

Norway

-

Oman

Oman

-

Pakistan

Pakistan

-

Palestine

Palestine

-

Panama

Panama

-

Papua New Guinea

Papua New Guinea

-

Paraguay

Paraguay

-

Peru

Peru

-

Philippines

Philippines

-

Poland

Poland

-

Portugal

Portugal

-

Puerto Rico

Puerto Rico

-

Qatar

Qatar

-

Reunion

Reunion

-

Romania

Romania

-

Rwanda

Rwanda

-

Saudi Arabia

Saudi Arabia

-

Serbia

Serbia

-

Singapore

Singapore

-

Slovakia

Slovakia

-

Slovenia

Slovenia

-

Somalia

Somalia

-

South Africa

South Africa

-

Spain

Spain

-

Sri Lanka

Sri Lanka

-

Sweden

Sweden

-

Switzerland

Switzerland

-

Syria

Syria

-

Taiwan

Taiwan

-

Tajikistan

Tajikistan

-

Tanzania

Tanzania

-

Thailand

Thailand

-

Trinidad and Tobago

Trinidad and Tobago

-

Tunisia

Tunisia

-

Turkey

Turkey

-

UAE

UAE

-

Uganda

Uganda

-

Ukraine

Ukraine

-

United Kingdom

United Kingdom

-

United States

-

Uruguay

Uruguay

-

Uzbekistan

Uzbekistan

-

Venezuela

Venezuela

-

Vietnam

Vietnam

-

Yemen

Yemen

-

Zambia

Zambia

-

Zimbabwe

Zimbabwe

- Forex

- Crypto