How Rate Hikes And Cuts Really Impact The Economy And Markets

Editorial Note: While we adhere to strict Editorial Integrity, this post may contain references to products from our partners. Here's an explanation for How We Make Money. None of the data and information on this webpage constitutes investment advice according to our Disclaimer.

Rate hikes and cuts influence markets not just through direction but through timing and intensity. Fast hikes can trigger recessions while sudden cuts often signal panic. Understanding these cycles helps investors read economic signals beyond headlines.

Rate hikes and cuts are not just policy levers. They are signals sent into a fragile system that reacts with delay distortion and often denial. Markets rarely move in sync with central bank decisions. They move on expectations which makes timing the cycle as much about psychology as it is about math. The problem is not just when rates rise or fall. It is how fast and from what level. When hikes come too late and cuts come too fast the economy often snaps before it bends. Understanding the lag between monetary action and economic impact is not optional. It is the difference between preparing for a slowdown and getting blindsided by one.

Understanding monetary policy cycles

Monetary policy plays a central role in shaping the economy. Through interest rate changes and money supply management, central banks attempt to maintain price stability, encourage growth, and manage inflation. These actions do not happen at random; they follow a cycle that responds to economic conditions. Understanding how these cycles work helps investors, businesses, and individuals prepare for shifts in borrowing costs, market sentiment, and currency value.

The role of central banks in economic stability

Central banks are responsible for keeping economies balanced during both booms and downturns.

What central banks do

Control interest rates to influence borrowing and spending.

Manage money supply to support liquidity and credit availability.

Monitor inflation, employment, and GDP growth to guide decisions.

How they maintain stability

During periods of overheating or rising inflation, central banks raise rates to cool demand.

When growth slows or a recession looms, they lower rates or inject liquidity to encourage borrowing and investment.

They act as lenders of last resort during crises to prevent financial system collapse.

Central bank moves affect everything from mortgage rates to job creation. Their policies directly influence consumer confidence, business investment, and currency strength. Investors closely watch central bank signals to adjust portfolios accordingly.

Objectives of rate hikes and cuts

Interest rate changes are one of the main tools used to manage the economic cycle.

| Policy Action | When Central Banks Raise Rates | When Central Banks Cut Rates |

|---|---|---|

| Primary Goal | To reduce inflation by making borrowing more expensive | To stimulate the economy during slowdowns or recessions |

| Economic Intent | To cool down overheating sectors like housing or credit markets | To make credit cheaper and more accessible |

| Currency Objective | To protect currency value or attract foreign capital | To weaken the currency and support exports |

| Impact on Spending | Slows consumer spending and business borrowing | Encourages consumer and business spending |

| Impact on Currency | Strengthens the national currency | Weakens the national currency |

| Impact on Assets | Can reduce asset price bubbles, but may slow growth excessively | Can boost asset prices but may cause inflation or speculative bubbles |

| Overall Economic Effect | Disinflationary, potentially contractionary | Stimulative, but with inflation risk if prolonged |

Moving too fast or too slow can either choke growth or let inflation get out of control. Markets often react before the actual rate change, based on expectations. The full effects of a rate hike or cut may take months to show in the real economy.

Historical patterns of rate hikes leading to recessions

Interest rate hikes are a central bank’s primary tool to cool an overheating economy. But when raised too quickly or too aggressively, they can tip economies into recession. History shows that many economic downturns followed periods of rapid tightening. Studying these past cycles helps identify warning signs and understand the impact of policy decisions on markets, employment, and growth.

Looking at past rate hike cycles reveals a pattern. When borrowing becomes more expensive too fast, spending slows, business confidence dips, and recessions often follow.

United States 1980s Volcker shock

The Federal Reserve raised rates to nearly 20 percent to fight double-digit inflation. While inflation came down, the aggressive hikes triggered back-to-back recessions in 1980 and 1981–82. Unemployment soared, but the policy is credited with restoring long-term price stability.

Dot-com bubble and 2001 recession

The Fed hiked rates from 4.75 percent to 6.5 percent between 1999 and 2000. Tightening coincided with the bursting of the tech bubble. The economy fell into recession in early 2001 as business investment collapsed and job losses mounted.

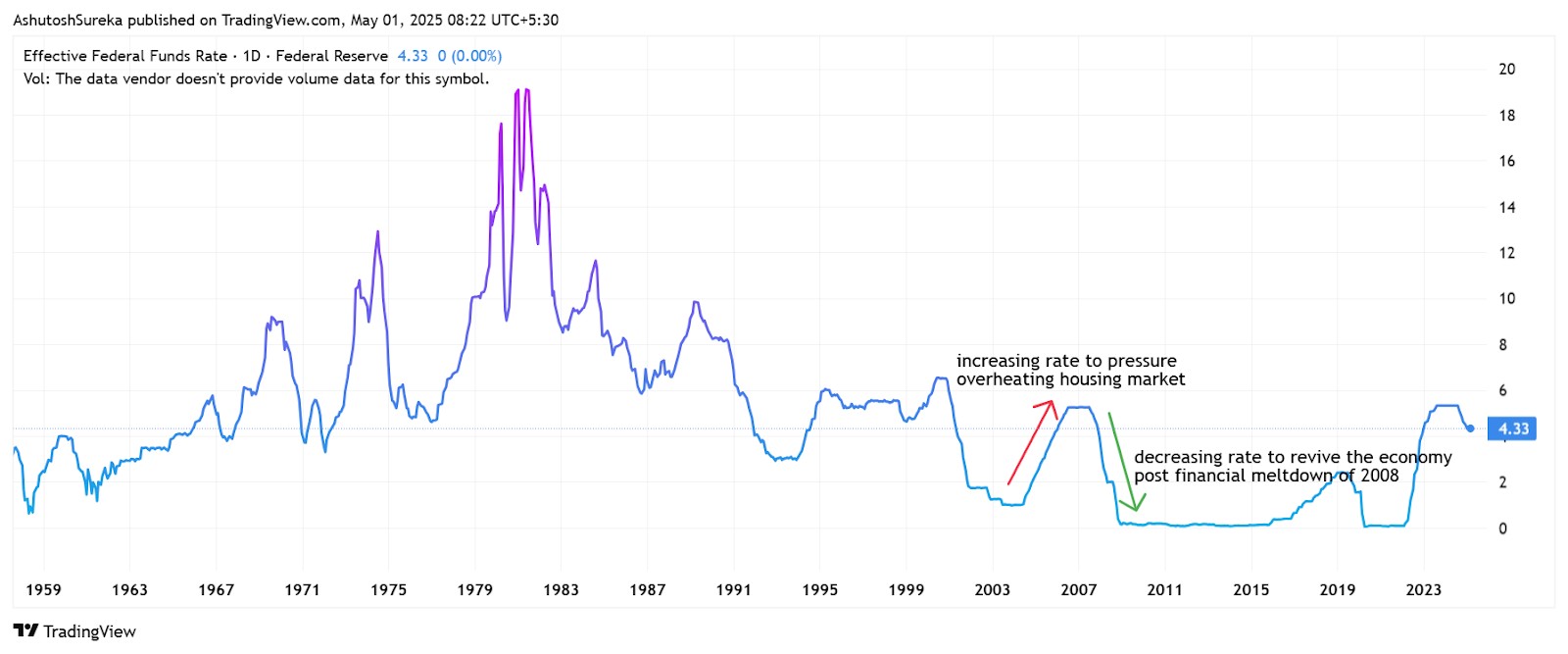

2004–2006 tightening and the 2008 crisis

Rates rose steadily from 1 percent to 5.25 percent over two years. Though the hikes were gradual, they added pressure to an overheated housing market. Combined with lax lending practices, rising rates helped trigger the mortgage meltdown and the 2008 financial crisis.

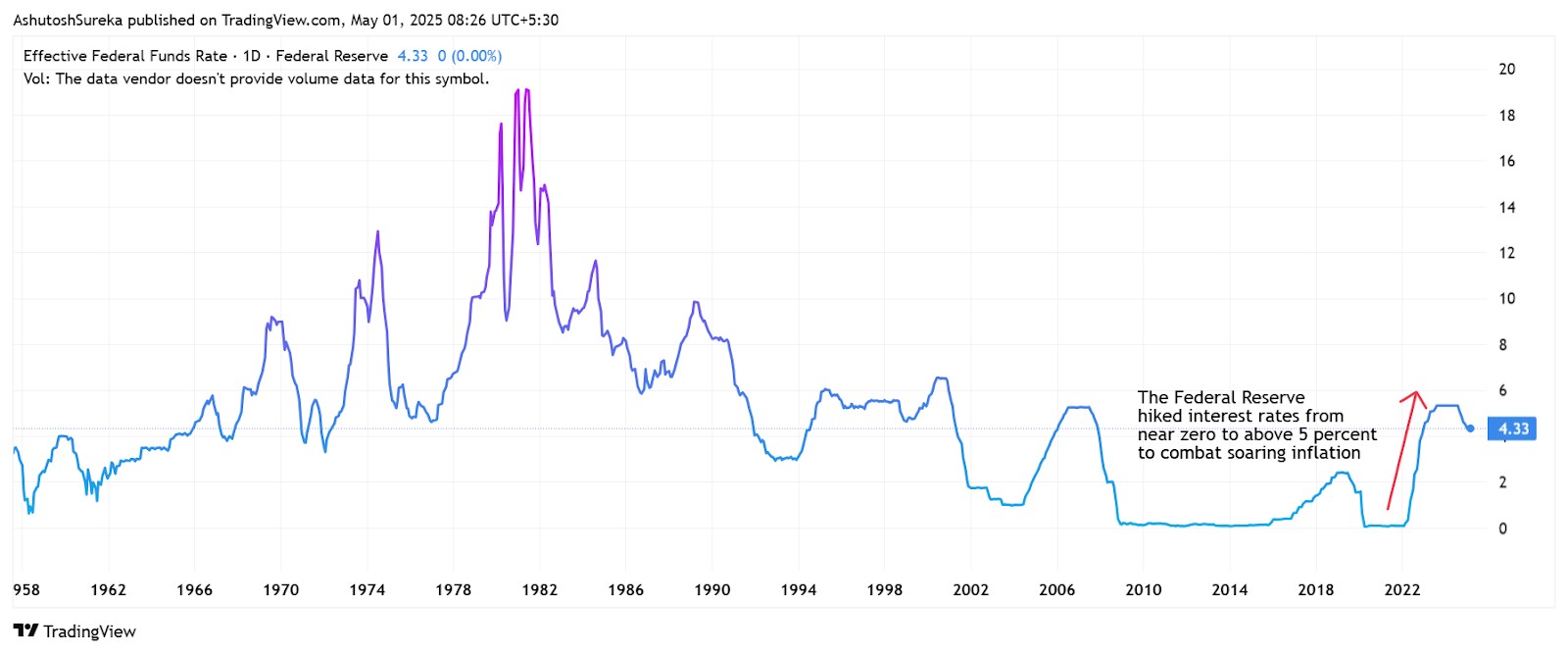

2022–2023 post-COVID tightening

The Fed rapidly raised rates from near-zero to over 5 percent in response to surging inflation. By mid-2023, signs of economic slowing and financial stress began to emerge in housing and credit markets. Though not yet a full recession, concerns over a downturn remain.

What history tells us:

Sharp or prolonged rate hikes often precede recessions.

The full impact is delayed and can take months or even years to unfold.

The sectors most affected tend to be housing, lending, and consumer spending.

Indicators preceding economic downturns

Before a recession officially begins, several economic indicators tend to flash early warnings – particularly during periods of monetary tightening. These signals are closely monitored by economists, investors, and policymakers because they often precede broader downturns.

One of the most reliable recession indicators is the inverted yield curve. This occurs when short-term interest rates rise above long-term rates, reflecting investors’ expectations of an economic slowdown. Historically, an inverted yield curve has preceded nearly every U.S. recession over the past five decades.

As central banks raise interest rates and borrowing becomes more expensive, consumer spending tends to decline. People become more cautious, reducing discretionary purchases and delaying major investments. Consumer sentiment often drops sharply in the months leading up to an economic contraction.

Tightening monetary conditions typically lead employers to slow down hiring or initiate layoffs as operational costs increase and demand softens. A rise in unemployment rates often follows shortly after rate hikes peak, signaling a broader economic slowdown.

Banks and financial institutions become more conservative in their lending practices during tightening cycles. Access to credit becomes restricted, particularly for small businesses and households. This reduction in credit availability can suppress growth, increase default risks, and accelerate the onset of recessionary pressures.

Why these signals matter:

They help economists and investors predict downturns before they fully unfold.

Policymakers often watch these signals closely to decide whether to pause or reverse course.

For businesses and individuals, recognizing these signs early can guide better financial planning.

The lag effect of monetary policy

When central banks adjust interest rates, the effects are not felt right away. It takes time for those changes to work their way through the economy. This delay, known as the lag effect, is one of the biggest challenges in monetary policy. Although rate hikes or cuts are intended to influence inflation and economic growth, the results often take months or even years to become visible. Understanding this lag is essential for anyone trying to interpret policy decisions or plan for what comes next.

Time frames between policy changes and economic impact

Financial markets often react instantly to rate decisions or even hints from central banks. Borrowing and lending adjust more gradually. Mortgage rates may move within days, but shifts in business investment usually take several months. Employment and spending are slower still, as companies wait to see how demand changes before hiring or firing.

| Time Frame | Key Areas Affected |

|---|---|

| Immediate | Market sentiment, stock prices, bond yields, currency values |

| Short-Term (3–6 months) | Mortgage rates, consumer loans, credit card spending |

| Medium-Term (6–12 months) | Business investment, hiring decisions, inventory adjustments |

| Long-Term (12–24 months) | Broader economic indicators such as GDP growth, unemployment rates, and inflation |

Why this delay matters

It makes policymaking harder, central banks must act based on forecasts, not current data.

By the time the impact shows up, conditions may have already changed.

Over-tightening or under-tightening is a real risk if timing is off.

Challenges in predicting outcomes

Monetary policy decisions are made in real time but their effects play out in the future. That makes prediction tricky.

What makes it difficult

Economic data is backward-looking. Central banks base decisions on reports that reflect past conditions, not future trends.

Global factors interfere. Oil prices, war, or supply chain shocks can overpower domestic policy effects.

Consumer and business behavior varies. A rate hike might cause one household to cut spending while another keeps borrowing.

Lag length is inconsistent. Sometimes policy impacts emerge within six months. In other cases, it may take over a year. The timing depends heavily on the broader economic environment.

Real-world examples

In 2006, the Fed finished raising rates just before the housing crash took full effect in 2008.

After the 2020 pandemic response, it took nearly two years for inflation to fully show the consequences of ultra-low rates and massive liquidity.

Why it matters

Mistiming rate changes can either stall a recovery or let inflation get out of hand.

Investors, consumers, and businesses must plan without knowing when the real impact will hit.

Being aware of the lag helps avoid overreacting to short-term market noise.

Implications for investors and markets

Interest rate changes have a ripple effect across global financial markets. Whether central banks are tightening or easing policy, investors must stay alert to shifting conditions. Rate hikes can slow growth and increase borrowing costs, while rate cuts often fuel market optimism and risk-taking. Understanding how different phases of the monetary cycle affect asset performance helps investors make more informed and timely decisions.

Strategies during tightening and easing phases

When interest rates rise or fall, market dynamics shift. Adapting your strategy to match the policy environment can help protect capital and uncover new opportunities.

During tightening cycles (rate hikes):

Focus on quality. Look for companies with strong balance sheets, low debt, and steady cash flows. They are better positioned to handle higher borrowing costs.

Shorten bond duration. Rising rates reduce the value of long-term bonds. Investors often shift to short-duration or floating-rate instruments to reduce interest rate risk.

Hold more cash or cash equivalents. As rates rise, yields on money market funds and savings accounts become more attractive with lower risk.

Reduce exposure to high-growth or speculative stocks. These stocks typically suffer more when rates rise, as their future earnings are discounted more heavily.

During easing cycles (rate cuts):

Lean into growth assets. Lower rates often boost tech, consumer discretionary, and other growth sectors, as borrowing becomes cheaper and sentiment improves.

Extend bond duration. Falling rates benefit longer-term bonds, as their fixed payments become more attractive.

Increase equity exposure. Rate cuts typically support higher stock valuations and improve investor appetite for risk.

Consider real estate and dividend-paying stocks. These assets tend to benefit from lower financing costs and steady income streams.

If you want to trade based on the impact of rate hikes and cuts, we suggest you do so through any of the brokers below. They are known for offering good support for a wide range of assets.

| Currency pairs | Crypto | Stocks | Min. deposit, $ | Max. leverage | Regulation | TU overall score | Open an account | |

|---|---|---|---|---|---|---|---|---|

| 50 | Yes | Yes | 10 | 1:1000 | No | 7.89 | Go to broker Your capital is at risk.

|

|

| 60 | Yes | Yes | 100 | 1:300 | CySEC, FCA, ASIC, FMA, FSCA, FSA Seychelles, EFSA, MAS, DFSA, SCB | 7.52 | Go to broker 80% of retail CFD accounts lose money. |

|

| 69 | No | No | 50 | 1:50 | CFTC, NFA | 6.81 | Go to broker Your capital is at risk. |

|

| 68 | Yes | Yes | No | 1:200 | FSC (BVI), ASIC, IIROC, FCA, CFTC, NFA | 6.8 | Go to broker Your capital is at risk. |

|

| 80 | Yes | Yes | 100 | 1:50 | CIMA, FCA, FSA (Japan), NFA, IIROC, ASIC, CFTC | 6.74 | Study review |

Momentum shocks matter more than direction

One of the biggest traps for new investors is assuming that rate hikes or cuts produce immediate and predictable outcomes. In reality, what moves markets is not the direction of change but the speed and the element of surprise. A slow series of hikes gives markets time to adjust. A sudden move, even if small, can instantly freeze credit, halt investment, and weaken risk appetite. Most recessions do not begin with the first hike. They begin when markets sense that central banks have lost control of timing. If you are tracking monetary cycles, it is better to focus on how unexpected the shift is rather than just what the headline says.

Rate cuts can be just as revealing. While many see them as a sign of relief, they often confirm that damage has already occurred. By the time central banks begin cutting aggressively, credit conditions have tightened, job growth has slowed, and defaults may already be rising. Waiting for rate cuts as a signal of safety is like waiting for an alarm after the fire has already started. What truly matters is not only the policy decision itself, but the urgency behind it. Real insight comes from understanding what the central bank is reacting to and not just what it announces.

Conclusion

Rate cycles are not simple patterns you can trade like weather forecasts. They are moves shaped by fear, hope and late decisions. A hike or a cut on its own says little. What matters is the speed, the surprise and the panic behind it. For anyone watching markets the real skill is not guessing what the central bank will do next. It is sensing when they no longer have control over what happens after. That is when recessions stop being theory and start becoming reality.

FAQs

Can rate cuts prevent a recession entirely?

Rate cuts can soften the impact of a downturn by lowering borrowing costs and stimulating demand, but they cannot always prevent a recession, especially if structural or external shocks are involved.

What are the signs that a central bank might change interest rates?

Key signs include shifts in inflation, employment data, GDP growth, and central bank statements. Market expectations, yield curve movements, and policy minutes also provide clues to potential rate changes.

How do bond markets react to interest rate fluctuations?

Bond prices move inversely to interest rates – when rates rise, bond prices typically fall. Yield curves may flatten or invert based on expectations of future rate moves and economic outlook.

Are there sectors that benefit from rising interest rates?

Yes, sectors like banking, insurance, and capital goods often benefit from rising rates due to improved interest margins or increased infrastructure investment. Conversely, rate-sensitive sectors like real estate and utilities may face pressure.

Editors' Top Picks and Insights

BitMEX is shutting down: Why Trump could not save the exchange

Do governments need crypto workers?

Brent nears $100: Why oil prices are rising

Gram Wallet launch: Can Telegram bring crypto to the masses?

AI without limits: How dangerous are neural networks?

Worldcoin on Wall Street: From iris scans to ETF

Related Articles

Team that worked on the article

Anton Kharitonov is an active trader and analyst. He employs both short- and long-term trading strategies, primarily based on fundamental factors, supported by technical indicators and intermarket analysis.

One of the most widely respected and quoted currency experts, Marc Chandler has been analyzing and advising on the global capital markets for more than 30 years. Throughout his career on Wall Street, Chandler has advised private businesses, hedge funds and asset managers on navigating the foreign exchange market.

Chinmay Soni is a financial analyst with more than 5 years of experience in working with stocks, Forex, derivatives, and other assets. As a founder of a boutique research firm and an active researcher, he covers various industries and fields, providing insights backed by statistical data.

Forex leverage is a tool enabling traders to control larger positions with a relatively small amount of capital, amplifying potential profits and losses based on the chosen leverage ratio.

Economic indicators — a tool of fundamental analysis that allows to assess the state of an economic entity or the economy as a whole, as well as to make a forecast. These include: GDP, discount rates, inflation data, unemployment statistics, industrial production data, consumer price indices, etc.

Index in trading is the measure of the performance of a group of stocks, which can include the assets and securities in it.

An investor is an individual, who invests money in an asset with the expectation that its value would appreciate in the future. The asset can be anything, including a bond, debenture, mutual fund, equity, gold, silver, exchange-traded funds (ETFs), and real-estate property.

CFD is a contract between an investor/trader and seller that demonstrates that the trader will need to pay the price difference between the current value of the asset and its value at the time of contract to the seller.

-

Afghanistan

Afghanistan

-

Albania

Albania

-

Algeria

Algeria

-

Angola

Angola

-

Argentina

Argentina

-

Armenia

Armenia

-

Australia

Australia

-

Austria

Austria

-

Azerbaijan

Azerbaijan

-

Bahamas

Bahamas

-

Bahrain

Bahrain

-

Bangladesh

Bangladesh

-

Belarus

Belarus

-

Belgium

Belgium

-

Bolivia

Bolivia

-

Botswana

Botswana

-

Brazil

Brazil

-

Brunei

Brunei

-

Bulgaria

Bulgaria

-

Cambodia

Cambodia

-

Cameroon

Cameroon

-

Canada

Canada

-

Chile

Chile

-

China

China

-

Colombia

Colombia

-

Congo

Congo

-

Costa Rica

Costa Rica

-

Cote d'Ivoire

Cote d'Ivoire

-

Croatia

Croatia

-

Cuba

Cuba

-

Cyprus

Cyprus

-

Czechia

Czechia

-

DR Congo

DR Congo

-

Denmark

Denmark

-

Dominican Republic

Dominican Republic

-

Ecuador

Ecuador

-

Egypt

Egypt

-

El Salvador

El Salvador

-

Estonia

Estonia

-

Eswatini

Eswatini

-

Ethiopia

Ethiopia

-

Finland

Finland

-

France

France

-

Georgia

Georgia

-

Germany

Germany

-

Ghana

Ghana

-

Greece

Greece

-

Haiti

Haiti

-

Hong Kong

Hong Kong

-

Hungary

Hungary

-

India

India

-

Indonesia

Indonesia

-

Iran, Islamic republic

Iran, Islamic republic

-

Iraq

Iraq

-

Ireland

Ireland

-

Israel

Israel

-

Italy

Italy

-

Jamaica

Jamaica

-

Japan

Japan

-

Jordan

Jordan

-

Kazakhstan

Kazakhstan

-

Kenya

Kenya

-

Korea

Korea

-

Kuwait

Kuwait

-

Kyrgyzstan

Kyrgyzstan

-

Laos

Laos

-

Latvia

Latvia

-

Lebanon

Lebanon

-

Lesotho

Lesotho

-

Libya

Libya

-

Lithuania

Lithuania

-

Luxembourg

Luxembourg

-

Madagascar

Madagascar

-

Malaysia

Malaysia

-

Malta

Malta

-

Mauritius

Mauritius

-

Mexico

Mexico

-

Moldova

Moldova

-

Mongolia

Mongolia

-

Montenegro

Montenegro

-

Morocco

Morocco

-

Mozambique

Mozambique

-

Myanmar

Myanmar

-

Namibia

Namibia

-

Nepal

Nepal

-

Netherlands

Netherlands

-

New Zealand

New Zealand

-

Nigeria

Nigeria

-

North Macedonia

North Macedonia

-

Norway

Norway

-

Oman

Oman

-

Pakistan

Pakistan

-

Palestine

Palestine

-

Panama

Panama

-

Papua New Guinea

Papua New Guinea

-

Paraguay

Paraguay

-

Peru

Peru

-

Philippines

Philippines

-

Poland

Poland

-

Portugal

Portugal

-

Puerto Rico

Puerto Rico

-

Qatar

Qatar

-

Reunion

Reunion

-

Romania

Romania

-

Rwanda

Rwanda

-

Saudi Arabia

Saudi Arabia

-

Serbia

Serbia

-

Singapore

Singapore

-

Slovakia

Slovakia

-

Slovenia

Slovenia

-

Somalia

Somalia

-

South Africa

South Africa

-

Spain

Spain

-

Sri Lanka

Sri Lanka

-

Sweden

Sweden

-

Switzerland

Switzerland

-

Syria

Syria

-

Taiwan

Taiwan

-

Tajikistan

Tajikistan

-

Tanzania

Tanzania

-

Thailand

Thailand

-

Trinidad and Tobago

Trinidad and Tobago

-

Tunisia

Tunisia

-

Turkey

Turkey

-

UAE

UAE

-

Uganda

Uganda

-

Ukraine

Ukraine

-

United Kingdom

United Kingdom

-

United States

-

Uruguay

Uruguay

-

Uzbekistan

Uzbekistan

-

Venezuela

Venezuela

-

Vietnam

Vietnam

-

Yemen

Yemen

-

Zambia

Zambia

-

Zimbabwe

Zimbabwe

- Forex

- Crypto