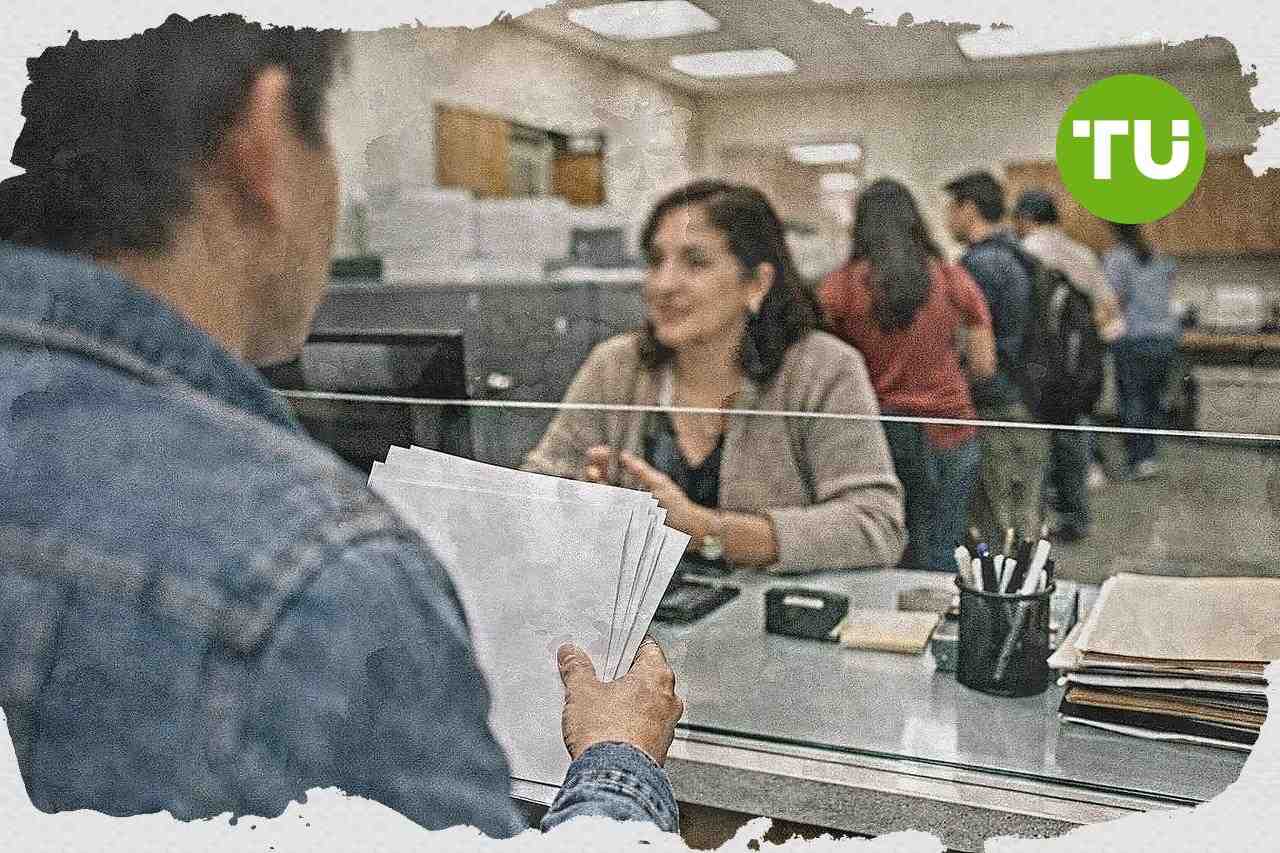

U.S. student-loan borrowers face higher payments after SAVE plan ends

The U.S. Department of Education says borrowers enrolled in former President Joe Biden's SAVE repayment plan need to move to a new option as the program is eliminated following a federal court-approved settlement in March. That shift is pushing millions of borrowers back toward repayment sooner than many expected, with some saying their monthly bills are set to rise sharply. The change affects about 7 million enrolled borrowers and adds pressure to household budgets already strained by housing and energy costs.

Highlights

- Ashley Grupe and other borrowers report monthly payment increases from $54 to $644 and from $800 to $2,000 after the SAVE plan's July 2024 end.

- A federal judge approved an early phaseout of SAVE in March, triggering a 90-day transition window starting July for borrowers to choose new, less generous repayment options.

- Public-service and middle-income households face higher repayment burdens and increased financial pressure, with millions navigating tighter budgets and confusion amid abrupt policy shifts.

Repayment shift raises costs for SAVE borrowers

Borrowers interviewed in the article say the end of SAVE leaves them facing materially higher monthly payments than they had budgeted for under the Biden-era plan. Ashley Grupe, a Missouri state employee working on water quality, says her payment is likely to jump from $54 to $644 this fall. She says the increase threatens her ability to stay on track for Public Service Loan Forgiveness, even though she has 21 qualifying payments left.Former President Joe Biden created SAVE to lower monthly payments and shorten the path to loan forgiveness for some borrowers. Litigation blocked the plan in July 2024, and enrolled borrowers did not have to make payments during that period. In March, a federal judge approved President Donald Trump's settlement to end the plan earlier than the original 2028 phaseout timeline.Other borrowers describe similar payment shocks. Joseph Strafaci says SAVE kept his payments at about $800, while without it he says they would have been close to $2,000 a month. Jordan Hendrickson says her monthly bill is projected to rise from $326 to $2,100, a change she says would squeeze her budget and limit retirement savings.Department sets transition timeline for new plan

The Department of Education says borrowers who have not yet switched plans will start receiving emails from their loan servicers in July. Those notices give borrowers 90 days to choose a new repayment option. If they do not act, servicers will move them to a new plan.The administration is introducing a new income-driven repayment plan this summer, but the article says it is less generous than existing options. That means some borrowers are likely to pay more each month and over a longer period. Department undersecretary Nicholas Kent says the administration's approach is straightforward, that borrowers who take out loans must repay them.Borrowers cited in the article say the process remains confusing because the timeline changed sooner than they expected. Some say they believed they had until 2028 to decide how to proceed. The earlier elimination of SAVE is now forcing faster financial decisions for households already managing other rising living expenses.Budget pressure spreads across public-service and middle-income households

The payment reset highlights broader pressure in the U.S. student-loan market as policy changes flow through to household finances. Borrowers with public-service careers and midlevel professional incomes appear especially exposed when lower monthly payment options disappear. Higher required payments can affect discretionary spending, savings rates, and longer-term financial planning.For borrowers seeking loan forgiveness programs, the loss of a lower-cost repayment option may complicate their ability to remain current until relief is reached. That creates operational challenges not just for individuals but also for servicers and the education system as millions of accounts transition at once. The result is likely to keep repayment policy and affordability at the center of the U.S. consumer finance debate.The case also underscores how court action and administrative changes can rapidly alter repayment expectations for a large borrower base. With the new plan arriving this summer, the next phase for the sector depends on how smoothly borrowers can switch and absorb higher bills. Until then, uncertainty over costs and timelines continues to weigh on affected households.We previously reported that the Education Department would begin notifying about 7 million borrowers enrolled in the SAVE student-loan plan that they have 90 days, starting July 1, to choose a new federal repayment option. Our publication noted that borrowers who do not select a new plan could be automatically moved into another repayment plan, potentially increasing monthly costs and changing forgiveness timelines.

-

Afghanistan

Afghanistan

-

Albania

Albania

-

Algeria

Algeria

-

Angola

Angola

-

Argentina

Argentina

-

Armenia

Armenia

-

Australia

Australia

-

Austria

Austria

-

Azerbaijan

Azerbaijan

-

Bahamas

Bahamas

-

Bahrain

Bahrain

-

Bangladesh

Bangladesh

-

Belarus

Belarus

-

Belgium

Belgium

-

Bolivia

Bolivia

-

Botswana

Botswana

-

Brazil

Brazil

-

Brunei

Brunei

-

Bulgaria

Bulgaria

-

Cambodia

Cambodia

-

Cameroon

Cameroon

-

Canada

Canada

-

Chile

Chile

-

China

China

-

Colombia

Colombia

-

Congo

Congo

-

Costa Rica

Costa Rica

-

Cote d'Ivoire

Cote d'Ivoire

-

Croatia

Croatia

-

Cuba

Cuba

-

Cyprus

Cyprus

-

Czechia

Czechia

-

DR Congo

DR Congo

-

Denmark

Denmark

-

Dominican Republic

Dominican Republic

-

Ecuador

Ecuador

-

Egypt

Egypt

-

El Salvador

El Salvador

-

Estonia

Estonia

-

Eswatini

Eswatini

-

Ethiopia

Ethiopia

-

Finland

Finland

-

France

France

-

Georgia

Georgia

-

Germany

Germany

-

Ghana

Ghana

-

Greece

Greece

-

Haiti

Haiti

-

Hong Kong

Hong Kong

-

Hungary

Hungary

-

India

India

-

Indonesia

Indonesia

-

Iran, Islamic republic

Iran, Islamic republic

-

Iraq

Iraq

-

Ireland

Ireland

-

Israel

Israel

-

Italy

Italy

-

Jamaica

Jamaica

-

Japan

Japan

-

Jordan

Jordan

-

Kazakhstan

Kazakhstan

-

Kenya

Kenya

-

Korea

Korea

-

Kuwait

Kuwait

-

Kyrgyzstan

Kyrgyzstan

-

Laos

Laos

-

Latvia

Latvia

-

Lebanon

Lebanon

-

Lesotho

Lesotho

-

Libya

Libya

-

Lithuania

Lithuania

-

Luxembourg

Luxembourg

-

Madagascar

Madagascar

-

Malaysia

Malaysia

-

Malta

Malta

-

Mauritius

Mauritius

-

Mexico

Mexico

-

Moldova

Moldova

-

Mongolia

Mongolia

-

Montenegro

Montenegro

-

Morocco

Morocco

-

Mozambique

Mozambique

-

Myanmar

Myanmar

-

Namibia

Namibia

-

Nepal

Nepal

-

Netherlands

Netherlands

-

New Zealand

New Zealand

-

Nigeria

Nigeria

-

North Macedonia

North Macedonia

-

Norway

Norway

-

Oman

Oman

-

Pakistan

Pakistan

-

Palestine

Palestine

-

Panama

Panama

-

Papua New Guinea

Papua New Guinea

-

Paraguay

Paraguay

-

Peru

Peru

-

Philippines

Philippines

-

Poland

Poland

-

Portugal

Portugal

-

Puerto Rico

Puerto Rico

-

Qatar

Qatar

-

Reunion

Reunion

-

Romania

Romania

-

Rwanda

Rwanda

-

Saudi Arabia

Saudi Arabia

-

Serbia

Serbia

-

Singapore

Singapore

-

Slovakia

Slovakia

-

Slovenia

Slovenia

-

Somalia

Somalia

-

South Africa

South Africa

-

Spain

Spain

-

Sri Lanka

Sri Lanka

-

Sweden

Sweden

-

Switzerland

Switzerland

-

Syria

Syria

-

Taiwan

Taiwan

-

Tajikistan

Tajikistan

-

Tanzania

Tanzania

-

Thailand

Thailand

-

Trinidad and Tobago

Trinidad and Tobago

-

Tunisia

Tunisia

-

Turkey

Turkey

-

UAE

UAE

-

Uganda

Uganda

-

Ukraine

Ukraine

-

United Kingdom

United Kingdom

-

United States

-

Uruguay

Uruguay

-

Uzbekistan

Uzbekistan

-

Venezuela

Venezuela

-

Vietnam

Vietnam

-

Yemen

Yemen

-

Zambia

Zambia

-

Zimbabwe

Zimbabwe

- Forex

- Crypto