How Crypto Is Revolutionizing Cross-Border Payments

Editorial Note: While we adhere to strict Editorial Integrity, this post may contain references to products from our partners. Here's an explanation for How We Make Money. None of the data and information on this webpage constitutes investment advice according to our Disclaimer.

Crypto enables faster, cheaper, and more inclusive cross-border transfers by bypassing traditional banking hurdles. With stablecoins like USDT and USDC, users can send money globally in minutes with low fees and without needing a bank account.

Using crypto for cross-border transfers is not just about saving on fees or skipping banks. It is about bypassing legacy systems that were never built for speed transparency or global inclusion. Traditional remittance rails are full of friction from intermediary banks to currency conversions and blackout periods. Crypto breaks that model by letting value move like email across borders without waiting for permission. The key shift here is not just technical. It is social. When people in unstable economies start trusting stablecoins more than their own banks the future of global money starts changing from the bottom up.

Risk warning: Cryptocurrency markets are highly volatile, with sharp price swings and regulatory uncertainties. Research indicates that 75-90% of traders face losses. Only invest discretionary funds and consult an experienced financial advisor.

The role of cross-border payments

Cross-border payments play a crucial role in the global economy. Whether for remittances or international trade, individuals and businesses move money across countries every day. However, the systems that support these transfers are often slow, costly, and built on outdated infrastructure. In response, digital currencies are emerging as a faster and more affordable option, particularly in regions with limited access to traditional banking services. Understanding the developments in this area sheds light on why digital assets are becoming increasingly relevant in global finance.

Traditional methods and their limitations

Banks and financial institutions have long handled cross-border transfers, but the process is far from smooth.

Most cross-border payments rely on correspondent banking networks like SWIFT. Funds often move through multiple intermediaries before reaching the final destination. Settlement can take several days and involves high fees, especially for smaller transfers.

Key limitations

Slow processing times. TransaFees can include exchange rate markups, wire fees, and service charges, all of which reduce the final amount received by the recipient. Actions may take 2 to 5 days to complete.

High costs. Fees can include exchange rate markups, wire fees, and service charges, all of which reduce the final amount received by the recipient.

Lack of transparency. Senders often cannot track funds in real time, leading to uncertainty.

Limited access. In many developing countries, people lack access to the banking services required to send or receive international transfers.

Delays and high costs hurt individuals relying on remittances. Small businesses face barriers to global trade. Many users seek faster and more affordable alternatives.

Emergence of cryptocurrency as an alternative

Cryptocurrencies are becoming a practical tool for faster, cheaper, and more inclusive cross-border payments. Transfers happen directly from sender to receiver, cutting out middlemen. Blockchain enables real-time settlement and low transaction fees. Stablecoins like USDT and USDC offer price stability, making them more practical for everyday use.

Real-world use cases

Remittances. Workers abroad use crypto to send money home in minutes instead of days.

Freelancer payments. Global remote workers are paid in crypto to avoid delays and high bank fees.

E-commerce. International merchants use crypto for instant settlement and better currency conversion rates.

Crypto enables faster settlement, often within minutes, and typically comes with lower fees, especially for small amounts. It does not require a traditional bank account – a simple mobile wallet is enough – and offers greater transparency through public blockchain records.

However, the price volatility of non-stablecoins may pose risks, while regulatory uncertainty can affect adoption. In addition, user education and limited access to digital tools remain barriers in some regions.

Advantages of using crypto for international transfers

Cryptocurrency is changing how people send money across borders. Unlike banks or wire services, crypto offers a faster, cheaper, and more inclusive way to move funds globally. Whether it is a family sending remittances or a freelancer getting paid, crypto gives people more control over their money, especially in places where traditional banking is slow, expensive, or unavailable.

Speed and efficiency

One of the biggest advantages of crypto is how fast it moves. Crypto transfers move directly from sender to receiver without waiting for bank hours or approval processes. Most transactions settle within minutes, even across time zones, and blockchain networks run 24/7, with no holidays or cut-off times.

Workers abroad can send money to their families instantly, even on weekends. Businesses can settle cross-border payments without delays, and emergency transfers reach people faster when funds are needed urgently.

Bank wires can take two to five business days, while crypto can settle in under ten minutes on many networks, with no paperwork, branch visits, or intermediaries required.

Cost-effectiveness

Crypto also cuts down the cost of sending money internationally. Crypto transfers involve fewer middlemen, which reduces service fees. Exchange rate markups are avoided when sending stablecoins like USDT or USDC, and fees on most blockchain networks are much lower than those charged by traditional remittance services. A $200 transfer through a bank may cost $15–$30, while the same amount sent via crypto can cost under $1, depending on the network.

More money reaches the recipient, which is especially important for low-income families relying on remittances. Small businesses can save on fees when paying suppliers or workers abroad, and regular transfers become more sustainable over time.

Accessibility for the unbanked

Crypto opens the door for millions who do not have access to traditional banking. Crypto only requires a smartphone and an internet connection, with no credit checks, ID verification, or minimum balance needed. Wallet apps are free and simple to use, even for first-time users.

This approach helps migrant workers in cash-heavy economies, people in rural areas without nearby banks, and individuals who lack the formal ID or paperwork required to open traditional accounts.

Traditional banks exclude more than 1.4 billion adults worldwide, while crypto offers them a way to receive, store, and send money safely, creating economic opportunities where access to financial services has long been limited.

| Payment Method | Average Cost per $1,000 Sent | Notes |

|---|---|---|

| Bitcoin (BTC) | ~$1.50 (0.15%) | Network fees vary with congestion. |

| Ethereum (ETH) | ~$5.00 (0.5%) | Fees fluctuate based on network activity. |

| XRP (Ripple) | <$0.01 (<0.001%) | Consistently low fees. |

| SWIFT | $20–$50 (2–5%) | Includes intermediary and FX fees. |

| Western Union | $30–$50 (3–5%) | Fees depend on destination and payout method. |

| PayPal | $50–$70 (5–7%) | Includes transaction and currency conversion fees. |

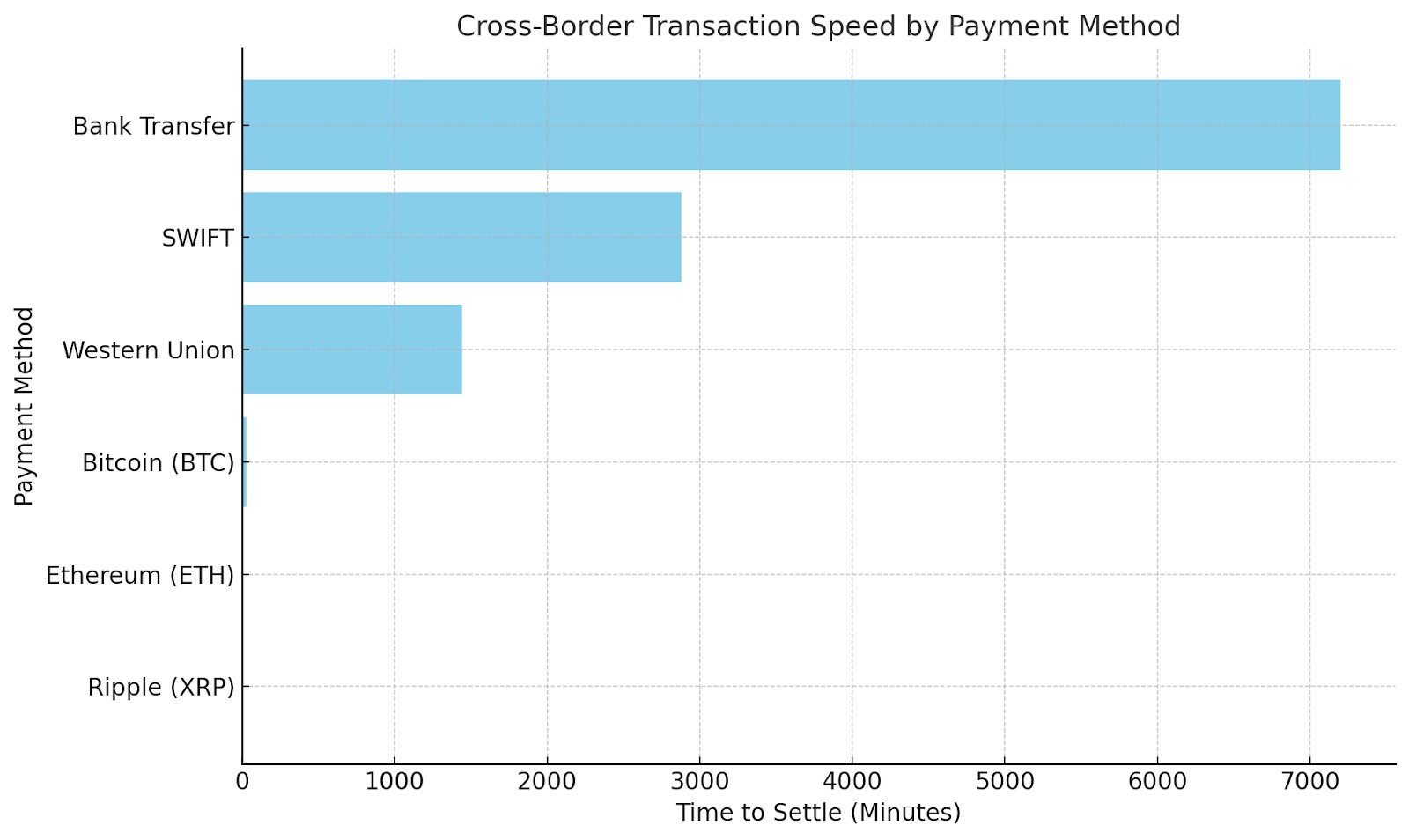

Cryptocurrency is often praised for its speed, affordability, and accessibility but how does it actually compare with the systems people have relied on for decades? Whether it is SWIFT transfers through banks, services like Western Union, or mobile money platforms in emerging markets, each method has strengths and trade-offs. Understanding how crypto stacks up against these legacy systems helps clarify its growing role in international finance.

SWIFT and wire transfers

SWIFT is the backbone of most bank-to-bank cross-border transfers. It connects over 11,000 institutions worldwide. It connects over 11,000 institutions worldwide and underpins the majority of international banking transactions.

Banks use the SWIFT messaging system to send payment instructions, and transfers often pass through several correspondent banks before reaching their destination. Settlement times vary but typically take two to five business days.

The system is slow and rigid, with delays caused by holidays, cut-off times, or compliance checks. Fees are high, as each intermediary may charge its own costs, and currency conversions can include hidden markups. Transparency is limited, and senders often cannot track payments in real time.

How crypto compares

Faster. Settlements in minutes rather than days.

Cheaper. With fewer intermediaries and flat transaction fees.

More transparent. Blockchain allows real-time tracking of transactions.

Money transfer operators like Western Union

Services like Western Union and MoneyGram are widely used for cash-based international remittances.

Users either visit a physical location or use an app to send money, and the funds are then picked up in cash at a branch or delivered to a bank account or mobile wallet. These services are widely used in regions with limited access to traditional banks.

They can be expensive, with fees reaching 7 to 10 percent of the transfer amount, especially for smaller payments. Access is limited by branch hours and locations, forcing recipients to travel or wait in line, and transfers can be slow in remote areas, sometimes taking a day or more, particularly when currency conversion is involved.

How crypto compares

Direct transfers to wallets and no need for branches.

Lower costs, especially for frequent or small transfers.

Instant delivery and 24/7 access.

Mobile money platforms

In many countries, mobile money services like M-Pesa are the primary method of sending and receiving funds.

Users can deposit, withdraw, and transfer money using mobile phone numbers, with local agents handling cash conversion while funds are stored as mobile credits. This system is especially popular in regions with limited banking access, particularly across Africa.

Mobile money enjoys widespread adoption and is deeply embedded in daily life in countries like Kenya, Ghana, and Tanzania. It is convenient and familiar, often working on basic phones via USSD codes without requiring smartphones, and it operates under clear regulations and local supervision.

Its use is often restricted to national borders, with cross-border transfers requiring third-party services. Transaction fees can accumulate over time, and users are typically limited to one provider’s network in many cases.

How crypto compares

Offers true cross-border functionality, allowing users to send money globally rather than being limited to local transfers.

More flexible, working across wallets, platforms, and apps.

Can complement mobile money by offering broader access and faster payments.

Case studies and real-world applications

Migrant workers utilizing crypto for remittances

For many families, remittances are essential. But sending money the old way can be slow and costly. Workers use apps to send money straight to a family member’s phone. Instead of losing money to high transfer fees, they now pay a fraction of the cost. Stablecoins like USDT let families receive money in a currency that holds value, even in countries with inflation.

Examples on the ground

Filipino workers in Europe use crypto wallets to send money home instantly.

In Nigeria, families skip the banks and receive Bitcoin or stablecoins through mobile wallets.

In Argentina or Venezuela, where local currencies lose value fast, crypto remittances help families hold onto more of their money.

Businesses adopting crypto for international payments

Companies are also turning to crypto not because it is trendy, but because it solves real problems. Bank wires are slow and come with fees that eat into margins. Currency exchange delays can hurt planning and cash flow. Some countries make it hard to move money in and out through traditional banks.

How they use crypto

Paying international teams and freelancers quickly and with fewer fees.

Settling invoices using stablecoins to avoid exchange rate shocks.

Moving money across borders instantly without waiting for bank approvals.

If you want to use crypto for cross-border payments, we suggest you do so through only the top crypto exchanges. This will increase the safety of your transactions and also fetch you lower fees. We have presented the best options along with their key features for you to compare.

| Crypto | Foundation year | Min. Deposit, $ | Coins Supported | Spot Taker fee, % | Spot Maker Fee, % | Alerts | Copy trading | Tier-1 regulation | TU overall score | Open an account | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Yes | 2011 | 10 | 278 | 0.4 | 0.25 | Yes | Yes | Yes | 8.7 | Go to broker Your capital is at risk. |

|

| Yes | 2012 | 10 | 249 | 0.5 | 0.5 | Yes | No | Yes | 8.46 | Go to broker Your capital is at risk. |

|

| Yes | 2017 | 10 | 329 | 0.1 | 0.08 | Yes | Yes | No | 8.44 | Go to broker Your capital is at risk. |

|

| Yes | 2014 | 5 | 30 | Not available | Not available | No | No | Yes | 7.84 | Go to broker Your capital is at risk.

|

|

| Yes | 2016 | 1 | 250 | 0.5 | 0.25 | Yes | No | Yes | 7.24 | Go to broker Your capital is at risk. |

The quiet power behind crypto transfers

Most beginners assume that crypto’s biggest advantage is speed. But in reality, its quiet movement is what makes it powerful. In countries with capital controls or unstable banks, the ability to transfer money discreetly without triggering regulatory alerts can be a lifeline. Stablecoins like USDT or USDC move through wallets and apps without passing through the usual checkpoints that cause delays or account freezes. For someone living under the constant threat of a bank shutdown or government restriction, crypto offers more than speed. It provides a path to financial freedom. The goal is not to compete with Western Union’s timing. It is to avoid the risk of getting blocked entirely.

Another point often overlooked is that crypto transfers are only as effective as the off-ramps that make them usable. Sending a stablecoin from Canada to Nigeria may be fast, but if the recipient cannot convert it into local currency or spend it on essential needs, the transfer loses its value. Beginners need to think beyond the send button and understand how the receiver will access and use the funds. In many countries, peer-to-peer markets or trusted local vendors fill that gap. Knowing who enables conversions, how they operate, and what they charge is just as important as selecting the right token. A successful transfer is not only about the technology. It is about completing the final step which is the last mile.

Conclusion

Crypto is changing how money crosses borders not by building faster rails but by removing the barriers altogether. For people who live under financial stress or rigid rules the ability to move value quietly and directly is not just useful. It is survival. But tech alone is not enough. What matters is understanding where it can move smoothly and where the friction still lives. Because the promise of crypto in cross-border payments is not in speed or slogans. It is in freedom that actually reaches the people who need it most.

FAQs

Can recipients easily convert cryptocurrency to local currency?

In many regions, recipients can convert crypto to local currency using exchanges or peer-to-peer platforms, though ease varies based on local infrastructure, regulations, and access to banking services.

Are there specific cryptocurrencies better suited for remittances?

Yes, cryptocurrencies like USDT, USDC, and XRP are often preferred for remittances due to their speed, low fees, and stable value. These features make them more practical for cross-border money transfers.

How do stablecoins address the volatility issue in crypto transfers?

Stablecoins are pegged to fiat currencies like the US dollar, which helps maintain a consistent value during transfers. This stability ensures that recipients receive the expected amount without price swings.

What is the future of cryptocurrency in the global remittance market?

Cryptocurrency is poised to play a larger role in remittances, especially in underserved regions. With improving infrastructure and growing trust in stablecoins, crypto could offer faster, cheaper, and more inclusive transfer options worldwide.

Editors' Top Picks and Insights

Bitcoin price prediction based on RSI: Is BTC poised for a new rally?

Toncoin becomes Gram: Why Durov restored token's original name

Why Tether flipping Ethereum is a pivotal moment for crypto

MiCA deadline: Why crypto companies are leaving Europe

From “Holy Trinity” to WLD crash: How Arthur Hayes became a market-moving seller

The world's first trillionaire: How Musk built his fortune on electric cars, space and AI

Related Articles

Team that worked on the article

Viktoras Karapetjanc is a seasoned financial trader, market analyst, and content creator with over 20 years of expertise in Forex, cryptocurrency, and stock markets. As a contributor to the Traders Union website, he provides in-depth analysis, data-driven strategies, and educational content to empower traders of all levels.

Dan Blystone began his trading career in 1998 as an arbitrage clerk on the floor of the Chicago Mercantile Exchange (CME). He later traded bond and Eurex futures at proprietary firms such as Altea Trading, gaining valuable experience in high-frequency trading and risk management.

Chinmay Soni is a financial analyst with more than 5 years of experience in working with stocks, Forex, derivatives, and other assets. As a founder of a boutique research firm and an active researcher, he covers various industries and fields, providing insights backed by statistical data.

Ethereum is a decentralized blockchain platform and cryptocurrency that was proposed by Vitalik Buterin in late 2013 and development began in early 2014. It was designed as a versatile platform for creating decentralized applications (DApps) and smart contracts.

Cryptocurrency is a type of digital or virtual currency that relies on cryptography for security. Unlike traditional currencies issued by governments (fiat currencies), cryptocurrencies operate on decentralized networks, typically based on blockchain technology.

An investor is an individual, who invests money in an asset with the expectation that its value would appreciate in the future. The asset can be anything, including a bond, debenture, mutual fund, equity, gold, silver, exchange-traded funds (ETFs), and real-estate property.

Bitcoin is a decentralized digital cryptocurrency that was created in 2009 by an anonymous individual or group using the pseudonym Satoshi Nakamoto. It operates on a technology called blockchain, which is a distributed ledger that records all transactions across a network of computers.

A wire transfer is a method of electronic funds transfer in which money is sent from one bank or financial institution to another, typically across international or domestic boundaries. It involves the sender providing their bank with specific instructions, including the recipient's bank details and the amount to be transferred, and the funds are then electronically moved from the sender's account to the recipient's account.

-

Afghanistan

Afghanistan

-

Albania

Albania

-

Algeria

Algeria

-

Angola

Angola

-

Argentina

Argentina

-

Armenia

Armenia

-

Australia

Australia

-

Austria

Austria

-

Azerbaijan

Azerbaijan

-

Bahamas

Bahamas

-

Bahrain

Bahrain

-

Bangladesh

Bangladesh

-

Belarus

Belarus

-

Belgium

Belgium

-

Bolivia

Bolivia

-

Botswana

Botswana

-

Brazil

Brazil

-

Brunei

Brunei

-

Bulgaria

Bulgaria

-

Cambodia

Cambodia

-

Cameroon

Cameroon

-

Canada

Canada

-

Chile

Chile

-

China

China

-

Colombia

Colombia

-

Congo

Congo

-

Costa Rica

Costa Rica

-

Cote d'Ivoire

Cote d'Ivoire

-

Croatia

Croatia

-

Cuba

Cuba

-

Cyprus

Cyprus

-

Czechia

Czechia

-

DR Congo

DR Congo

-

Denmark

Denmark

-

Dominican Republic

Dominican Republic

-

Ecuador

Ecuador

-

Egypt

Egypt

-

El Salvador

El Salvador

-

Estonia

Estonia

-

Eswatini

Eswatini

-

Ethiopia

Ethiopia

-

Finland

Finland

-

France

France

-

Georgia

Georgia

-

Germany

Germany

-

Ghana

Ghana

-

Greece

Greece

-

Haiti

Haiti

-

Hong Kong

Hong Kong

-

Hungary

Hungary

-

India

India

-

Indonesia

Indonesia

-

Iran, Islamic republic

Iran, Islamic republic

-

Iraq

Iraq

-

Ireland

Ireland

-

Israel

Israel

-

Italy

Italy

-

Jamaica

Jamaica

-

Japan

Japan

-

Jordan

Jordan

-

Kazakhstan

Kazakhstan

-

Kenya

Kenya

-

Korea

Korea

-

Kuwait

Kuwait

-

Kyrgyzstan

Kyrgyzstan

-

Laos

Laos

-

Latvia

Latvia

-

Lebanon

Lebanon

-

Lesotho

Lesotho

-

Libya

Libya

-

Lithuania

Lithuania

-

Luxembourg

Luxembourg

-

Madagascar

Madagascar

-

Malaysia

Malaysia

-

Malta

Malta

-

Mauritius

Mauritius

-

Mexico

Mexico

-

Moldova

Moldova

-

Mongolia

Mongolia

-

Montenegro

Montenegro

-

Morocco

Morocco

-

Mozambique

Mozambique

-

Myanmar

Myanmar

-

Namibia

Namibia

-

Nepal

Nepal

-

Netherlands

Netherlands

-

New Zealand

New Zealand

-

Nigeria

Nigeria

-

North Macedonia

North Macedonia

-

Norway

Norway

-

Oman

Oman

-

Pakistan

Pakistan

-

Palestine

Palestine

-

Panama

Panama

-

Papua New Guinea

Papua New Guinea

-

Paraguay

Paraguay

-

Peru

Peru

-

Philippines

Philippines

-

Poland

Poland

-

Portugal

Portugal

-

Puerto Rico

Puerto Rico

-

Qatar

Qatar

-

Reunion

Reunion

-

Romania

Romania

-

Rwanda

Rwanda

-

Saudi Arabia

Saudi Arabia

-

Serbia

Serbia

-

Singapore

Singapore

-

Slovakia

Slovakia

-

Slovenia

Slovenia

-

Somalia

Somalia

-

South Africa

South Africa

-

Spain

Spain

-

Sri Lanka

Sri Lanka

-

Sweden

Sweden

-

Switzerland

Switzerland

-

Syria

Syria

-

Taiwan

Taiwan

-

Tajikistan

Tajikistan

-

Tanzania

Tanzania

-

Thailand

Thailand

-

Trinidad and Tobago

Trinidad and Tobago

-

Tunisia

Tunisia

-

Turkey

Turkey

-

UAE

UAE

-

Uganda

Uganda

-

Ukraine

Ukraine

-

United Kingdom

United Kingdom

-

United States

-

Uruguay

Uruguay

-

Uzbekistan

Uzbekistan

-

Venezuela

Venezuela

-

Vietnam

Vietnam

-

Yemen

Yemen

-

Zambia

Zambia

-

Zimbabwe

Zimbabwe

- Forex

- Crypto