KBRA assigns ratings to UK Logistics CMBS backed by £648.8 million loan

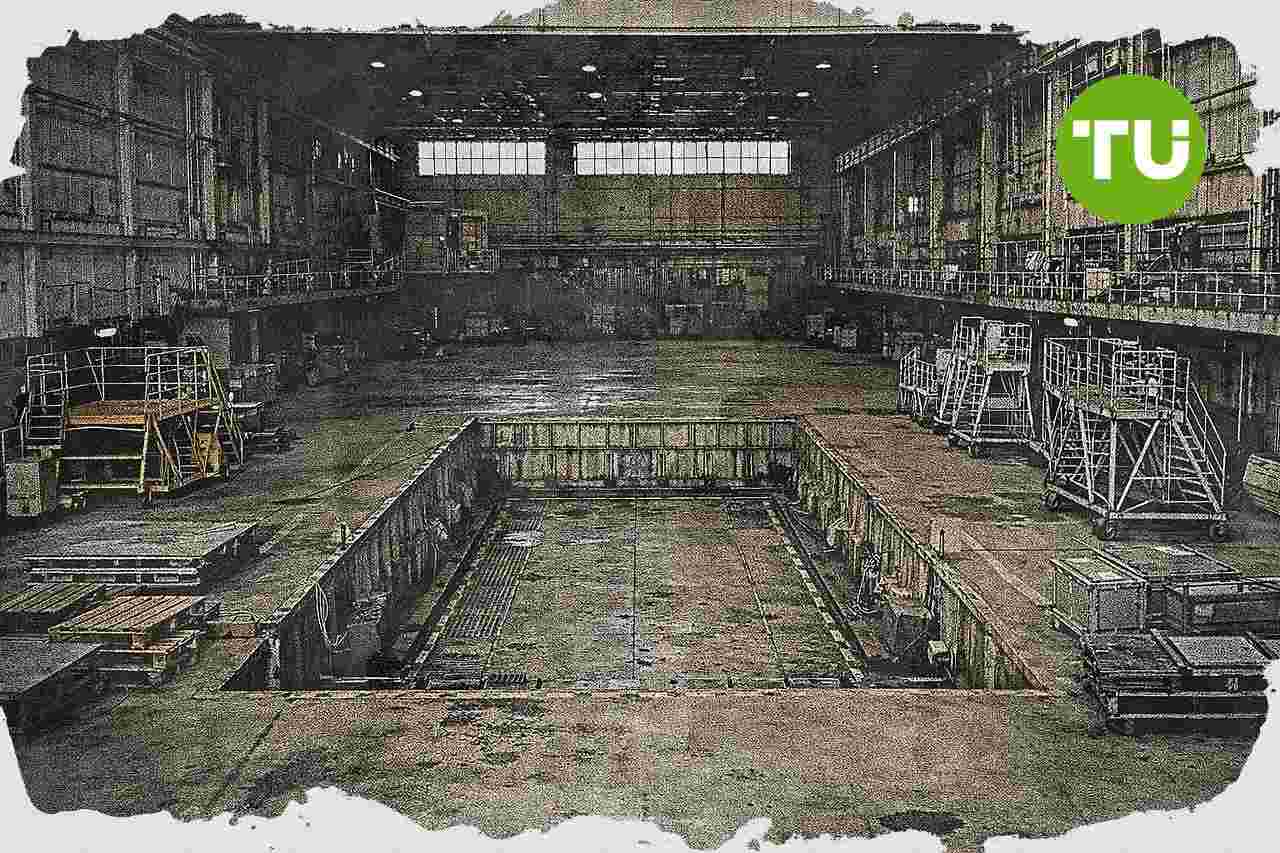

A new UK commercial mortgage-backed securities deal is entering the market with financing tied to a large nationwide industrial property portfolio. The transaction covers 184 logistics and industrial assets and reflects continued investor focus on income-producing warehouse real estate across the UK.

Highlights

- KBRA assigns ratings to five classes of UK Logistics 2026-2 DAC CMBS, backed by a £648.8 million Barclays-originated mortgage loan.

- The collateral comprises 184 industrial properties totaling 9.5 million square feet, 91.7% leased to about 1,700 tenants as of December 2025.

- KBRA's aggregate property values are 36.5% below third-party valuations, with the securitized loan carrying a KLTV of 102.4%.

Transaction structure and collateral profile

As reported by Kroll Bond Rating Agency, KBRA UK assigns ratings to five classes of UK Logistics 2026-2 DAC, a CMBS single-borrower transaction.The collateral for the deal is a £648.8 million limited recourse, first lien mortgage loan originated by Barclays Bank PLC in June 2026. The floating-rate loan carries an initial two-year term and includes three one-year extension options.

The financing is secured by the borrower’s freehold interests in 159 assets and long leasehold interests in 25 assets, covering a total of 184 industrial properties across the UK. The portfolio includes about 1,960 units totaling 9.5 million square feet, with concentrations in the North, Midlands, and Scotland representing 44.9%, 17.6%, and 16.9% of aggregate lettable area, respectively.

Portfolio occupancy and valuation implications

As of December 2025, the properties are 91.7% leased to about 1,700 unique tenants, spanning multinational, regional, and local companies. That tenant mix gives the transaction exposure to a broad base of occupiers within the UK industrial and logistics market.KBRA says it analyses the transaction primarily under its European CMBS Rating Methodology, including a review of the collateral properties’ financial and operating performance to determine sustainable net cash flow and KBRA value. Its capitalisation rates applied to each asset’s KNCF produce values that are, on an aggregate basis, 36.5% below the third-party aggregate portfolio value, while the securitised loan has a KLTV of 102.4%.

Our earlier update on Comber Wind Financial Corporation’s BBB/Stable credit ratings highlighted how contracted revenues and solid operating results supported the issuer and its Series 1 Senior Secured Bonds due 2030. We noted that power generation and debt service coverage stayed above the rating-case expectations through 2025, while wind resource and outage risks remained key constraints to the credit profile.

Latest UK News

-

Afghanistan

Afghanistan

-

Albania

Albania

-

Algeria

Algeria

-

Angola

Angola

-

Argentina

Argentina

-

Armenia

Armenia

-

Australia

Australia

-

Austria

Austria

-

Azerbaijan

Azerbaijan

-

Bahamas

Bahamas

-

Bahrain

Bahrain

-

Bangladesh

Bangladesh

-

Belarus

Belarus

-

Belgium

Belgium

-

Bolivia

Bolivia

-

Botswana

Botswana

-

Brazil

Brazil

-

Brunei

Brunei

-

Bulgaria

Bulgaria

-

Cambodia

Cambodia

-

Cameroon

Cameroon

-

Canada

Canada

-

Chile

Chile

-

China

China

-

Colombia

Colombia

-

Congo

Congo

-

Costa Rica

Costa Rica

-

Cote d'Ivoire

Cote d'Ivoire

-

Croatia

Croatia

-

Cuba

Cuba

-

Cyprus

Cyprus

-

Czechia

Czechia

-

DR Congo

DR Congo

-

Denmark

Denmark

-

Dominican Republic

Dominican Republic

-

Ecuador

Ecuador

-

Egypt

Egypt

-

El Salvador

El Salvador

-

Estonia

Estonia

-

Eswatini

Eswatini

-

Ethiopia

Ethiopia

-

Finland

Finland

-

France

France

-

Georgia

Georgia

-

Germany

Germany

-

Ghana

Ghana

-

Greece

Greece

-

Haiti

Haiti

-

Hong Kong

Hong Kong

-

Hungary

Hungary

-

India

India

-

Indonesia

Indonesia

-

Iran, Islamic republic

Iran, Islamic republic

-

Iraq

Iraq

-

Ireland

Ireland

-

Israel

Israel

-

Italy

Italy

-

Jamaica

Jamaica

-

Japan

Japan

-

Jordan

Jordan

-

Kazakhstan

Kazakhstan

-

Kenya

Kenya

-

Korea

Korea

-

Kuwait

Kuwait

-

Kyrgyzstan

Kyrgyzstan

-

Laos

Laos

-

Latvia

Latvia

-

Lebanon

Lebanon

-

Lesotho

Lesotho

-

Libya

Libya

-

Lithuania

Lithuania

-

Luxembourg

Luxembourg

-

Madagascar

Madagascar

-

Malaysia

Malaysia

-

Malta

Malta

-

Mauritius

Mauritius

-

Mexico

Mexico

-

Moldova

Moldova

-

Mongolia

Mongolia

-

Montenegro

Montenegro

-

Morocco

Morocco

-

Mozambique

Mozambique

-

Myanmar

Myanmar

-

Namibia

Namibia

-

Nepal

Nepal

-

Netherlands

Netherlands

-

New Zealand

New Zealand

-

Nigeria

Nigeria

-

North Macedonia

North Macedonia

-

Norway

Norway

-

Oman

Oman

-

Pakistan

Pakistan

-

Palestine

Palestine

-

Panama

Panama

-

Papua New Guinea

Papua New Guinea

-

Paraguay

Paraguay

-

Peru

Peru

-

Philippines

Philippines

-

Poland

Poland

-

Portugal

Portugal

-

Puerto Rico

Puerto Rico

-

Qatar

Qatar

-

Reunion

Reunion

-

Romania

Romania

-

Rwanda

Rwanda

-

Saudi Arabia

Saudi Arabia

-

Serbia

Serbia

-

Singapore

Singapore

-

Slovakia

Slovakia

-

Slovenia

Slovenia

-

Somalia

Somalia

-

South Africa

South Africa

-

Spain

Spain

-

Sri Lanka

Sri Lanka

-

Sweden

Sweden

-

Switzerland

Switzerland

-

Syria

Syria

-

Taiwan

Taiwan

-

Tajikistan

Tajikistan

-

Tanzania

Tanzania

-

Thailand

Thailand

-

Trinidad and Tobago

Trinidad and Tobago

-

Tunisia

Tunisia

-

Turkey

Turkey

-

UAE

UAE

-

Uganda

Uganda

-

Ukraine

Ukraine

-

United Kingdom

United Kingdom

-

United States

-

Uruguay

Uruguay

-

Uzbekistan

Uzbekistan

-

Venezuela

Venezuela

-

Vietnam

Vietnam

-

Yemen

Yemen

-

Zambia

Zambia

-

Zimbabwe

Zimbabwe

- Forex

- Crypto